29 min read

Evergrande: Not a “Lehman moment,” but it may be the first domino to fall in a larger, multiyear rebalancing

China has been in the financial headlines with an uncommon frequency of late, even for the world’s largest economy by purchasing power parity. Strict lockdowns and port closures over the summer gave way to tech crackdowns, bank bailouts, and the looming default of the world’s most indebted real estate firm, Evergrande. American investors who have long voiced concerns over China’s balance of trade, debt-fueled investment binge, and financial repression might be feeling a sense of schadenfreude. But as commentators highlight unsettling parallels between Evergrande and the collapse of Lehman Brothers in 2008, growing anxiety is leaving little room for righteousness.

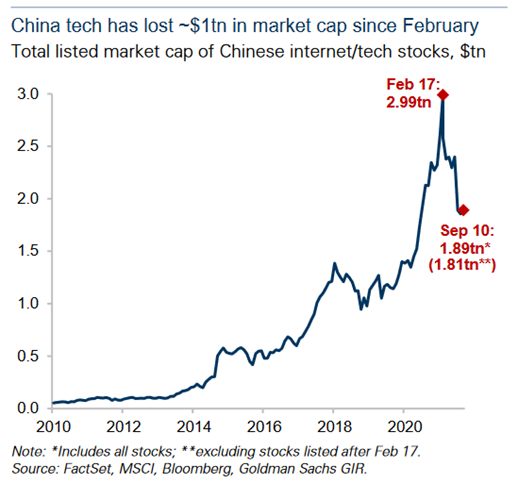

Investors in the Chinese stock markets or American-listed depository receipts have had a rough 2021. Chinese consumer tech shares began the year on a high. For good reason; Alibaba does twice the e-commerce business of Amazon, while Tencent’s super-app has over 1 billion users. Chinese tech champions looked like must-own innovation machines to U.S. investors fed on a diet of FAANGs. But, since February, there have been several score regulatory actions targeting various sectors including internet platforms, education, and property, ostensibly to rein in such abuses as anticompetitive behavior, data privacy and security, and over-leverage. President Xi Jinping’s regulation push has wiped more than $1 trillion of market cap off the Chinese equity market. Even before the Evergrande crisis came to a head, this market tumult led Goldman Sachs to publish an analysis titled “Is China Investable?” To cut to the chase, Goldman’s answer to its own question, and ours, is “yes,—but with certain caveats.

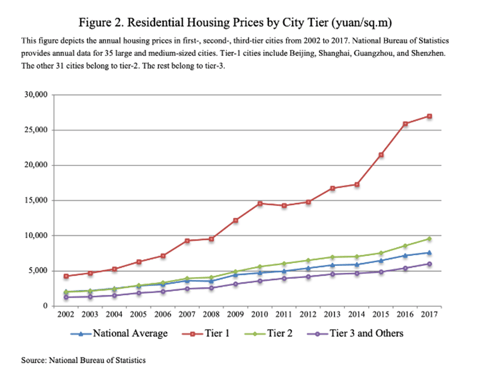

In late September, almost exactly thirteen years after the U.S. mortgage crisis ripped through the global financial system, the most urgent questions surrounded the fate of Evergrande, China’s second largest property developer. Evergrande, which had focused on building apartments in second- and third-tier Chinese cities where prices have risen rapidly yet remain more accessible than the largest coastal megalopolises, is the most indebted real estate firm in the world. Its on-balance sheet liabilities alone amount to fully 2 percent of Chinese GDP, with further off-balance sheet commitments worth another 1%. The company did $110 billion in sales last year and has branched out into unrelated businesses such as sports, insurance, electric cars, and even bottled water. Its construction workforce of 3.8 million augments a full-time staff of 200,000. Clearly an operation of this size and scope, with a web of debts across bank and nonbank lenders and tentacles in dozens of businesses and municipal government offices, has more than a whiff of “Too Big to Fail” about it. Domestic regulators and Western China watchers have been sounding the alarms over potential systemic risk. Almost more concerning than the sheer size of the obligations are their nature: of Evergrande’s $305 billion in liabilities, roughly $200 billion represents deposits that customers have placed on homes not yet built, the equivalent of 1.4 million properties. Many of these pre-sold homes aren’t scheduled for delivery for years. Moreover, many vendors, suppliers, and employees have been paid not with cash, but with commercial paper in the form of wealth management products (WMPs) packaged and marketed by Evergrande itself.

In late September, almost exactly thirteen years after the U.S. mortgage crisis ripped through the global financial system, the most urgent questions surrounded the fate of Evergrande, China’s second largest property developer. Evergrande, which had focused on building apartments in second- and third-tier Chinese cities where prices have risen rapidly yet remain more accessible than the largest coastal megalopolises, is the most indebted real estate firm in the world. Its on-balance sheet liabilities alone amount to fully 2 percent of Chinese GDP, with further off-balance sheet commitments worth another 1%. The company did $110 billion in sales last year and has branched out into unrelated businesses such as sports, insurance, electric cars, and even bottled water. Its construction workforce of 3.8 million augments a full-time staff of 200,000. Clearly an operation of this size and scope, with a web of debts across bank and nonbank lenders and tentacles in dozens of businesses and municipal government offices, has more than a whiff of “Too Big to Fail” about it. Domestic regulators and Western China watchers have been sounding the alarms over potential systemic risk. Almost more concerning than the sheer size of the obligations are their nature: of Evergrande’s $305 billion in liabilities, roughly $200 billion represents deposits that customers have placed on homes not yet built, the equivalent of 1.4 million properties. Many of these pre-sold homes aren’t scheduled for delivery for years. Moreover, many vendors, suppliers, and employees have been paid not with cash, but with commercial paper in the form of wealth management products (WMPs) packaged and marketed by Evergrande itself.

The problem with property

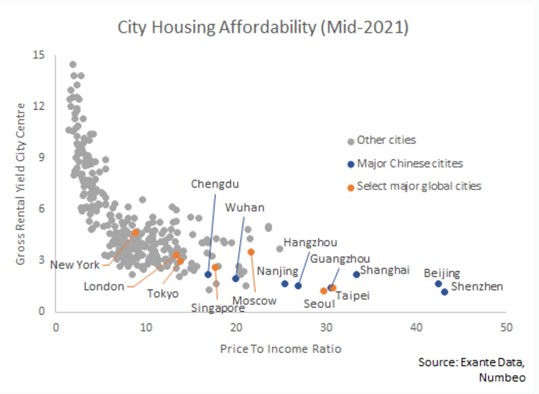

In order to understand how a business like Evergrande could get to the brink, we need to zoom out onto the property sector as a whole, its strategic importance to the CCP and its role in generating the large imbalances that have so animated critics of the Chinese economic model. Building in China has been both a propellant of rapid growth and an enormous wellspring of debt. Rising property prices fuel rising borrowing (and vice versa) in a giddy loop, stoking housing affordability concerns that are more acute in many Chinese cities than even in New York or London. All told, property accounts for as much as 25% of GDP, a much greater share than in the U.S. and on a par with Spain in the height of that country’s pre-crisis real estate bubble. It accounts for roughly 17% of urban employment, while sales of land contribute nearly 30% of local government revenue. Because of a lack of alternative investment outlets, real estate makes up almost 80% of household wealth in China, compared to a 35% share in the U.S. A 90% homeownership rate means that average Chinese have a lot to gain (or lose) from house price appreciation.

https://twitter.com/jnordvig/status/1439562669573513217

https://twitter.com/jnordvig/status/1439562669573513217

Evergrande’s aggressive and creative approach to borrowing is commonplace in its industry. In gross terms, China’s economy is even more vulnerable to a real estate crash than the U.S. or Japan were at the height of their respective property bubbles.

https://voxeu.org/article/can-china-s-outsized-real-estate-sector-amplify-delta-induced-slowdown

https://voxeu.org/article/can-china-s-outsized-real-estate-sector-amplify-delta-induced-slowdown

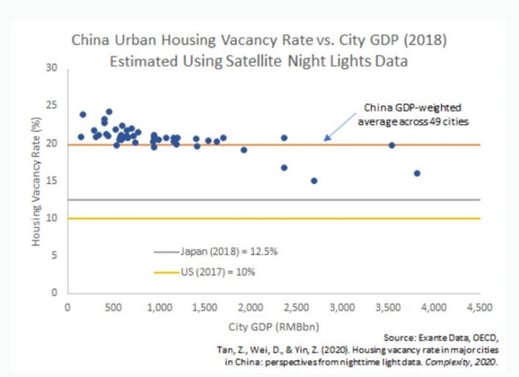

Vacancy rates appear to confirm this vulnerability. Estimates of the percentage of empty apartments range from one-fifth to one-quarter of the total housing stock, much of it sold to speculative buyers with no intention to move in or lease. According to one analyst, there are enough empty homes in China for over 90 million people, greater than the entire population of Germany. This is a giant source of misallocation, funneling large amounts of levered capital to an unproductive asset and imposing a deadweight loss on the economy as a whole. The relatively undeveloped and largely closed nature of China’s financial markets helps explain why property has engendered such a speculative frenzy. Another is loose credit conditions; local party officials, under pressure to meet GDP growth targets set in Beijing, sell land at inflated prices to developers who pay using subsidized debt from state-owned banks. Apartments are then pre-sold as investments to urban professionals. Everyone has an incentive to see prices rise—except those not yet on the housing ladder (particularly the young) and urban migrants. Naturally, the government frets over the long-term unsustainability of this dynamic.

https://twitter.com/jnordvig/status/1439562669573513217, https://adamtooze.substack.com/p/chartbook-on-shutdown-4-neither-chernobyl

Recently officials have imposed limits on second and third home purchases and curtailed resale before five years, but the boom continued undimmed. In October 2017, President Xi famously announced that houses “are for living in, not for speculating.” In 2019 the Politburo declared that property should not be a vehicle for short-term stimulus. Last year, regulators enforced caps on the amount of mortgage debt that banks could own. They then drew “three red lines” on large property developers, requiring financial ratios of debt-to-assets below 70 percent, debt-to-equity below 1-to-1, and cash-to-short-term-liabilities of at least 1. Any developer failing these tests could not incur more indebtedness. By June, Evergrande was in breach of all three tests—particularly the liquidity ratio, with only 36% cash. In effect, Chinese financial regulators deliberately provoked the Evergrande crisis with the goal of pricking the larger property bubble.

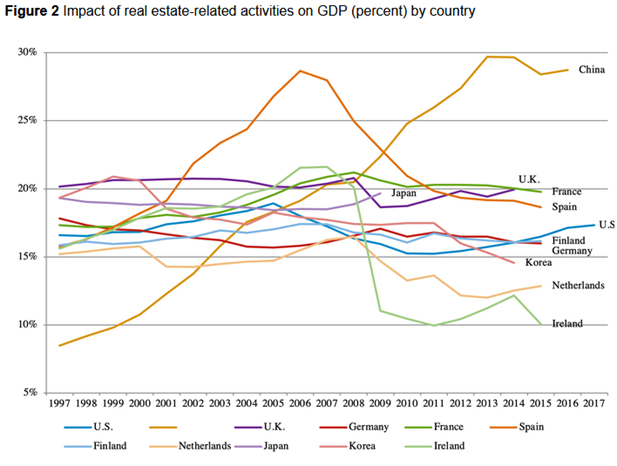

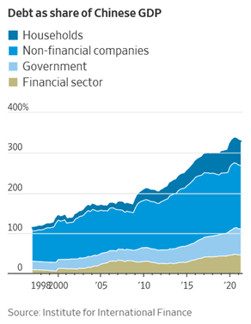

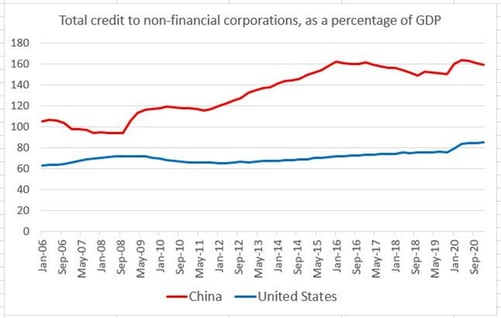

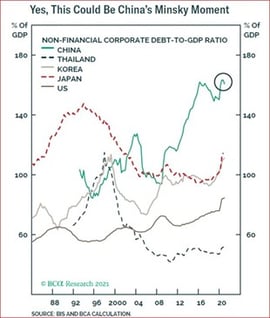

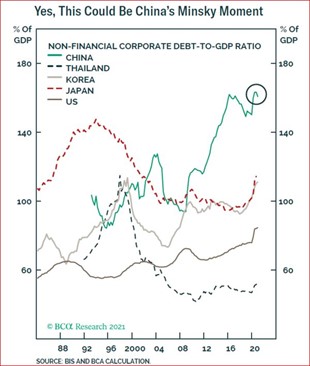

Real property serves as a proxy for the broader problem of over-leverage that the government has been attempting to wrestle for years. Debt has been rising in China at an alarming pace. The Economist writes, “Banking assets have ballooned to about $50trn and they sit alongside a large, Byzantine system of shadow finance. Total credit extended to firms and households has soared from 178% of GDP a decade ago to 287% today.” Private, non-financial sector debt reached 222% of GDP at the end of 2020. Most of that leverage is corporate. The equivalent figure in the U.S. is 164% of GDP. Here are some charts showing the increase in borrowing.

https://www.wsj.com/articles/evergrandes-struggles-reflect-chinas-efforts-to-rein-in-multiyear-debt-boom-11632319200, https://www.ft.com/content/f858fe4a-716e-49ee-bebe-45c810b0d7a6, https://www.bloomberg.com/opinion/articles/2021-09-22/evergrande-won-t-be-a-lehman-like-debt-crisis-china-may-still-slow?sref=CWVdwe0e

How China deals with its property developers will have an important read-through for corporate leverage in general. Investors are watching carefully.

A “Lehman Moment”?

Back to Evergrande. Last week, the giant developer missed an $83 million payment on its U.S. dollar bonds. As of writing, there is little clarity on what sort of resolution process might take place. An expert consensus has emerged, however, that the finance ministry and the PBOC have the ability to keep untrammeled contagion at bay (where have we heard that before?) Two quotes summarize the view that Evergrande will not likely be a replay of Lehman Brothers.

Michael Pettis of Peking University writes,

My best guess is that in the next few days or weeks, perhaps as late as the national holiday in the first week of October, they will take concrete steps and make announcements aimed at toning down the spread of financial distress costs. This will involve what Zhou Xin, of the South China Morning Post, describes as another “cocktail of proven tricks: rolling over debt, haircuts on assets and emergency payments to the most vulnerable.” Most analysts expect—correctly, in my opinion—that there will be a hierarchy of creditors, with the most protected being retail investors, although if investors in wealth management products are substantially bailed out, this will only reinforce the idea that the risks of wealth management products are nonexistent. Local suppliers and contractors are likely next in line for protection, as they did not choose voluntarily to be Evergrande creditors, and any losses they might suffer could threaten in some cases to bring them down. Because local banks are expected to continue to fund growth, they will probably be next in line, followed by other Chinese creditors, with external-currency creditors probably bringing up the rear. A surge in lawsuits as these foreign creditors claim unfair discrimination can be expected.

There is precedent for this. Wei Yao of Société Générale (quoted in Bloomberg) adds,

While we do think that Evergrande is systemically important, we also reckon that Chinese policymakers have the willingness, capability and knowhow to stem a financial market meltdown. On this front, the default of Baoshang Bank on its interbank liabilities in May 2019 is a good reference. Compared with Baoshang at the time of default, Evergrande has much more total debt, but similar amount of liabilities to financial institutions and in the capital markets. Also, Baoshang had more complex ties in the financial system (with over RMB300bn interbank liabilities with over 700 counterparties) and, very importantly, its default was a complete surprise.

These optimistic views do not argue that there is no contagion—only that it doesn’t rise to the level of “systemic.” Crises, of course, are always local until they are not. Many, including then-Fed chair Ben Bernanke, once proclaimed that the U.S. mortgage crisis was “contained.” In contrast to the mortgage crisis in America, Chinese debts are largely owed to and by government-controlled entities. As Leland Miller at China Beige Book says, “There is no durable counterparty risk when the state owns or controls all of the counterparties.” While there are concentrations at certain banks (notably Ping An and Minsheng who have seen their bond prices fall), financial exposure is largely dispersed across the system. In August, regulators rescued Huarong, a failing bank that was judged too interconnected to be left to its fate. So long as the entire property sector doesn’t implode at once, Evergrande can likely be dismantled by committee much in the way that Long Term Capital Management was wound down by the New York Fed and a number of private counterparties.

“In our base case scenario,” write analysts at Liberum (quoted in the Financial Times), “China Evergrande will be allowed to collapse with the most profitable parts of its business bought up by rivals and the debt underwritten by either the [People’s Bank of China] directly, or by a consortium of Chinese commercial banks with the help of a liquidity injection by the PBOC.”

“Unless China’s regulators seriously mismanage the situation,” concurs He Wei at Gavekal, “a systemic crisis in the country’s financial sector is not on the cards.”

So, what sort of contagion is likely? Firstly, there is a direct impact in credit markets, particularly for Evergrande’s highly levered peers. Distress is already evident in the U.S. dollar bonds issued offshore by Chinese property developers. Much of the market is priced for default, with 16% of trading at yields north of 30%. More generally, the Chinese high yield market is close to its lows of last March. The reason why credit stress might spread beyond property is that Evergrande’s default removes the perception of an implicit put offered by Chinese authorities. “Moral hazard” was cited as the concern when the Federal Reserve let Lehman Brothers go to the wall. By taking away moral hazard, China hopes to effect a larger restructuring of asset markets and to encourage more scrupulous pricing of credit. But the assumption of a bailout backstop might structurally lie underneath many Chinese assets; pulling the rug out at once could cause more than one domino to fall. Economist Jens Nordvig wrote on Twitter that broad credit supply will be maintained, as so much is provisioned by state-owned banks, though credit demand should suffer in the intermediate term.

Greater second- and third-order effects are to be expected in the real economy, which Nordvig characterizes as “real contagion.” Some are directly related to the Evergrande debacle; the company has $142 billion in short-term payables to contractors and suppliers of cement, rebar, copper, and ceramic tiles. Until payment is guaranteed, there will be a slowdown and potential job losses across the construction sector. Suppliers who had been paid with short-term Evergrande debt will now suspend work pending upfront cash payment. Evergrande has already announced that its projects are falling behind schedule. Further knock-on effects are visible in commodities. Iron ore and steel production is falling. On September 20, the price of iron ore fell below $100 per ton for the first time in a year. Australian miners might soon feel the pinch.

Shadow lenders contributed 45% of Evergrande’s liabilities as of 2020. Some proportion of these were employees. Workers paid in virtually worthless WMP’s will curtail spending on consumption goods. What about the many customers to whom Evergrande owes 1.4 million homes? They will be very angry seeing their down payments tied up in a lengthy resolution process. Across the country, buyers will be less keen to put down deposits with other developers. Sales volumes are indeed down 16% year-over-year in major cities, with a 23% decline in August. This will of course redound back on already stressed developer balance sheets.

Ultimately, we believe that much of the downstream consequences of Evergrande’s failure are likely to be felt in the form of slower growth. While it is almost certain that authorities will fiddle with the hierarchy of claims against the firm, seeking to protect customers, vendors, and employees at the expense of foreign creditors, the psychological effect could still be chilling. Falling house prices tend to have negative wealth effects, and engender some political unrest. The adjacent chart from Pictet suggests a downtick in consumer spending is already occurring.

Ultimately, we believe that much of the downstream consequences of Evergrande’s failure are likely to be felt in the form of slower growth. While it is almost certain that authorities will fiddle with the hierarchy of claims against the firm, seeking to protect customers, vendors, and employees at the expense of foreign creditors, the psychological effect could still be chilling. Falling house prices tend to have negative wealth effects, and engender some political unrest. The adjacent chart from Pictet suggests a downtick in consumer spending is already occurring.

Equally consequential may be the hit to local government finances, with land sales falling by 90% year-on-year through September. The FT notes that $8.4 trillion of government financing vehicles depend on revenue from land sales. These debt instruments are in many ways the financial engine of China’s infrastructure building boom. A pullback here will mean fewer highways, airports, subways and high-speed trains. On top of demand and supply shocks, China enters 2022 in a very unfavorable position for growth, at least from a demographic point of view. Birthrates have fallen in recent years, despite authorities gesturing at a “three child policy,” and the population is aging rapidly. Further, the urbanization that fueled China’s productivity gains in the first decade of the millennium has slowed. “About three quarters of the cities in China are in population decline,” says Houze Song, an analyst at the think-tank MacroPolo.

Stepping back, the noise around Evergrande is likely amplified by certain parallels with Lehman Brothers—huge debts, real estate, baroque financial linkages. China is facing less immediate, yet broader and deeper imbalances in its economy and financial system. Historian Adam Tooze likens the Evergrande response to a “controlled demolition”—not a sudden stop brought about by market forces, but an effort by financial regulators to begin the process of rebalancing. China’s growth model, so successful in the last two decades, has come to the end of its useful life. “There is a recognition that the old build, build, build playbook does not work anymore and that it is actually getting dangerous,” Leland Miller told the FT. “The leadership now appears to be thinking that it can’t wait any longer to change.”

Chinese debt has climbed for years but began accelerating faster than GDP just before the Great Financial Crisis. With growth targets set by the central government, but productivity-enhancing infrastructure opportunities in increasingly short supply, party officials had nowhere to turn for growth other than state-supported loans. As Americans have learned, ever-increasing debt experiences diminishing marginal utility. For every incremental dollar we borrow, above a certain point, output rises by less than a dollar. Adjusting for increases in physical capital, Chinese actual productivity growth is negative at present. Greg Ip points out in the Wall Street Journal, “Since 2008, [China] has needed ever more debt to deliver the same increment to economic output. Between 2008 and 2019, total debt—government, household and business—rose from 169% to 306% of gross domestic product, but GDP growth fell from 10% to 6%.”

Growth isn’t just slowing; it’s becoming more uneven. Measures of income and wealth inequality in China are among the worst in the world for large countries—perhaps an embarrassment to a nominally communist regime. Much of the distributional strains have been fueled by the property sector. Chinese academics have found that housing causes 75% of Chinese wealth inequality. The inaccessibility of housing for the young may actually be one of the reasons Chinese women are having fewer children. In this context, the failure of Evergrande should be seen as belonging to a multiyear, multipronged social and economic reform initiative that leaders believe is overdue.

China’s “techlash” – biting harder than in the West

Actions taken to reduce debt in the property sector are congruent with the government’s evolving regulatory crackdown that has ramped up through 2021. Among its first targets were consumer internet companies. Most Americans became aware of the “techlash” last year when China halted the IPO of its digital finance darling, Ant Group, an affiliate of Alibaba. The company has now been effectively dismantled, and its founder, the billionaire celebrity Jack Ma, muzzled. His other firm, Alibaba was fined several billion dollars for antitrust violations. Regulations aimed at Tencent, China’s largest social media company, and ByteDance, the owners of TikTok have forced much more stringent restrictions on gathering consumer data, the serving of ads, and on acquisitions. Didi, the ride-hailing app, was subject to a “national security review” after it listed in the U.S. China’s internet regulator then blocked it from signing up new users while removing it from mobile app stores. Tech tycoons have been variously berated and obliged to make billion-dollar charitable contributions.

China is becoming, in the Economist’s words, a “policy laboratory” to enact technology regulation many U.S. and European lawmakers might envy. The “arrows” of its strategy are familiar: data security, antitrust, consumer protection, financial supervision, regulation of media controlled by business moguls. Yet the style of the rulings emanating from Beijing is sudden, uncompromising, and sometimes capricious. The party is clearly in a hurry to issue new rules and enforce them vigorously. One example is the requirement that video game companies scan users’ faces to ensure children play online games for no longer than three hours per week. China has toyed with gaming bans and curfews before, as the country is plagued with an epidemic of myopia in children driven by long hours in front of screens. Now, state media label video games “spiritual opium” (a very meaningfully chosen word in China), while Tencent’s billionaire founder Pony Ma grovels before authorities who accuse him of “ruining a generation.”

Similarly swift and brutal was the crackdown on for-profit education. With the stroke of a pen, regulators essentially kneecapped an entire industry, erasing billions of dollars of public market equity value. Again, as with video game (or social media) addiction, the pretext was the protection of youth. Students study for years to prepare for make-or-break exams that may see them admitted to one of the “Chinese Ivies” such as Peking University, Tsinghua, Fudan, or Shanghai Jiao Tong—all with lower admissions rates than Harvard or Yale. By banning for-profit tutoring, the government seems to be addressing “opportunity hording” by wealthy, well-connected families, a phenomenon that came into the spotlight in America’s own college admissions scandal. The pattern is the same—progressive ambition, authoritarian means.

Most recently, China announced an outright ban on the ownership and trading of cryptocurrency, consolidating several half-steps it had taken in the past months and years. Exchanges, miners, and services are all proscribed: “No room for discussion. No gray area.” China may have several goals here, not least of which is control over financial flows in a system where the capital account is, for official purposes, closed. China is introducing a digital currency, the “digital RMB,” which it hopes to have a prominent place in financial transactions. It will certainly brook no private competition. But China is also trying to play its part in fighting climate change, having announced a commitment to carbon neutrality by 2060 and peak emissions by 2030. The massive amounts of energy consumed by crypto miners stress China’s electricity grid; according to Bloomberg, in April China had a 46% share of the global hash rate, a measure of the computing power used to mine crypto coins.

Why is China taking an axe to so many of its leading industries? Why now? With respect to the tech crackdown, there are strategic reasons at play. China had built a world-class tech sector, defying critics who accused its firms only of Western business models while failing to innovate indigenously. But China is only smashing certain kinds of businesses—those catering to consumers on the Internet. Huawei, for example, is still in favor. AI, electric vehicles and semiconductors remain beneficiaries of massive state largesse. When Americans speak of “tech,” they are usually thinking very narrowly of software businesses, usually consumer-facing, usually on the Internet. Before the likes of Facebook and Google, “tech” used to mean industrial R&D labs, chemicals, hardware, robotic automation. In China, this is still what “tech means”—much of the consumer internet ecosystem is, in Beijing’s planners’ view, a mindless distraction at best, and, at worst, an unproductive vacuum for long-term risk capital. In 2019, Dan Wang at Gavekal very eloquently explained this way of thinking:

I find it bizarre that the world has decided that consumer internet is the highest form of technology. It’s not obvious to me that apps like WeChat, Facebook, or Snap are doing the most important work pushing forward our technologically-accelerating civilization. To me, it’s entirely plausible that Facebook and Tencent might be net-negative for technological developments. The apps they develop offer fun, productivity-dragging distractions; and the companies pull smart kids from R&D-intensive fields like materials science or semiconductor manufacturing, into ad optimization and game development. The internet companies in San Francisco and Beijing are highly skilled at business model innovation and leveraging network effects, not necessarily R&D and the creation of new IP….I wish we would drop the notion that China is leading in technology because it has a vibrant consumer internet. A large population of people who play games, buy household goods online, and order food delivery does not make a country a technological or scientific leader… These are fine companies, but in my view, the milestones of our technological civilization ought to be found in scientific and industrial achievements instead.

China has no need for glamorous startups or venture capital hype. What it seeks is strategic military and industrial advantage. Last year, Wang wrote “It’s become apparent in the last few months that the Chinese leadership has moved towards the view that hard tech is more valuable than products that take us more deeply into the digital world.” Beijing is pivoting to a different industrial policy focused on rivalry with the West. The industries it champions will be those that allow it to win the technological battlefield—military and communications hardware, chips, AI, biotech, batteries, cleantech. It seeks to pioneer and control technological standards, much as the U.S. did with wireless telecommunications and the Internet. For all the focus on Alibaba, Baidu, JD.com, and Pinduoduo, one only needed to look at the Made in China 2025 agenda to apprehend which industries Xi Jinping sees as critical. Ip, again in the Journal, writes “even as the Chinese Communist Party unleashes a multifront regulatory assault against consumer internet companies, it continues to shower subsidies, protection and ‘buy-Chinese’ mandates on manufacturers.” Like property and construction, consumer tech was potentially crowding out more innovative sectors and needed its wings clipped. Just as China shifts its energy mix toward renewables, and its automobile fleet toward EVs, the leadership is thinking of sustainability in the very broad sense—including, and especially, sustaining its political hegemony. Mass media, social media, and culture are sectors that may be targeted in the future, while inputs into military-industrial supremacy will remain untouched.

“Quality Growth”

In the West, there has been much debate around what constitutes “sustainable” growth—that is, real, per capita GDP that does not borrow from the future, either in financial terms or in terms of natural resource endowments. China too recognizes that certain sectors of the economy (though certainly not households) have been living beyond their means. Since coming to power in 2012, President Xi has emphasized the pursuit of what he calls “quality growth.” By this he means, according to David Li of Tsinghua University, “[g]rowth that is based on innovation rather than resource consumption or intensifying investment, is inclusive or equitable for society as a whole, and is environmentally sustainable.” By contrast, highly leveraged white elephant projects such as empty apartment blocks and high-speed trains to nowhere represent “fictional growth,” as Xi put it in an editorial for a leading CCP mouthpiece.

Michael Pettis estimates that “quality growth” likely accounted for little over half of China’s stated GDP growth rate in recent years. That means that eliminating the sources of overinvestment necessarily implies a growth slowdown. While he doubts Evergrande will provoke a sudden or sharp crash, Ting Lu, the chief China economist at the investment bank Nomura, says, “I think China’s potential [annual] growth rate will drop to 4 per cent or even lower between 2025 and 2030.” Miller of China Beige Book suggests a rate of 1 to 2 percent is possible a decade hence. Given China’s debt backdrop and deteriorating demographic picture, this might not be a terrible outcome. Even if it avoids crisis, Jonas Goltermann of Capital Economics told the FT, China’s “medium-term prospects are much worse than generally acknowledged.” Goldman Sachs’ chief China economist Hui Shan is more optimistic. He believes the shift in emphasis around innovation will lead to more measured productivity, and points to the highly educated engineering workforce as font of ideas and entrepreneurial skill. Any Evergrande-induced slowdown, Shan and David Li argue, will likely be temporary.

Deeply linked with “quality growth” is a new concept in Chinese political discourse: “common prosperity.” This vague and slightly ominous term might carry connotations of Mao-era reeducation camps and forced collectivization, but is generally taken to mean a thrust toward greater socioeconomic cohesiveness. The Economist skeptically describes it as “a catch-all phrase extending from a reduction in social inequality to more coddling of workers and customers to the nannying of overstressed youngsters.” What’s important to appreciate is that “common prosperity” is the political pretext for cracking down on tech, slamming the brakes on property investment, and enduring a growth slowdown that might otherwise provoke rising dissent. China recognizes that in a future where 8% annual GDP growth is no longer achievable, policy still has ample space to continue to lift middle incomes simply via distribution of the spoils. Boosting consumer disposable income and economic security, even at the expense of entrenched elites, can ensure the Party’s legitimacy through the exhaustion of its legacy development model. “The slogan of ‘common prosperity’ is a narrative change that paves the way for a shift in the growth model,” says Miller. “It clarifies that a drop in GDP growth is not a failure for the Chinese Communist party.”

But “common prosperity” is not just rhetoric. It embeds concrete actions. Goldman’s Shan points to an economic plan set forth for the province of Zhejiang. Rather than simply targeting output growth as in the past, the plan identifies goals of increasing wages’ share of GDP to 50% and ensuring 80% of households have disposable income of more than $15,500. “Common” implies redistributional outcomes, but “prosperity” still recalls the central goal of growth; the Zhejiang plan also intends to double household income inside of a decade.

Broadly, the objective is to restructure the economy away from a model of endless fixed investment-driven, debt- and resource-intensive growth. More often than not, this model took the form of “crony capitalism with Chinese characteristics,” with benefits mostly accruing to politically connected elites and their children. It has generated tremendous wealth inequality, suppressed consumption, created capital market distortions, suppressed borrowing rates for favored industries at households’ expense, and allowed for the rise of a class of internet plutocrats with unprecedented control of consumer data. As do many in the West, China’s government appears now to believe that a more equitable economy can simultaneously be more productive. There is much space for consumption to assume greater leadership. For Exhibit 1, see Chinese households high savings rates, which export surpluses to the rest of the world in the form of financial flows that force down key interest rates such as those on U.S. Treasuries.

The preceding might be read as positioning China as the world’s enlightened despot, showing the West the way to redress financial imbalances, decarbonize the economy, bolster sustainable and inclusive growth, and lead all in a hymn of “Kumbaya.” Its abject human rights record should not be forgotten, nor should decades of trade policies and intellectual property theft that have immiserated many Western workers and flouted international law. It retains barbaric vestiges of Maoist exploitation, such as the hukou system of household registration that denies migrant workers access to homes, schools, and social services. Moreover, many of the reforms that we otherwise applaud are being implemented in an incredibly heavy-handed manner. So which is it? Is China’s leadership belatedly clamping down on excesses in its “build build build” economy to better protect children, investors, and consumers, and to ensure a more equitable distribution of wealth? Or is Xi simply consolidating power ahead of its 20th Party Congress in 2022 where he is expected to break with tradition and receive a third term, effectively becoming president for life?

Greg Ip characterizes China’s regulatory push as “creeping nationalization,” while economist and veteran China watcher George Magnus tells Goldman Sachs that the “regulatory crackdown has the hallmark of a crafted plan to reinforce the primacy of the party and the state machine and subjugate private firms and entrepreneurs.” A distinct lack of transparency in the details of the various edicts being promulgated seemingly permits the state a wide latitude to interfere in the operations of putatively private businesses. Rules have been hastily enacted in a manner that violates a basic principle since the reforms of Deng Xiaoping: grandfathering. New rules are immediate, sweeping, and retroactive. Instead, David Li argues that dispensing with this principle allows the official dragnet to catchup all of its targets, without giving license to clamor for exemptions, loopholes, and delays.

The answer to the question of whether the government’s recent moves are about truly needed reform, or are instead a naked power grab, is probably “both.” Xi Jinping has accrued to himself power unprecedented since Mao and is determined to use it forcefully. We leave it to political philosophers to interpret whether “Xi Jinping thought” has more in common with market socialism or unreconstructed Leninism. What is clear is that, for years, China’s leaders have recognized a need to restructure the economy and rebalance from the investment and export growth model. The fabulous increase in debt since the GFC have only increased their urgency. Reform-minded aims had in the past been held back by powerful elites heavily invested in the current economic arrangements—CEOs, bankers, and government ministers on the boards of both state-owned and private businesses. These “vested interests,” as they are known in China, were the target of Xi’s signature corruption purges upon attaining high office, and will now be swept aside or will undergo rectification like Jack and Pony Ma (no relation).

In our view, this sort of blunt-edged reform has a mostly positive readthrough for global issues of economic and trade imbalances, technological growth, competition, and the environment. Xi’s personal power cult rightfully frightens Westerners with long memories, but the current path also augurs lower current account surpluses, less worker and environmental exploitation, higher wages, cleaner air, less monopoly power, and a more consumer-focused economy. China’s recent pledge to cut funding for overseas coal plants might presage stronger commitments at November’s COP26 climate conference in Glasgow. But greenery has a domestic focus as well; studies have found that air pollution is responsible for one million deaths per year in China. Cleaner energy and transportation provide huge public health benefits, and, intangibly, they are markers of human development that a middle class society demands. We have long argued for investing in the emerging market (and, a fortiori, the Chinese) middle-class consumer. Smaller companies focused on consumer welfare might well be the ultimate stock market beneficiaries of a reorientation towards “common prosperity.”

Investment implications

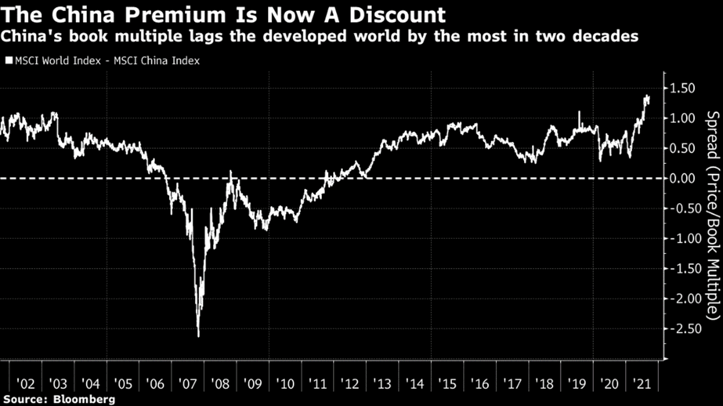

To a first approximation, China is now on sale. Chinese stocks today trade at the largest discount to the MSCI World since China joined the WTO. Nevertheless, markets hate uncertainty; the opacity and apparent caprice with which regulators have moved will not be salutary for multiples any time soon. If successful, deflating the property bubble will take years, not months. Long-term investors need not rush in.

In the bigger picture, the events in China serve as a wake-up call to U.S. investors. This is a political system and an economy that has few analogues in history, let alone in investors’ experience. The stock market upheaval ought to correct a basic asymmetry in how Americans get exposure to China. ADR’s that are not audited to the standards of American exchanges will be delisted, and the Chinese tech darlings whose stories were relatively easy for American investors and fund managers to grasp are now facing serious growth headwinds. Indeed, the concentration of Chinese tech leaders in EM indices had reached proportions similar to the S&P 500 in February, just before the stocks began to get punished. MRB Partners, a research firm, reported on February 11 that “[t]he top 10 individual stocks in the MSCI EM benchmark are being treated with FAANG-like reverence, and now account for more than 30% of the market capitalization of the benchmark (with the top six Chinese stocks accounting for nearly a fifth of the entire EM universe).”1 This extreme level of concentration is undesirable for investors seeking diversification, and was likely not the intended emerging market allocation. In the end, regardless of the authorities’ actions, there was too much faith being placed in just a few e-commerce, gaming, and social media business models. Goldman’s strategists recommend focusing on A-shares in industries aligned with China’s development objectives, including “hard” technology, renewable energy, and communications/digital infrastructure. Investors’ eyes should be on the medium- to long-term, and Chinese leaders helpfully announce every five years where they intend to take the economy. Don’t fight the PBOC or the CCP.

In the bigger picture, the events in China serve as a wake-up call to U.S. investors. This is a political system and an economy that has few analogues in history, let alone in investors’ experience. The stock market upheaval ought to correct a basic asymmetry in how Americans get exposure to China. ADR’s that are not audited to the standards of American exchanges will be delisted, and the Chinese tech darlings whose stories were relatively easy for American investors and fund managers to grasp are now facing serious growth headwinds. Indeed, the concentration of Chinese tech leaders in EM indices had reached proportions similar to the S&P 500 in February, just before the stocks began to get punished. MRB Partners, a research firm, reported on February 11 that “[t]he top 10 individual stocks in the MSCI EM benchmark are being treated with FAANG-like reverence, and now account for more than 30% of the market capitalization of the benchmark (with the top six Chinese stocks accounting for nearly a fifth of the entire EM universe).”1 This extreme level of concentration is undesirable for investors seeking diversification, and was likely not the intended emerging market allocation. In the end, regardless of the authorities’ actions, there was too much faith being placed in just a few e-commerce, gaming, and social media business models. Goldman’s strategists recommend focusing on A-shares in industries aligned with China’s development objectives, including “hard” technology, renewable energy, and communications/digital infrastructure. Investors’ eyes should be on the medium- to long-term, and Chinese leaders helpfully announce every five years where they intend to take the economy. Don’t fight the PBOC or the CCP.

We have spoken to some who wish to “divest” of China. It’s not an absurd question. Regardless of the size of its economy, if China is uninvestable for businesses and investors seeking fair treatment, rule of law, and respect for contracts, investors will make do without. Our take is that China still is “investable” and is likely to be more so in coming years. We believe that its growth will indeed slow as the country stutteringly transitions from middle to upper income. Its political economy is troublesome, but then so is the United States’.

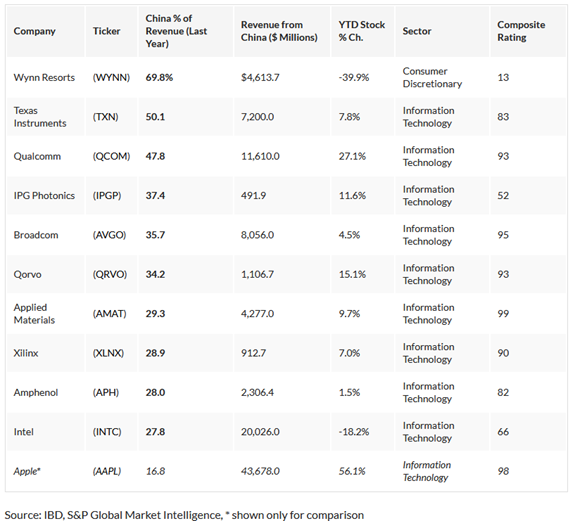

Further, divestment of all Chinese exposure is nearly impossible in a diversified portfolio. Revenue derived from China made up 2% of the total for the S&P 500, but that share is much higher for the largest firms. Apple reported almost 20% of its first quarter 2021 revenue coming from Greater China. And where China is not an end market, it is inextricably bound up in global manufacturing, shipping, and supply chains. In a 21st-century, interlinked, globalized economy, you cannot fully disengage from China, as recent American presidents have discovered. Viruses first discovered in Wuhan kill hundreds of thousands of Americans, and companies selling air conditioners “made in America” rely on vital inputs from Chinese suppliers. Such strategic Sino-American decoupling is only likely to provoke more rivalry and accelerate Chinese import substitution in high-tech industries.

S&P 500 companies revenue exposure to China; source: www.investors.com

We endorse the idea that investors, like manufacturers considering nearshoring or reshoring, should look to diversify out of China. In the short-term, many markets will be affected by machinations in Beijing. From Australia’s miners to New Zealand’s tourism industry, to intermediate goods suppliers in Indonesia, South Korea, and Taiwan, to German auto parts makers and French luxury goods brands, Brazilian and Chilean commodity exporters, global investors will need to watch the “common prosperity” agenda closely, whether they are buying Chinese shares or not. Volatility should rise.

Notwithstanding the dominance of Alibaba and Tencent, EM has always meant more than Chinese internet. Underweighting China’s index share makes more sense today than ever. But Western governments will need to engage with China on mutually important significant issues such as trade, capital flows, and climate change. China and the West can learn from each other’s experience combatting financial crises and tech behemoths. Equivalently, market participants must take stock of events in China to form inferences about the pace of global growth, the implications of deleveraging, and the consequences of taking on technology platforms. It is likely that many of the best performing investments of the next decade will be found in China, though they are less likely in the consumer internet or property development sectors. We must learn a lesson from Evergrande’s incipient crisis, one which has never been put better than by Herb Stein in 1986: “If something cannot go on forever, it will stop.”

Please See Our Important Disclosures

1 “Asian Outperformance Will Drive EM to Irrelevance,” MRB Research Report, February 11, 2021.