26 min read

Cash is once again king

- Resilience will be the key test of any investment strategy in a higher-for-longer regime.

- We expect markets to continue to care rather more than in previous years about tangible cash flows. As Rod Tidwell once said, “Show me the money.”

It’s the (real) economy, stupid

- The mood of the FOMC gets the headlines, but the path of interest rates and valuations depends on rent (dis)inflation, on wages, credit markets, on Vladimir Putin, and on China.

Stocks for the long-term, but at a reasonable price

- At 17.5x multiple of 2023 estimated earnings (a number likely to come down), the S&P 500 does not represent compelling value but does remain an unavoidable ingredient in a growth-focused portfolio.

- Investors focusing below the broad equity index level should be able find better opportunities in value, high-quality, and smaller-capitalization stocks. A relenting of the dollar’s multiyear rise should support international equities.

Looming valuation marks on private investments

- Although it’s impossible to know the size of mark-to-market losses awaiting investors in venture capital, private equity, and commercial real estate, we do see downside risk to those valuations.

- Opportunistic strategies, capital solutions, and loan-to-own strategies should provide interesting performance in the coming years.

- We remain on the lookout for smaller funds, with smaller deal sizes, and younger, hungrier management companies with proven expertise in actually running companies well.

2022: A year of investment detox

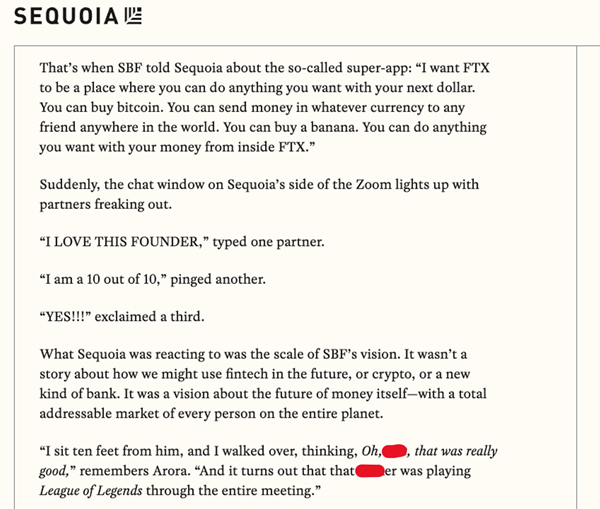

Source: Web archive of a profile of Sam Bankman-Fried posted, and withdrawn shortly thereafter, on Sequoia Capital’s own website.

When future market historians write the story of 2022, it will likely be twinned with its immediate predecessor, 2021. Fittingly, the all-time closing high price for S&P 500 index—to date at least—was registered December 31, 2021: 4,766. Lurking behind the champagne and party hats of that New Year’s Eve bacchanal, it was already evident that change was in the air. Two weeks earlier, at its December meeting, the Federal Reserve had committed at last to a policy of tapering asset purchases—a prelude, as it turned out, to the severest course of policy tightening ever experienced over a calendar year in the institution’s history. Some investors had been reading the inflation tea leaves; many of the riskiest assets had been in retreat since the summer.

Source: CrossBorder Capital

It is tempting to read 2022’s market turmoil as sequel to the speculative binge investors began shortly after policymakers determined to fight COVID-19 on the economic battlefield with an (apparently) limitless fusillade of stimulus measures. In this framing, 2022 is the year of payback, of predictable consequences, of post-bender hangover, of (liquidity) withdrawal symptoms, of the karmic return of economic orthodoxy. And indeed, we will describe it in precisely these terms, at least with respect to the sobering bath taken in 2022 by many of the wildest speculations on far-future profits. But the financial year marked a deeper transition as well, as we have written about elsewhere. Financial markets sometimes offer up paradigm shifts, inflection points where one prevailing backdrop of sentiment, of policy, even of physical market structure, gives way to another. In hindsight, 2000 was one such; 2008 was another. The lessons learned in one paradigm become deeply ingrained in a generation of investors; generally they fit poorly, if at all, to the subsequent years.

Though there are many head fakes and as many false signals as there are stock market shamans, and we ought to thus be humble about predicting turning points, we believe 2022 inaugurate such a new regime in market psychology and behavior. It takes place in an economic environment likely to be characterized by higher-than-desired inflation, hard tradeoffs, rangebound markets, and by a valuation climate that once again rewards commonsense and cynicism. As we review 2022, we might equally be looking forward to a period of time when getting rich in momentum stocks, in consensus trades, and in financial assets of dubious practical utility will remain much more difficult. One where patience, diversification, and an attitude of “show me the cashflows” will come back into vogue.

But before we steady ourselves and portfolios for this chastened reality, let us stop to rubberneck at a few wrecks along the road. It being December as we write, holiday over-indulgence just behind us and much journalistic ink already spilled on the subject, piling on the FTX debacle seems a touch hedonistic. But it will help us make a larger point… so here goes.

2022 dealt a harsh blow to the heedless momentum investor

Source: Miami Herald

Sam Bankman-Fried, whose cognomen “SBF” will probably enter the pantheon of initials parents try to avoid when naming an infant, is the poster-child for financial excess. But is he more bad apple or scapegoat? A penniless post-adolescent as recently as 2017, SBF is just the latest in a line of charismatic, media-savvy and ethically unconstrained tech founders happy to play merry havoc with investors’ dollars. The most interesting thing about the FTX scandal is its utter banality—in this case, the Pied Piper who’d dazzled journalists and investors alike stands accused of perpetrating a rather straightforward (and not particularly sophisticated) financial fraud. The important lesson in the excerpt at the top of this blog is not about FTX’s Ponzi scheme per se. It’s not a fable about hubris and nemesis, pride going before a fall, or even how the company may have debuted its own version of the “skyscraper curse” in securing naming writes for the arena of crypto’s hometown team, the Miami Heat. Rather, it’s about venture capital. It’s about how much of the vertiginous heights scaled by various financial markets in the wake of the pandemic have been primarily built up on storytelling, on mimetic (viral) narrative, on Greater Fool Theory, and on, as the dean of financial crisis economics Hyman Minsky would have it, “Ponzi finance.” The degree to which this diagnosis is true of the post-pandemic run-up writ large—the degree to which valuations were solely supported by a belief in perpetually zero interest rates—will tell us if, when, and how much asset prices will recover.

Sequoia is an object lesson, because the firm is the most prestigious, most sought-after, and arguably the best venture capital fund manager in the history of Silicon Valley, as described in detail in journalist Sebastian Mallaby’s recent hagiography, The Power Law (Editor’s note: it’s an excellent book, despite its relatively uncritical treatment of Sequoia). Notably, the partner who led the FTX investment was Alfred Lin, who as recently as 2021 topped Forbes’ ranking of venture capital superstars, the Midas List. Sequoia wrote off the entirety of its $213 million stake in FTX, and has since apologized to fund investors, promising to return to old-fashioned standards of due diligence such as requesting financial statements.

Sequoia and Lin did not in 2022 suddenly cease to be great investors. Any of us would be lucky to be limited partners of theirs. For them to have made such a facepalming investment mistake demonstrates how easy it is for anyone, in raging bull market, to relax risk controls, to “ape in,” and to follow the crowd—even as it heads over the cliff. We must all (and we are all guilty!) use this moment to remember the value of those formal structures that keep us from veering off plan: consistent, rigorous process, a relentless, stubborn focus on the long term, and—wherever we can summon it—a contrarian temperament born of distrust of grand narratives. Risk management is the practice of formalizing these behaviors, and it will often cause us to steer well clear of seasonal fashions or new ways to get-rich-quick. While such phenomena may mint multimillionaires of our friends and neighbors, they may likewise be (as they were on December 31, 2021) on the precipice of freefall.

Just as 2021 pushed to the fore no end temptation, 2022 equally offered many flavors of revulsion. The headlines teemed with takedowns, morality plays, and parables of the proud laid low. In fact, much of the rocket-fueled “wealth” creation of the past two years represented some species of gaseous hype: what follows is an abbreviated inventory of some of the more sensational post-pandemic can’t lose, “buy-the-dip” trades that were taken behind the woodshed this past year.

Source: Michael Novogratz @novogratz on Twitter

At the outset, we would emphasize that we do not wish to cast aspersions on investors in assets that went down in 2022. Above all, it would be hypocritical and invite the investment gods’ wrath to adopt a triumphalist tone in a market where everyone’s portfolios were down. Many investors deploy a small portion of their portfolios to more speculative ideas—a “lottery ticket” model of portfolio construction, if you like. This is reasonable and rational, if sized correctly. The point we wish to make when surveying 2022’s wreckage is just that the year should serve as a reminder not to become overly caught up in manias. When, as in 2021, everything is going up, the barmier the better, it is the time to carefully review and possibly pare back the size of these lottery tickets.

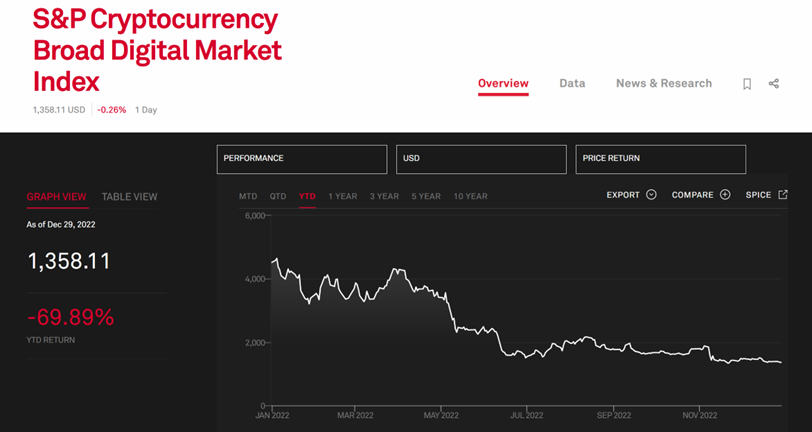

First, most salaciously, must come the industry for which SBF purported to be reputable spokesman: cryptocurrency. FTX was valued in October at $32 billion. By November it was worthless. Over the past year, the market value of cryptocurrency assets collapsed from $3 trillion to about $850 billion. Bitcoin—the original and best-known cryptocurrency—plunged from $68,000 to $17,700, so-called “algorithmic stablecoins” such as TerraUSD broke their peg and collapsed, and crypto lending platforms such as Celsius went bankrupt. Celebrity endorsers received letters from the SEC. Generically, a dollar invested in crypto at the end of 2021 was worth roughly $0.30 at the end of this year. Most were worth much less.

We looked for a chart on the performance of crypto’s most fantastical avatars, non-fungible-tokens or NFT’s. To the best of our ability to tell, the leading index (“NFTI”) was discontinued in September—felicitously, as it was on a trajectory to zero.

Source: Coinbase

On to more prosaic financial assets. After crypto, the investment trend that implicated the greatest number of celebrity shills was that of the Special Purpose Acquisition Vehicles, or SPACs—to be kind, a form of regulatory arbitrage with hugely misaligned incentives that served largely to encourage public investment in profitless companies. Sidenote: when a tabloid-baiting celebrity promotes a financial investment, it’s probably wise to hold tight to your wallet.

The SPAC washout appeared to have crested by midyear. Not so: in December, the collapse reaccelerated to the surprise of many who had forgotten that there were still herds of zombie vehicles in search of acquisition targets they would never find.

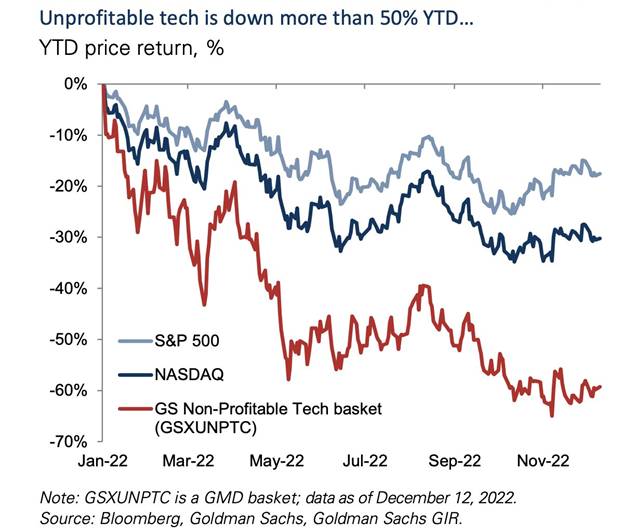

Speaking of profitless companies, the rise and fall of Goldman Sachs’ “Non-Profitable Technology Basket” rings with eerie echoes of the Nasdaq bubble and collapse of 1998-2000. The IPO and SPAC boom that brought public investors the opportunity to invest in such companies as Nikola—the electric truck-maker without a product—or the aptly-named e-scooter startup Helbiz (stock currently at $0.13) calls to mind the era of Pets.com and Webvan.

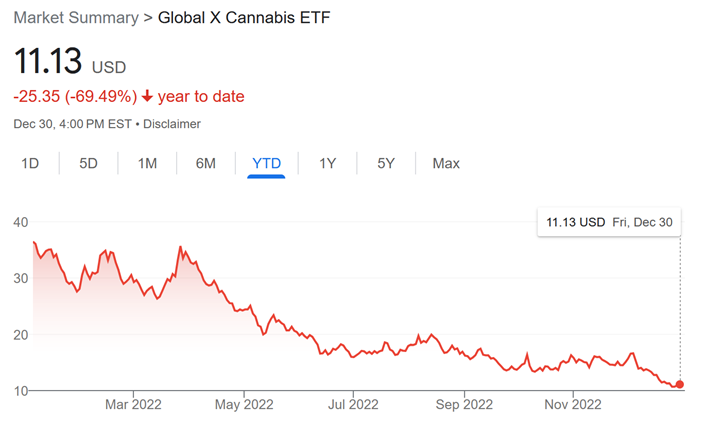

In 2021, investors exhibited reefer madness for cannabis stocks. Makes sense—these companies at least had a product, and an addictive, newly legal one at that. What they didn’t have was profits. Investors in a popular index of these stocks also lost 70%.

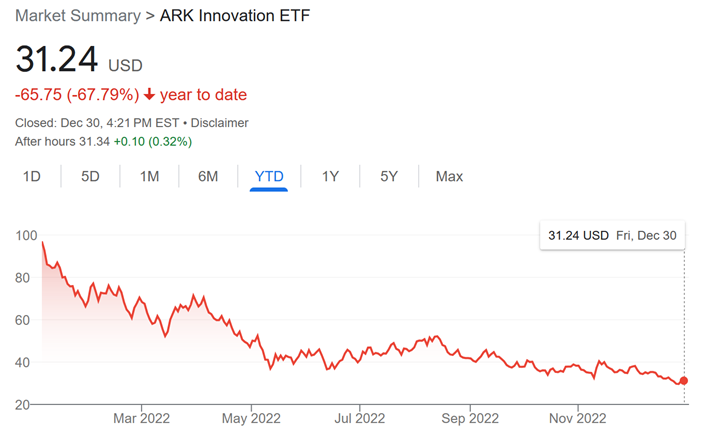

The most famous oracle of “disruptive technology” during the boom was frequent television guest Cathie Wood. Depending on who you ask, she is either a visionary investor or a visionary self-promoter. Like many lightning-rods of the last half decade, she rode to fame on a populist message. Either way, 2022 saw her flagship product give up all of its pandemic-era gains. As is so frequently the case in momentum investments, more dollars were lost in the crash than were ever made in the rise. This was already true in 2021. In 2022, Ark Invest lost another 68%.

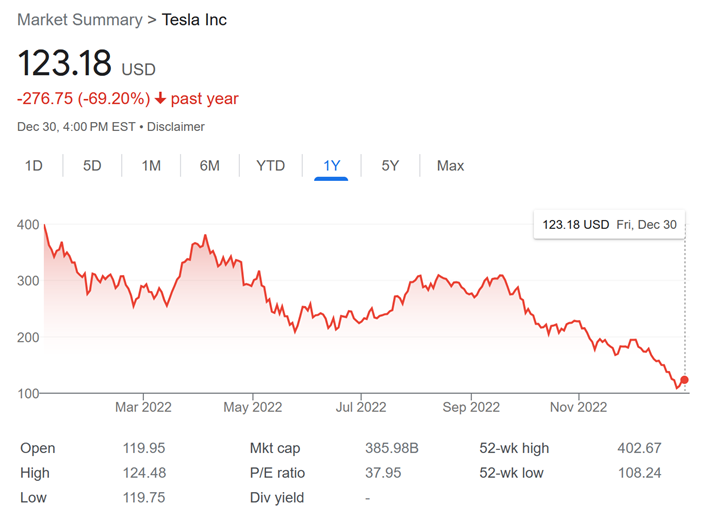

In 2022 Cathie Wood managed to outperform “stonks” such as AMC Entertainment (down 84.6%) and Clover Health (down 77%), though original memelord Gamestop (down only 51.7%) eked out a narrow victory. The largest beast aboard the ARK was undoubtedly Elon Musk’s Tesla, which weighed down Wood’s fund by losing 69% and wiping out over $1 trillion in market cap (and the wealth of countless first-time investors) while its CEO busied himself with a very expensive hobby of making off-color jokes and otherwise stretching the limits of civil discourse. As a reminder, when an asset falls 70% in value, it must return 233% to recover its previous high. Under the most optimistic scenario, for Tesla, Bitcoin, ARKK, or pot stocks, it will take several years to regain those 2021 peaks.

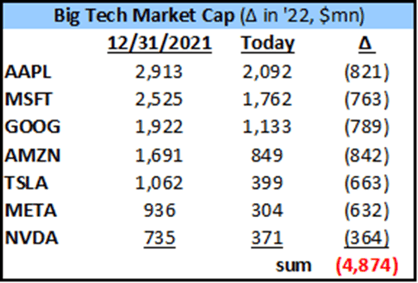

To reiterate, we do not relate any of these tales to finger-wag or cluck at the naïveté of novice investors. For one, Tesla was hardly alone. Large-cap U.S. growth equities, the best performing investments for most of the past decade, have, with few exceptions, fallen from grace.

Source: Goldman Sachs

Furthermore, year-to-date losses are unrealized for many and percentage returns are of highly sensitive to start- and end-dates. Crypto has been down before and may soar again. Earlier investors in Tesla, Bitcoin, and Sequoia Capital’s funds are sitting on large gains, even if they exited today. And after all, the safest, boringest asset class in the world, U.S. Treasuries, lost more than 16% in 2022, punishing even the most staid portfolios. Volatility hedge, bonds were not. This was, incidentally, the worst calendar-year experience bondholders have endured in recorded history. Many asset allocators look foolish compared to the seemingly clairvoyant Hindsight Capital portfolio.

No, we only wish to underscore the point that a mentality of “what goes up must go further up” is very dangerous to the long-term performance of investment portfolios, and that all of us—retail and professional alike—must guard against this mistake. However disciplined we imagine ourselves, without a contrarian streak and certain formal risk management brakes, it is only too easy to allow the fear of missing out to trick us into a belief that social proof constitutes adequate due diligence, that newfangled, unregulated financial products offer true diversification, or that simple rules—whether “HODL” or "the 60-40 portfolio"—provide the last word in portfolio strategy.

If our hypothesis is correct and 2021 was the apotheosis of such thinking, drenched now in the cold shower of rate hikes and quantitative tightening, it will certainly be back again to tempt us into unprofitable speculations we cannot yet imagine. We must build from here. All who owned large-cap stocks suffered major setbacks in the last year. At 17.5 times next year’s estimated earnings (a number likely to come down), the S&P 500 does not represent compelling value but does remain an unavoidable ingredient in a growth-focused portfolio.

Venture capital and “the bezzle”

"Alone among the various forms of larceny [embezzlement] has a time parameter. Weeks, months or years may elapse between the commission of the crime and its discovery. (This is a period, incidentally, when the embezzler has his gain and the man who has been embezzled, oddly enough, feels no loss. There is a net increase in psychic wealth.) At any given time there exists an inventory of undiscovered embezzlement in—or more precisely not in—the country’s business and banks.…

"This inventory—it should perhaps be called the bezzle—amounts at any moment to many millions of dollars. It also varies in size with the business cycle. In good times, people are relaxed, trusting, and money is plentiful. But even though money is plentiful, there are always many people who need more. Under these circumstances, the rate of embezzlement grows, the rate of discovery falls off, and the bezzle increases rapidly. In depression, all this is reversed. Money is watched with a narrow, suspicious eye. The man who handles it is assumed to be dishonest until he proves himself otherwise. Audits are penetrating and meticulous. Commercial morality is enormously improved. The bezzle shrinks."

John Kenneth Galbraith, The Great Crash of 1929 (Mariner Books)

Looking forward, the appropriate response to a year of reset expectations such as 2022 is to examine our portfolios’ resilience to a less forgiving, more tumultuous economic conditions, should these stick around. What investments do we still own that may bear the original sin—and the valuation methodology—of zero-interest-rates-forever thinking?

Does commercial property unwind years of gains as cap rates fell in tandem with risk-free rates, or can real estate investors successfully kick the can until discount rates reset again lower? Does the banking system continue to finance leveraged purchases of office buildings, money-losing companies, or even private second homes? Can the best performing asset class of the post-GFC period, venture capital (exemplified by Sequoia), continue its heady gains?

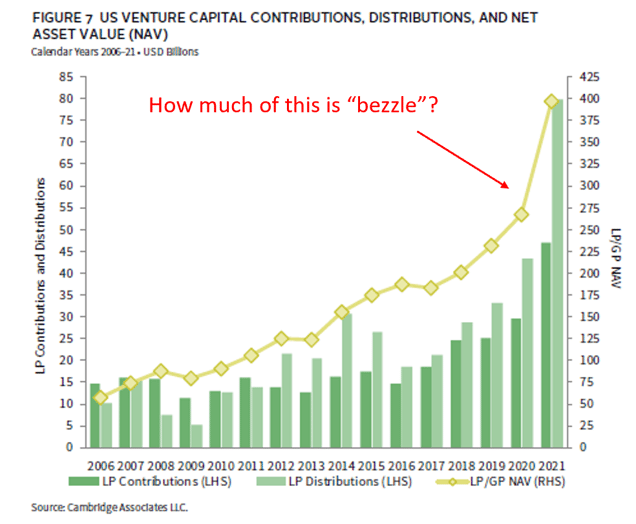

Let us pick on venture capital for a moment longer since it represents an extreme illustration of a more widespread phenomenon. We began this piece with a vignette, a slightly embarrassing bit of publicity for Sequoia. We end it with a quote from the great observer of markets and wit, John Kenneth Galbraith. What strikes us as most underappreciated detail in the FTX saga is the fact that it is a salient example of Galbraith’s “bezzle”—money that has been stolen, but whose victims don’t yet realize it, and thus it is double-counted by both the thief and the prey. Sequoia and its investors felt very rich indeed when FTX was valued at $32 billion. When Sequoia led the crypto exchange’s enormous Series B round in 2021, its valuation was $18 billion. The investment was showing a 78% gain in little over a year.

Now, many seasoned venture investors are sitting on appreciated portfolios (funds’ “net asset values”) that show similarly intoxicating gains. But, as venture capitalists are learning, it’s risky to get high on one’s own supply. Venture capital funds often arbitrarily and almost unilaterally set valuations of portfolio companies in the absence of arm’s-length price discovery. Prices of marked-up companies have not been driven by cashflows, but by other venture capital investors deploying recently raised funds into later rounds. The NASDAQ technology index was down almost 40% in 2022. Venture capital portfolios? Not so much. There are hundreds of billions of dollars of assets, many of them de-horned unicorns, awaiting a mark-to-market. True, this rinsing might never come, and venture capitalists and other private equity barons have little reason to increase the apparent volatility of their limited partners’ holdings.

Source: CNBC

Unless, that is, that value has already been stolen, or otherwise destroyed. One might wake up one day and find that a portfolio company’s assets are effectively uncollateralized loans to itself, that it just rolled its high-tech electric truck down a hill, or that it was literally using your money to buy back its own merchandise. Often it’s simpler: companies that crossover investors become unwilling to finance at higher and higher valuations sometimes just run out of cash.

The last tech bubble and collapse gave rise to numerous high-profile corporate frauds and bankruptcies that had exploited both the gullibility of investors and the laxity of some accounting rules. That market crash, and the financial crisis that followed less than a decade on, each led to new regulation and consumer financial protection—for good and ill. This time is likely to be no different. With the blowups of FTX, Terra/Luna, and Celsius, we have probably only seen the tip of much larger iceberg. The tech founder-VC-institutional investor group hug shares all the same perverse incentives and conflicts of interest that led to the 2000 crash, but today many more billions of dollars sit in private equity funds, outside the scrutiny of regulators. As the Financial Times writes, “[h]ating Cathie Wood’s Ark and loving venture capital seems intellectually inconsistent.” We agree to the extent that venture capital pursues a valuation-be-damned, growth-at-all-costs strategy. It’s impossible to know if there are large mark-to-market losses awaiting investors in venture capital, private equity, and commercial real estate. By exercising discretion, high levels of counterparty due diligence, and measured deployment across multiple vintage years, investors will likely be spared much of the nastiest shocks.

The last tech bubble and collapse gave rise to numerous high-profile corporate frauds and bankruptcies that had exploited both the gullibility of investors and the laxity of some accounting rules. That market crash, and the financial crisis that followed less than a decade on, each led to new regulation and consumer financial protection—for good and ill. This time is likely to be no different. With the blowups of FTX, Terra/Luna, and Celsius, we have probably only seen the tip of much larger iceberg. The tech founder-VC-institutional investor group hug shares all the same perverse incentives and conflicts of interest that led to the 2000 crash, but today many more billions of dollars sit in private equity funds, outside the scrutiny of regulators. As the Financial Times writes, “[h]ating Cathie Wood’s Ark and loving venture capital seems intellectually inconsistent.” We agree to the extent that venture capital pursues a valuation-be-damned, growth-at-all-costs strategy. It’s impossible to know if there are large mark-to-market losses awaiting investors in venture capital, private equity, and commercial real estate. By exercising discretion, high levels of counterparty due diligence, and measured deployment across multiple vintage years, investors will likely be spared much of the nastiest shocks.

What we are sure of is that the speed of the recent valuation ascent will not be repeated. IRR’s a standard deviation or two above the historical mean will not be sustained. Indeed, in venture capital, the performance of what ought to be the longest duration asset class came was lately driven by one factor above all—speed. Faster-and-faster mark ups, new “crossover” investors such as Softbank, Tiger Global, and Fidelity piling into swollen late-stage rounds, 48-hour turnarounds for term sheets, etc. Velocity became the new leverage. This was all eminently unsustainable of course. So were the returns that investors enjoyed for a few years at the tail-end of the boom. FTX should have removed the scales from our eyes, along with the halo from around venture capital’s exalted brow.

Lessons and warnings from the real economy

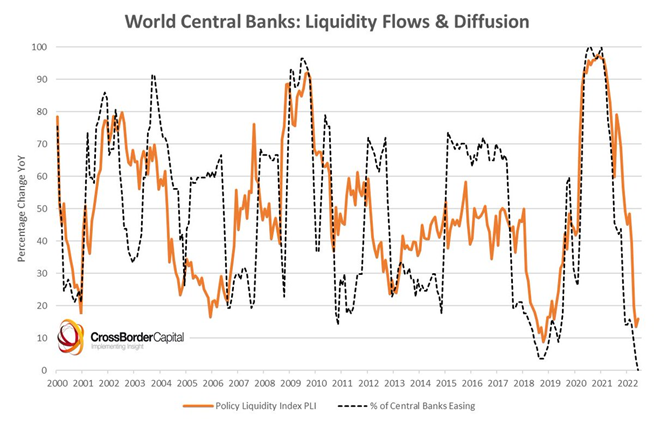

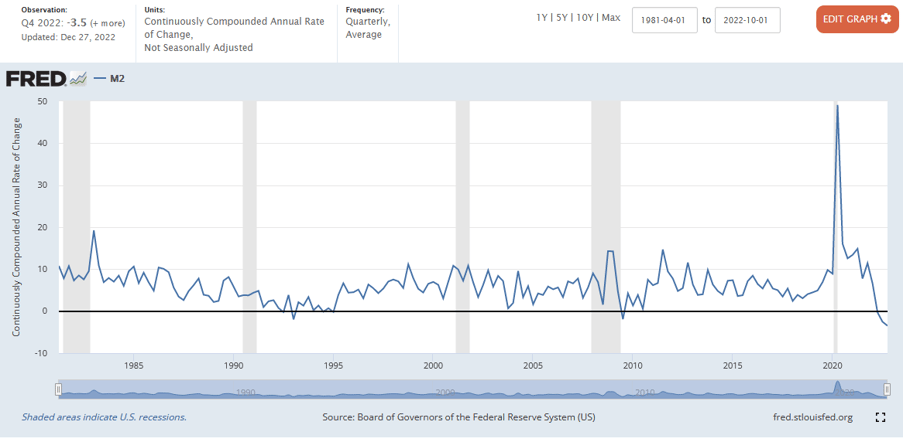

We clearly remember in the aftermath of the GFC a chorus of naysayers insisting that interest rates were just about to normalize back to a longer-term equilibrium level of, say 5% or higher. This was the average level these investors had experienced in their careers, mostly dating to the beginning of the great bond bull market in the 1980’s. They were of course, wrong. They were also wrong to assume that quantitative easing would inevitably produce inflation. What the Cassandras missed, as we’ve written before, was the spectacular collapse of interbank lending and private money (AAA-rated securitized assets) which together created a massive hole the Fed and its companion central banks only partially filled with new reserves. Aggregates of the “broad” money supply, despite all the money-printing, grew only steadily when measured against longer time-scales—and certainly when compared to growth in the overall economy. Private money disappears, QE takes its place. Fiscal austerity partners with monetary stimulus. Disinflation ensues.

Observe the following chart, which describes annual growth rates in the broad money supply. Notice any unusual bulge around 2009-2013? Neither do we. What about coming out of the pandemic? Similarly, the decline in 2022 appears without precedent in the data series. These sorts of liquidity changes can be effective predictors of valuations in financial assets.

Today a new generation of investors, weaned on a lower-for-longer, disinflationary decade, waits in expectation of another inevitable normalization of interest rates—in the other direction. Surely, 4% Fed Funds or 7% 30-year mortgage rates are aberrant. Let us hold our private portfolio marks at 2021 levels while all this chaos settles out. Will interest rates eventually reset, bailing out unrealized investments that we made when the yield of the long bond was measured in tens rather than hundreds of basis points? Perhaps. But it is not inevitable. Whether such a normalization happens depends not on the mood of Jerome Powell, but on the macroeconomic and geopolitical backdrop—on rent inflation, on the labor market, on the decisions of local bank credit officers, on Vladimir Putin, on China’s Politburo. In short, on the real economy and the real world.

Will the tightening of the monetary taps result in disinflation, perhaps supporting higher valuation levels going forward? Likely it already has, as U.S. inflation seems to have peaked before October. This should not be read as an “all-clear” for risk assets, however, since the Fed’s actions have tightened conditions to the point where housing starts and new mortgage applications are plummeting, yield curves are inverting (these events have been historically Delphic recession forecasters), and corporate earnings estimates are shrinking fast. Inflation will come off the boil, no doubt. But many of the secular forces that kept inflation low—weak worker bargaining power, globalization and global labor arbitrage, labor-substituting automation, and miserly levels of fixed investment look to be either decelerating or going into reverse. Retirements, reduced immigration, changed fiscal priorities, and governments’ renewed focus on antitrust, climate, and inequality could all well conspire to keep equilibrium inflation—and policy rates—much higher than we became used to in the teens.

A tentative outlook—if we dare

The key to investment strategy in years forward will be to determine if monetary tightening has been sufficient to cause a recession. The shift from inflation risk to recession risk reflects the sudden about-face of global central bankers, who as recently as Summer 2020 were meeting to announce new, more tolerant attitudes toward inflation. The timing of this was a strategic error, one the Fed seems determined to redress. Even with inflation starting to moderate (at least in the U.S.), there is no guarantee that central bank policy rates will follow suit. In fact, in November, Fed Chair Powell conveyed that rates are likely to remain higher-for-longer, posing a continued headwind to both financial markets and the economy.

It has been a very long time since nearly anyone has liked bonds as an investment, but 2023 may be the year that they come back into fashion. After a decade of low yields followed by a brutal drop in prices during 2022, risks and prospective returns (both yield and price) in the fixed income market are now more balanced. It's nevertheless likely to be a bumpy ride.

The backdrop for public equities in 2023 will be somewhat better than in 2022, given reduced starting valuations, potential valuation support from moderating inflation, and—at some point—a temporary pause in Fed rate hikes. It will still be a challenging year ahead. The overall earnings cycle is decelerating, but there are some notable divergences across sectors, reflecting excesses still not entirely worked out by the air pockets hit in 2022. Investors focusing below the broad equity index level should be able to find better opportunities in value, high-quality, and smaller-capitalization stocks. Furthermore, some long-awaited respite from the relentless rise of the U.S. dollar as global central banks catch up to the Fed’s hawkishness could lend support to international equities. There has already been a marked shift in relative strength over the past two months, with global ex-U.S. equities significantly outperforming domestic stocks, a trend that current valuations suggest has much room to run. But beware the dollar smile; a global recession will not favor investors in overseas assets.

In private markets, we are very constructive on opportunistic credit; the receding tide of liquidity will give lenders the ability to invest at much lower valuations, with greater spreads, and, importantly, better structural protections. For existing portfolios of loans, there is likely a credit cycle coming. Much of the growth of the private credit landscape in the last several years could be described as “froth” with inflows and AUM growth loosening standards. As ever, when choosing your private investment partner, discretion is the better part of valor. In credit perforce downside protection is the name of the game.

Private real estate investment suffers (benefits?) from the lagged reporting and the slow valuation adjustment cycle referenced above. Generally, we have favored the most resilient and safest assets with the best economic tailwinds. These property types—high quality multifamily and industrial—are also the priciest and most at risk of a valuation correction. It has not happened yet. A popular public REIT ETF (the Vanguard Real Estate Index Fund) was down 28% in 2022. While private fund structure gives some real estate managers the advantage of long-term time horizons and the benefit of illiquidity, private managers must still provide regular valuations of the underlying assets and we see downside risk to those valuations. What private structures can also do is enforce a longer hold period (both for managers and investors), which disciplines us both to invest predominantly for real cashflows rather than a hoped-for appreciation “pop.” Hence, we believe we have avoided improper levels of leverage and egregiously overvalued assets. Cashflows, especially in the multifamily and industrial sectors, remain resilient. Real estate is an inflation-resistant asset class. But it is also financed with copious (often floating-rate) debt and is therefore sensitive to interest rates. Time will tell. Special situations, developer takeouts, and loan-to-own strategies should provide interesting performance in the coming years.

Enough ink has been spilled about the structural issues with private equity or whether it truly outperforms a fairly constructed public equity benchmark. We have certainly been happy to poke fun at the venture capital elite. Even if the entire private equity industry is not a pyramid scheme, it is certainly a pyramid – with massive fundraising capacity at the top and a very long tail of smaller outfits at the bottom. There’s little doubt that the broader market will have to grapple with drooping company valuations and more expensive debt in 2023. Many of the largest leverage buyouts are already experiencing distressed or hung financings. We remain on the lookout for smaller funds, with smaller deal sizes, and younger, hungrier management companies with proven expertise in actually running companies well. The colossal amounts of dry powder that have accumulated at the top of private equity’s inverted pyramid imply that those with the ability to buy companies (moderately) cheaply, drive operational improvements, and position those assets for sale to a rapacious megafund should be able to make money in spite of—or perhaps especially in the present market environment.

Source: S&P Global Ratings

As a coda to this gloomy and occasionally snarky discussion, we are more convinced than ever that a certain skepticism around investment fads, clichés, or anything that promises a quick buck is in order. 2023 may prove to be easier on portfolios than 2022, but we continue to anticipate rough and unforgiving terrain. Speculative excess must and will, for a time, give way to more hard-headed analysis of both tangible return-on-capital and return-of-capital. If next year’s hindsight confirms that 2022 did in fact mark a permanent sea-change, a paradigm shift in capital markets, we expect resilience to be the operative test of any investment strategy under the emerging regime.

Related Posts

Middle Market Private Equity: The Art of Picking Your Spots

In our last entry, we wrote that inflation and monetary tightening were returning investors to a...

Darkest Before the Dawn

Key Points

- The pathway to a sustained, durable recovery in 2021 is now far clearer than it has...

Scarcity

As we write today, the surge in energy costs and consumer prices everywhere looks set to drag on...