14 min read

Looking back

In February 2020 we penned an update letter surveying what we knew about the virus then called 2019-nCov. At that precarious time, we realized we were already in the midst of a truly global pandemic and wondered what the response would be. We did not foresee the scale of the devastation—the toll in lives lost and social upheaval. We did fret about supply chains through Asia becoming snarled, and, perhaps presciently, wrote “We worry about hysteresis, the longer-term effects that stubbornly persist after their initial causes disappear.”

Ultimately, when we look back at February 2020, we recall the feeling of staring out over the abyss. Forecasts were “futile,” we argued, because nature—and the whims of markets—will find a way to disrupt even the most securely laid plans. And yet, our outlook had we been forced to profess one, was for a deep economic slump and asset prices to retrace many months of gains as chastened market participants embedded higher risk premiums and more radical uncertainty in their portfolio.

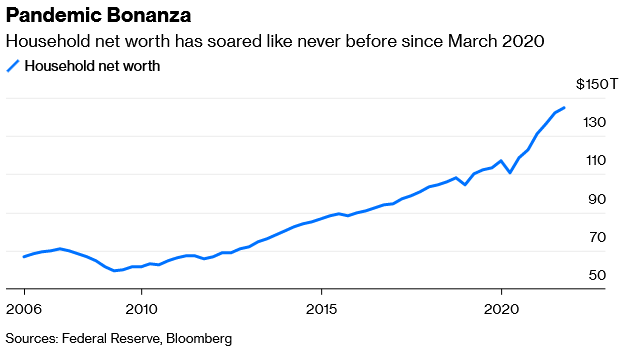

That is exactly what happened… for two months. The Covid recession was officially the briefest in history, as monetary and fiscal policymakers shortly rode to the rescue, providing a floor under all sorts of financial markets and depositing more than $4 trillion in the bank accounts of American individuals and employers alone. Financial markets recovered with palpable giddiness—and then just kept rising. Despite record profits in 2021, the S&P 500—just one, but perhaps the most effervescently priced major index—trades today at over 21 times next year’s earnings. IPOs and less orthodox public listings swelled. Flush with sudden liquidity, the venture capital industry (which had been bunkering for winter since the implosion of WeWork, Masayoshi Son’s profitless and profligate office-rental-cum-consciousness-elevation boondoggle) is freshly rolling in riches and fawning press. Retail traders formed online flash-mobs and pushed the prices of parody currencies and bankrupt businesses into large capitalization territory.

Less than two years after a major party presidential candidate declared that automation would put most Americans out of work, a combination of replenished savings, office ties loosened after months of work-from-home, and justified risk-reward calculations about workplace face-to-face interaction has driven a so-called “Great Resignation.” Far from being automated out of existence, workers are voluntarily stepping away to reevaluate and revalue, while wages (particularly at the lower end) are responding briskly. Employers tell surveys at record rates that finding qualified workers is their greatest challenge. Contrary to the Fed’s expectation when it pledged to keep policy accommodative to ensure a “robust job market,” the obstacle to full employment has lately been labor supply, not demand.

In our view, the market has learned all the wrong lessons from the pandemic. The new “Fed put” has been assumed (including by many on Wall Street with no pre-2008 institutional memory) to be permanent, irrevocable, and ironclad. Yet political conditions are changing; the Fed is now signaling they are willing to remove emergency measures in the face of soaring inflation. The market may have to unlearn many of the conclusions unquestioned since the start of the pandemic—foremost that one should always, without reservation, “buy the dip.” Unprecedented policy measures designed to save lives and incomes also encouraged an orgy of spending on consumer goods, 40-year highs in inflation, and debauched levels of speculation on any financialized asset able to bottle the zeitgeist of the moment. With “stonks,” SPACs, and some parts of the cryptoconomy off more than 50% from their highs, an understanding may be gradually seeping in. Peak liquidity and peak growth imply higher variability of future outcomes and higher dispersion of asset returns.

Leaving the nest

In the coming year, as one major bank puts it, the “training wheels” will have to come off. The Fed will taper asset purchases, and may raise benchmark rates, pushing markets increasingly to stand on their own. We liken this phase of the cycle to an unruly adolescent with great promise, some very good marks, its share of growing pains, and more than one brush with trouble carefully papered over by an unconditional parental backstop. As some point this rambunctious teenager will need to fly the nest—global central bank liquidity is slowing or in decline, wartime levels of fiscal support won’t be repeated, and at least one of three pillars supporting stock markets (record revenues, peak margins, and peak valuations) will likely have to give. A flattening yield curve suggests greater difficulty ahead. So, where will markets land when left on their own?

Given our disdain for forecasts, we can hardly claim to foresee losses where Wall Street strategists predict gains. But dangers are heightened. Economic conditions appear to be facing increasing headwinds and crosswinds, despite strong momentum that should last through most of 2022. Expectations in both equity and credit markets are dialed to the most optimistic end of their historical ranges. The amount of money fleeing seemingly surefire negative real returns in fixed income into private markets has been likened to a deluge. With the idea of purely “transitory” inflation banished to the dustbin of history, a hawkish central bank pivot may be in the offing. Markets are not currently priced for such a new reality. As liquidity is withdrawn, financial conditions tighten, firms who borrowed heavily face debt rollover difficulties, and long-duration (e.g. interest rate-sensitive) stocks that have experienced massive recent buying pressure may cool considerably.

It may be that capital investments inaugurated by ongoing labor shortages, communications technologies baptized in the pandemic work-from-home (WFH) environment, and a centralized infrastructure push from governments will result in a sustained pickup of economic productivity. But this will likely take years. In the meantime, we ask if the economic value added by the resurgent corporate sector (in the face of a rising labor share) is commensurate with all of the cash being thrown at it. If not—and we believe it is not, at least over short horizons—valuations will be inflated and prospective returns will fall. Those are the ingredients for a more defensive posture in portfolios, emphasizing assets more resilient to the greater bouts of volatility ahead.

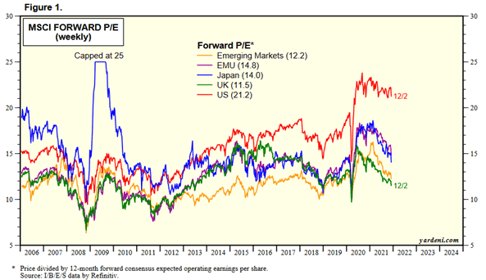

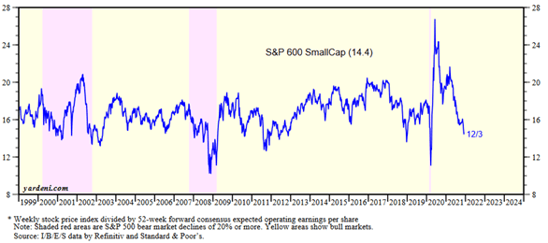

How to invest in this environment? More than ever, our advice is to be sensible. Be diversified. Profitable small-cap stocks in the U.S. trade at mid-teens multiples, several turns below their large-cap peers. International developed markets (with European GDP growth looking perkier than it has in decades) are also relatively cheap. Emerging markets have been challenged on many sides but remain modestly valued. For stocks, “value” and “growth” are increasingly blurry categories, but in a market with rampant price pressures and many macro uncertainties, “quality”—sustainably high profits, pricing power and low debt—seems worth a reasonable premium.

Source: https://www.yardeni.com/pub/mscipe.pdf (December 8, 2021), https://www.yardeni.com/pub/stockmktperatio.pdf (December 10, 2021)

Don’t rush headlong into manias. SPACs and metaverses and blockchains may warrant investigation, but chasing momentum is always a shorter road to ruin than to riches. Be selective; think long-term (decades) and stick with that discipline. Notwithstanding prophetic claims from techno-futurists that we are living in the midst of precipitous structural economic change, patient long-termism remains the one asset that is truly scarce, a renewable source of an investment edge—what Warren Buffett suggests might be called “time horizon arbitrage.” You need not be smarter or faster if you are patient and more disciplined.

Amusingly, many of the loudest proponents of disruptive change are also among the most egregious short-term trend chasers. Unfortunately, they often assume the role of pied pipers for a generation new to investing—to their followers’ great disadvantage. A fundamental truth has been obscured during the almost two years of pandemic-inspired economic Twilight Zone: investing is hard. Especially for a younger generation saddled with student debt, priced out of housing markets, facing historically expensive equities and bonds, witness to multiple financial crises followed by multiple bailouts of the rentier class—their parents. No wonder they seek alternative ways to get rich quick—creating social media-friendly non-fungible tokens (NFTs), chasing meme stocks on Robinhood, resigning from their dead-end jobs in historic numbers. It’s said the collapse of the dot-com bubble crash launched a million startups (Google was a young company then). Maybe the pandemic will spawn a cohort of millions of metaverse-native influencers? Their mood and that of the markets will increasingly come to overlap.

https://www.ppesydney.net/another-speculation-is-possible-the-political-lesson-of-r-wallstreetbets/

Older investors can ill afford to ignore this generation and the long-term sentiment shifts inspired by COVID, its coming-of-age moment. They will inherit vast sums from their parents, and they will care a great deal more about climate and about social justice, while trusting far less in institutions such as the Federal Reserve, Wall Street banks, and financial advisors than had previous generations. The surge in interest around Environmental, Social and Corporate Governance (ESG) investing, seen in the rise and fall of electric vehicle stock valuations, may reflect not simply a fad, but an early warning shot. For those building long-term portfolios, patience and an open mind are virtues (to repeat our earlier counsel concerning cryptocurrencies).

We conclude with some quick notes about what we’re watching in 2022.

- Not out of the woods. Unlike previous false alarms, the Omicron variant combines enhanced transmissibility with vaccine-evading mutations. It thus looks to be substantially more contagious than even the currently rampant Delta variant, with far greater frequency of reinfection. So far, evidence suggests that risk of severe disease may be lower, at least for those with prior immunity.

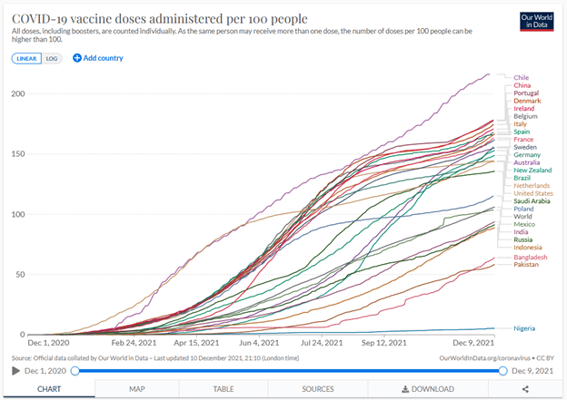

Yet current celebrations are premature; the United States has 130 million unvaccinated people, with only 15% of the population having yet received what appears to be a vital booster shot. Hospitalizations are already picking up; it was shaping up to be a particularly difficult winter even before the latest surprise. The U.S. has a vaccination rate of a middle-income country, and however many Americans get their jabs, unvaccinated billions elsewhere may provide (as do many animal populations) reservoirs of new strains. More infections of lesser average severity do not necessarily imply less overall disease burden. https://ourworldindata.org/covid-vaccinations

https://ourworldindata.org/covid-vaccinations - Speaking of “hysteresis.” We wrap 2021 with a grim acknowledgment of having endured two years of the global pandemic, a catastrophe that has likely claimed more than 15 million lives. We had hoped that the rapid development and then the initially faltering but ultimately widespread rollout of vaccines would have by now returned the economy to something resembling “normal.” Rather, the global toll of disease and the subsequent policy response have cast a much longer shadow than we first predicted.

Worryingly, we are today no closer to resolution of disarray in global supply chains, months after economists had expected logjams to clear. The inflationary implications of Omicron—and newly conceivable variants to follow—are not pretty. The much-delayed recovery in labor supply and easing of logistics bottlenecks may have to be put off further into 2022; if Asian factories and ports to shut down as governments renew a futile containment policy against a virus that spreads much faster even than Delta, shortages may persist even longer. https://www.nytimes.com/2021/09/23/business/cargo-ships-supply-chain.html

https://www.nytimes.com/2021/09/23/business/cargo-ships-supply-chain.html

Vaccination rates at least have increased tremendously in the parts of the world at the source of most manufacturing hiccups. Malaysia, which supplies more semiconductors to the US than any other country, has now vaccinated 79% of its population. That share was only 10% in the Spring when the chip shortages started to bite. Supply chain issues had started to improve in recent months. Chinese coal prices were declining from the surges early in the Fall. Oceanbound freight rates were receding from recent highs. Even the initial discovery of Omicron caused oil futures to drop by 10%. The resilience of the economy’s supply side to new phases of the pandemic will be worth watching 2022 and beyond. - A secular reflation tilt. We wrote about inflation risk here, here, and here. Evidently our predictions for a more inflationary bias have come to pass, though in greater force than we had predicted. To react appropriately, it’s necessary to answer the question “why has inflation returned with such vigor?” The answer is both supply and demand. Supply chain snarls are indeed “transitory”—given a long-enough timeframe. Commodity price gains have quietened to a degree, and investments in factory capacity from chips to electronics to raw materials will gradually bring supply chains into equilibrium. Pent-up savings from stimulus, services spending foregone, and higher wages, however, are largely an American phenomenon and account for the faster pace of price rises in the U.S. than other developed countries.

Wage rises in excess of 5% reflect chronic shortages and more than compensate for increases in productivity. They are inflationary in a stickier sense. The cost of housing, which has risen at greater than 5% for most of the year, is not being addressed in any meaningful way. Thus, at least in the U.S., higher-than-target inflation is with us for the foreseeable future. Surveys and market indicators are beginning to reflect this reality. It must be remembered, however, that inflation rates measure rates of change, not levels. Without a positive fiscal impulse, and with energy, agricultural, and automotive prices having already registered dizzying rises, the pace of increase looks set to moderate. Consumers who brought forward purchases of cars, refrigerators, and home improvements may not be cash-constrained, but they may eventually be sated.

- The year of the tiger. Nowhere did markets and politics collide so tremendously in 2021 as in China. As the CCP reasserts control over an exuberant capitalist economy, the Chinese growth engine is likely to end up somewhere between a hard landing and a more sustainable economic rebalancing. In China, the brakes have been well and truly engaged since May—crackdowns on tech firms and the property sector, enforced power outages, and zero-tolerance COVID policies restricting trade and travel have coupled with a retrenchment in credit to paint a policy backdrop in sharp contrast to the post-GFC loosening. 2022 may herald a more expansive stance, beginning with recent cuts in banks’ required reserve ratios.

As far as the West is concerned, China is more and more a political adversary that unites all factions. The People’s Republic of China likewise has become a huge hot button issue for big business, with both sides of the political aisle united in battering the country's increasing bellicosity and increasingly flagrant human rights abuses. That, combined with a perceived posture of unfriendliness to capital and the pandemic's highlighting the fragility of international supply chains will make any CEO or purchasing manager think twice before outsourcing production to the People's Republic. This will add to inflation pressures.

Unfortunately, while some tariff easing makes sense for both the U.S. and China heading into an Olympic year and a mid-term election, saber-rattling around the Taiwan strait makes for very tricky politics. How goes China still largely determines how goes the emerging markets complex, though this is changing at the margin. Investors in risk assets should hope for détente and policy easing. They should be prepared for the opposite.

Related Posts

Keep Calm ...

... But Mind the Speculative Unwind and Position Cautiously

The Dog that Caught the Car

Last year we visited the topic of inflation, and wondered if, after a decade of false alarms, the...

Happy Holidays, from WMS (and the Market)

“When a consensus of policymakers, commentators and investors is arrayed so overwhelmingly behind...