17 min read

In our last entry, we wrote that inflation and monetary tightening were returning investors to a world where capital and liquidity are more precious. Building portfolios to endure in this market involves hard choices and tradeoffs which necessitate a high degree of selectivity. One choice that has appeared relatively easy is to allocate away from public markets and into private ones. Private equity returns beat public markets (especially when stock markets are plunging!) while sparing investors the daily volatility. What’s not to like?

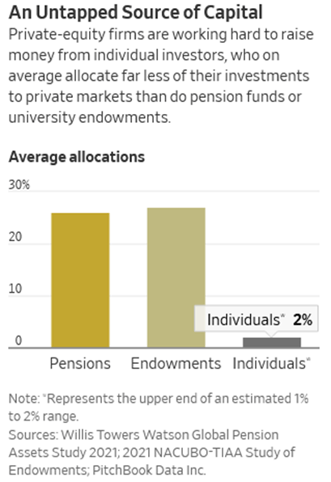

Wall Street has certainly spied a sales opportunity. Large private equity firms and intermediaries have raced into the retail channel, barraging private investors and wealth advisors with advertisements recommending this exact trade. The CEO of one large aggregation platform called private equity’s retail push a “land grab,” likening it to “the mutual fund boom 2.0.” While rising interest rates cause investors to dump both stocks and bonds, flows to large private equity firms are accelerating; Blackstone is seeing $5 billion in retail inflows a month; Carlyle gets up to 15% of its funds from individual investors, while KKR is targeting one half. The rest of the industry has taken notice: fully a third of private capital managers anticipate launching a retail-focused vehicle within five years.

As ever, when Wall Street starts spinning up its marketing apparatus, skeptical investors should wonder whether the product is primarily being bought or sold. The benefits of “private equity for the masses” are likely to accrue more to private equity than to the masses. “For the private-equity industry to keep growing, you’ll need more access to the retail investor,” one consultant says bluntly.

For more seasoned private equity allocators, such rapid increases in capital bear scrutiny. Where fast-money retail flows go, disappointing returns often follow. Call it the dollar-weighted return effect; early investors may make a killing, but the average dollar invested in a hot strategy fares far less well. Two-thirds of institutional investors polled by the private equity secondaries firm Coller Capital worried that tourists to the private markets pose a risk to future returns. Private equity has had a very good three decades. Maybe it’s time to cut bait?

Source: Wall Street Journal

The PE stampede and the risk of disappointment

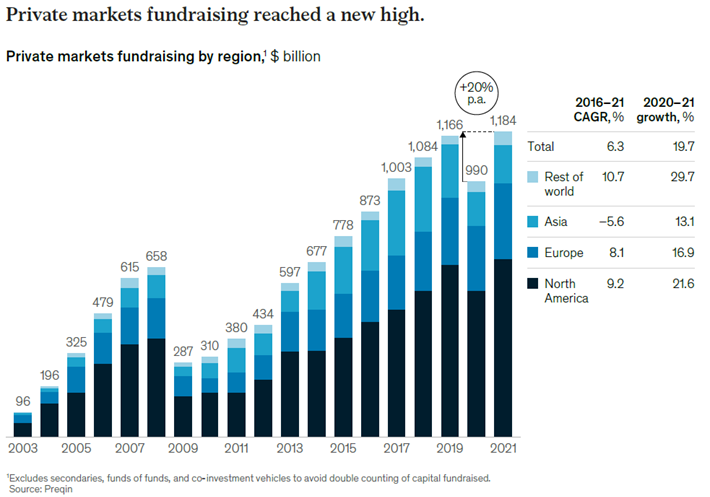

Higher interest rates signal a higher opportunity cost for investable funds. This, in turn, means higher required returns. If a safe bond is yielding 4% for 10 years, private equity with its concentration risk, leverage, and illiquidity needs to deliver far in excess of that. At the same time that global costs of capital are rising, the influx of dollars into private markets will mechanically depress expected returns for these asset classes. PE fundraising trends are therefore diametrically at odds with the asset class’s promise of better risk-adjusted performance. Investors allocating to private managers need to choose carefully.

Source: 2022 McKinsey Private Markets Annual Review

PE has seen very good times during the long boom. Some skepticism is therefore warranted about whether the perceived outperformance will last or whether it ever existed in the first place. Further, investors hoping to escape market melodrama by hiding out in illiquid assets may not be getting the safety they bargained for. It can be debated how much of the last decade’s private equity bonanza is attributable to steadily rising valuations across all risk assets, to increased leverage and cheap debt, to new and faster inflows of capital, or to all of the above via the innovative use of subscription lines. But surely private equity has been the beneficiary of most of the same forces that have worked in favor of the stock market. In the language of the trade, private equity has beta. Or, in other words, the respite that many investors are seeking from the volatility of public markets is partly illusory.

The following charts demonstrate unambiguously how the ride up in valuations that has flattered the performance of a generation of PE managers has been pretty unidirectional since 2009—until, perhaps, 2022.

Source: J.P. Morgan Guide to Alternatives Source: Pitchbook

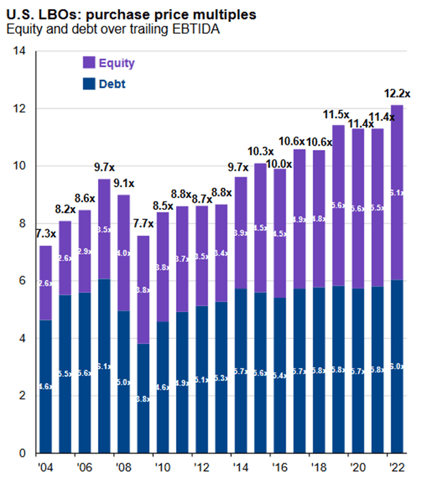

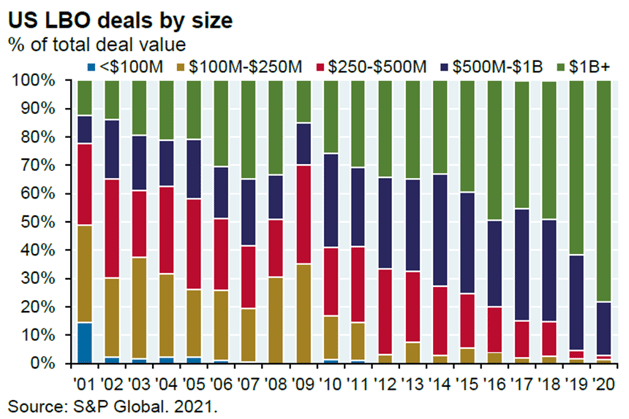

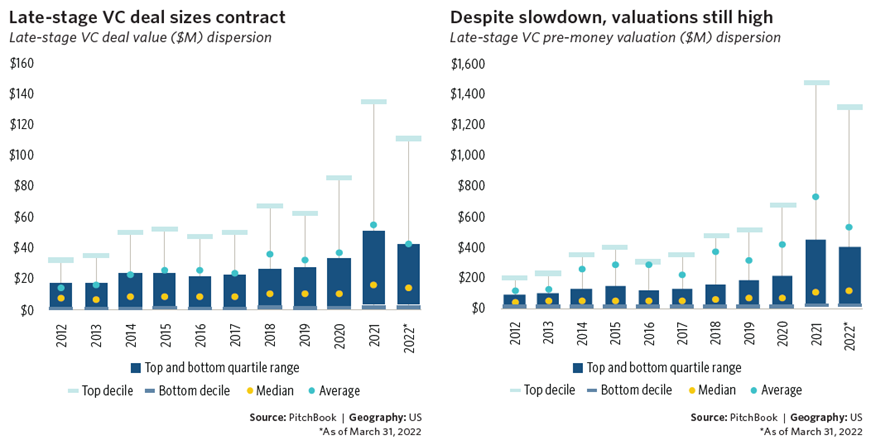

The natural consequence of bloating assets under management and steepening valuations is bigger deal sizes. The proportion of private equity buyouts with enterprise values (equity + debt) larger than $1 billion has more than doubled since 2014. Swelling funds have deployed more capital with more debt in order to swallow bigger and bigger companies. Both as starting valuations grow and deal sizes get larger, expected future returns should mathematically drop. This is to say nothing of the risks associated with leverage ratios north of 6 times, a level that would have seemed almost irresponsibly risky just a few years ago, and was, last year, the average. The same trend of splashier and more creative financing can be seen in late-stage venture capital, where the influx of “crossover” investors such as hedge funds and open-ended mutual funds, along VCs’ new “growth” funds have seen Series D fundraising rounds surge into the hundreds of millions, valuing scores of profitless pre-IPO companies at more than $1 billion. What was once so rare as to be called a “unicorn” now roams in herds numbering over 1,000.

Source: JP Morgan

Source: Pitchbook 2002 US VC Valuations Report

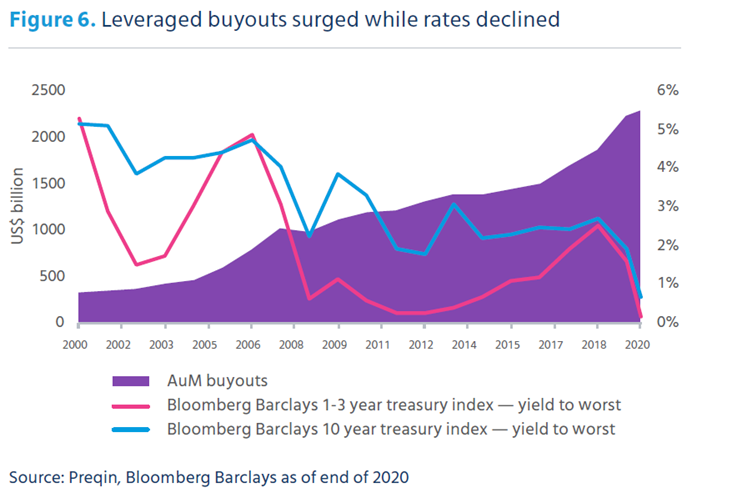

This constantly inflating valuation bubble has sprung from numerous sources—not least abundant inflows of capital and shorter deployment schedules. But, undeniably, a decade and a half of low and falling inflation have the largest role to play. By consensus, the paradigm shifts underway today in global capital markets imply that such a one-way ticket is no longer a safe bet. The below chart from Mercer shows the rough correlation of assets under management in the leveraged buyout (LBO) industry and trends in interest rates.

Source: Mercer

Rising rates have already crushed valuations in public markets this year, with the tech-heavy NASDAQ 100 index collapsing from 30 times at year-end to 22 times today. Interest rates have a less perceptible and less immediate but no less dramatic impact on private markets. Venture capital assets derive most of their value from long-term expectations for revenue and earnings growth and are thus highly sensitive to changes in the discount rate used to set valuations.

Equally, increased borrowing costs and scarcer debt finance will force buyout firms to adjust their models. One study found that most buyout firms double the amount of leverage on a company’s balance sheet. This borrowing is almost always done with floating-rate debt. The data provider Pitchbook writes that, at today’s rates, the average 6x PE leverage ratio equates to 3x interest coverage. If rates rise in line with market expectations, this coverage will fall toward 2x by the end of 2022. Should the economy enter recession this year or next, a 2x coverage ratio leaves little room for error with interest payments soaking up an increasing share of revenues and may lead to debt covenant violations or refinancing difficulties. There will be no alternative but for valuations and purchase multiples to come down.

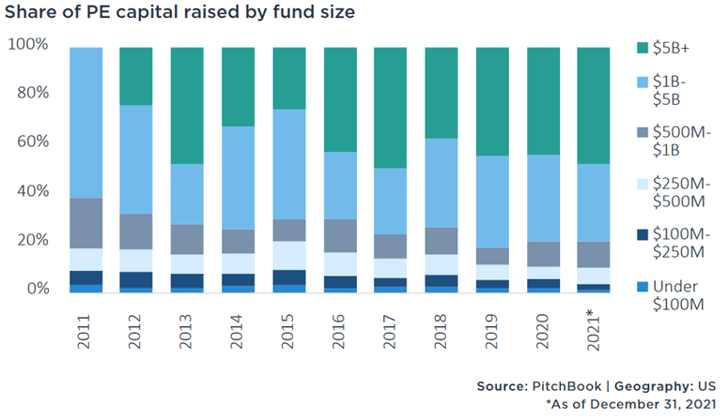

With such a gloomy outlook for the basic calculus of private equity returns, it’s easy to see ordinary investors’ rush toward illiquid markets as naïve or worse. Yet we believe that some of the most interesting and appealing opportunities available today can still be found in private equity. The reason for this apparent paradox comes down to the tremendous dispersion in PE manager performance. Measures of dispersion—for example, the range between the first and last quartile—have lately been coming down, but we expect them to increase again as higher rates and a weaker macroeconomic backdrop begin to bite. As we’ll explain, highly selective investors may have the ability to take advantage of a significant and (we believe) widening performance gap between the best smaller-sized funds and their mammoth siblings. Very large funds have disproportionately been the recipients of the flood of cash bestowed by public market refugees. In important ways, we view these megafunds as little more than public markets camouflaged in private market clothing. Let’s explore why.

A way forward – small funds, small deals, and selling up the food chain

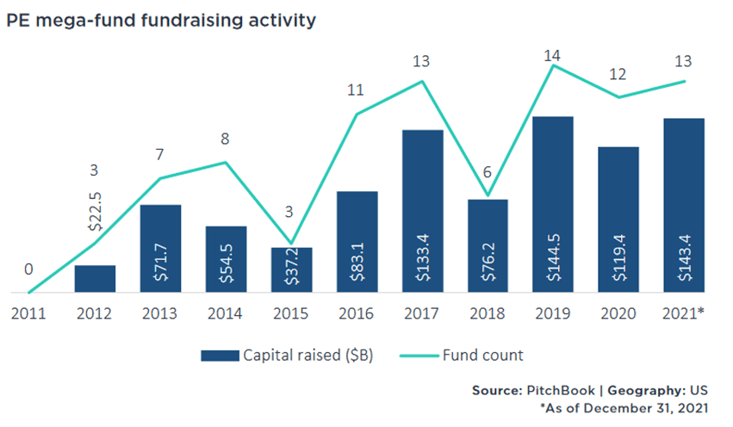

First, we need to examine who is gobbling up the majority of the newfound interest in private markets. As mentioned above, large firms like Apollo, KKR, Carlyle, and Blackstone, along with their merchandising partners like iCapital and CAIS, have made a deliberate pivot toward the high net worth private investor. Their active marketing push has borne fruit. These firms have amassed huge sums in their flagship funds—the vehicles that are routinely writing $1 billion buyout checks. Over the past several years, roughly half the capital raised by all private equity has concentrated in megafunds larger than $5 billion. About 80% goes to funds over the $1 billion mark.

Again, to quote Pitchbook:

Again, to quote Pitchbook:

Public PE firms… continue to break their own records at a rapid pace thanks to their growing flagship buyout funds, launches of new strategies, and scaling of other current strategies. Blackstone (NYSE: BX) is expected to raise more than $30 billion for its next flagship PE fund, surpassing Carlyle Group’s (NASDAQ: CG) $27 billion target for its 13th flagship fund earlier in 2021—both funds would set a new highwater mark… Apollo Global Management (NYSE: APO) will likely raise more than $25 billion for its next flagship buyout fund, which is expected to formally launch Q1 2022. Other players, such as Advent International and Vista Equity Partners, are setting similarly stunning targets for their next funds, which will help mega-funds achieve an incredible fundraising year in 2022.

These record-breaking fundraises are also coming faster and sooner than previously witnessed. The software buyout firm Thoma Bravo has earmarked $22 billion for its latest flagship fund less than a year after closing on $17.8 billion in its predecessor. Blackstone recently brought in a director from General Atlantic to launch a growth practice: its inaugural fund raised $4.7 billion in 2020, and it is now seeking $10 billion for its successor.

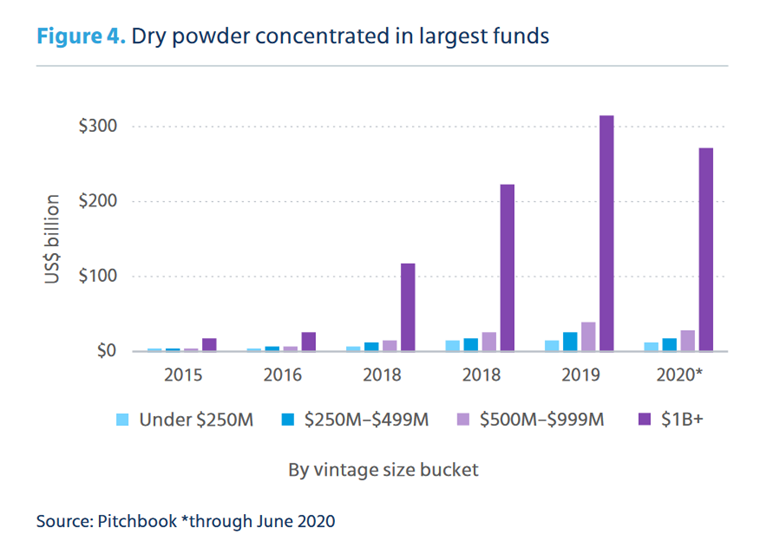

All this fundraising has resulted in huge reserves of “dry powder”—unspent funds looking for acquisitions—in staggering numbers that dwarf the amounts controlled by smaller managers. This money must be spent or general partners (GPs) forfeit the chance to earn large fees. Indeed, much of it will be spent in competitive auctions, buying companies from smaller funds!

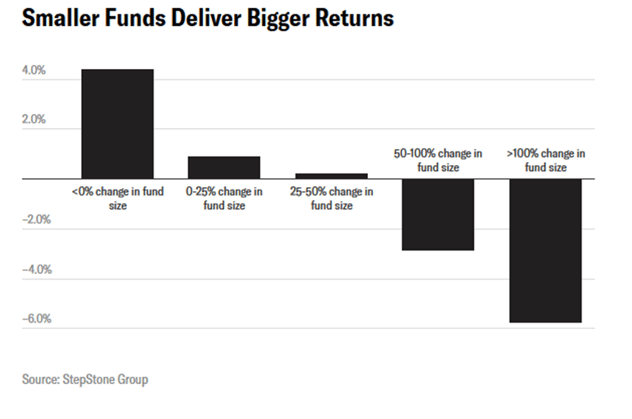

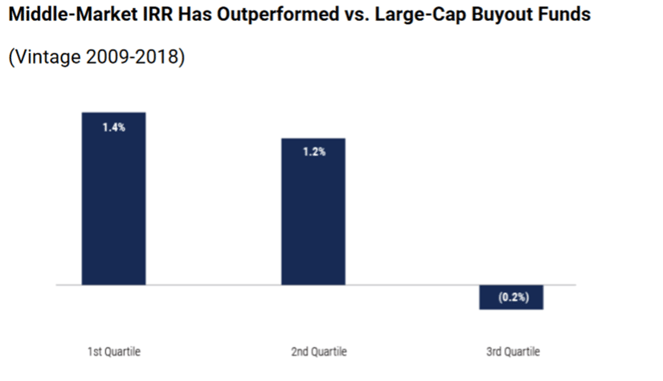

The dynamic of highly competitive large markets with more fragmented smaller markets makes for a very intriguing investment opportunity. As fund sizes grow, the challenge of generating consistent returns grows harder. An increase in fund size of 50% or more is associate with an almost 3% drop in rate of return. Relative fund size growth seems even more inversely correlated with relative performance. Data from Preqin, another research firm, show that smaller buyout funds outperform large capitalization funds 70% of the time on a rolling 12-month basis. A study by the asset manager Pinebridge found that top quartile middle-market buyout funds have outperformed top quartile large-cap funds by 2.7% annually since 2009.

Source: Institutional Investor

Source: PineBridge Investments

There are many hurdles to managing a larger pool of capital. As fee-paying assets balloon, the attention and motivations of PE managers tend to wander from first-rate returns to marketing new products or even to more hours on the golf course. But the simplest explanation for this performance gap may just be the size of deals. According to Institutional Investor, “As transaction sizes grow, questions of a winners’ curse arise. Are some deals creating bidding wars that end in the winner holding an overpriced asset? Evidence suggests that funds involved in these larger deals have struggled to outperform the median IRR of funds not involved in these deals.” The conclusion seems obvious: we should just invest with smaller managers, right?

Broadly, this is a principle we at WMS Partners have embraced, though absolute fund size is less of a predictor of future returns than its rate of change. The critical issue is that, while smaller funds often outperform, the standard deviation of performance across the universe of small funds is much higher. There are rewards but also significant risks in picking a smaller fund manager. In order to ensure you are investing with a top-performing, small private equity partnership, painstaking due diligence is required.

Fortunately, the private equity landscape has two features that make it feasible, at least in principle, to find such skilled managers. As an asset class, PE exhibits both manager dispersion and performance persistence. In brief, the two requisites for picking any active manager, whatever the strategy, are that

1) Good managers’ performance differs meaningfully from that of mediocre ones, and that

2) Good managers remain good managers (i.e. that funds raised subsequent to top-performing vintages also go on to deliver excellent returns).

Public equity mutual funds notoriously fail the second test, while mutual fund performance tends to be less dispersed and clustered around the index as well. The statistical evidence for persistence in private equity returns exists, though it has been getting weaker. Importantly, however, when investors have the time and resources to undertake thorough due diligence, peering beneath the averages and into the drivers of fund performance, there are ways to meaningfully improve the odds.

Private equity is, in many respects, a qualitative people business. Simply asking the right questions to the right people can elucidate, in ways mere numbers cannot, important factors behind returns:

- What is the investment process?

- What is the opportunity set?

- What is the competitive advantage?

- What is the operational value-added?

Critically, performance persistence is much greater if the investor controls for two important variables: team turnover and sensible fund size growth. Are the people making the investments the same people responsible for prior funds and do they have the right incentives? Is the firm growing merely to gather fee-paying assets, or does the logic of fundraising match up with the investable opportunity and the internal resources to take on this larger pool of capital? Where the answer to these questions is yes, a partnership’s strong results are likely to endure. It is notable that access is not a trivial matter, as the best GPs with the discipline to maintain small fund sizes find themselves in heavy demand and their funds many times oversubscribed.

Advantages of the middle market

Smaller deals, on average, have produced better returns than larger ones, albeit with greater variability around outcomes. Why is this, and why do middle market private equity investments (or, similarly, earlier-stage venture investments) offer up less correlation to movements in stock and bond markets? There are a couple of intuitive facts about the middle market that answer both questions.

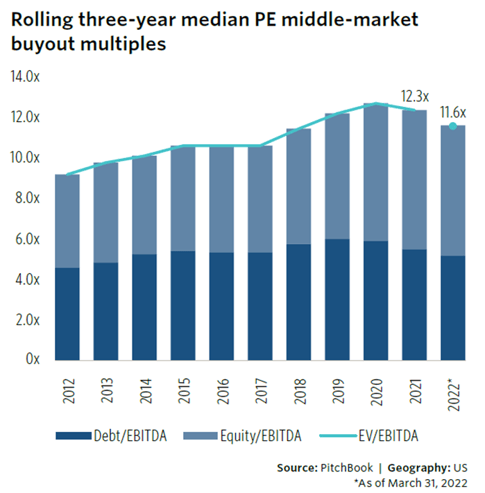

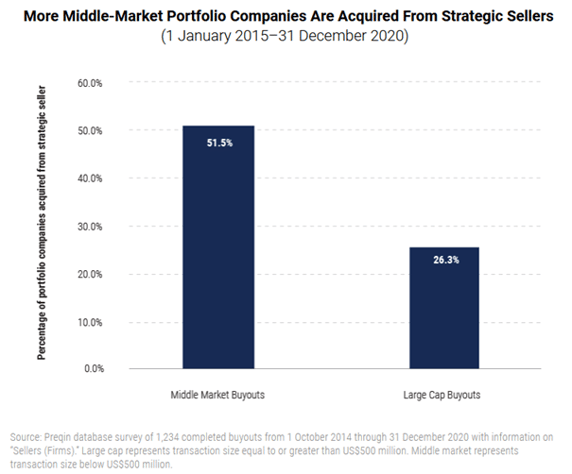

First, leverage and valuation. Both because the purchase process is less competitive, and because the companies themselves are less mature, small acquisitions are simply less expensive. The Pinebridge study compared acquisition multiples of deals smaller than $500 million in enterprise value with larger ones and found that the smaller companies traded 16% cheaper on average. To state the obvious, lower starting valuations, all else equal, translate to higher returns. Partly this valuation discount stems from a different sourcing model for middle market funds. More than half the time, companies are acquired from families, founders, or through corporate carveouts. These markets are less efficiently intermediated and the sellers may be less sophisticated, more motivated to exit, more in need of a private equity partner for continued growth, or all of the above.

Source: Pinebridge Investments

Source: Pinebridge Investments

Smaller companies can support less debt, and the same study reported that buyouts of sub-$50 million EBITDA companies used more modest leverage than larger ones. More debt may hold the potential to turbocharge returns but in an environment of structurally higher interest rates and greater macroeconomic volatility, investors must weigh the higher costs and higher risks that debt imposes as well. Liberal use of leverage also exposes private equity funds directly to the credit cycle, to global liquidity conditions, and to changes in the conduct of monetary policy. That is to say the returns of funds utilizing more leverage are proportionally more linked to global capital markets. Bigger companies may need to exit via IPO or sale to a publicly listed rival, and so in this way are also tethered to movements in the stock market. This is an important consideration for investors seeking to build a portfolio of less correlated assets.

Secondly, at the lower end of the market, skilled private equity managers have greater freedom to flex their operating muscles. It may be hard for a Harvard MBA grad to connect to a small-town Indiana supplier of building materials, but if they take the time to forge that connection, there are often state-of-the-art management best practices to be profitably applied. PE know-how can enhance corporate strategy and efficiency on the production line, or help with financing, strategic M&A, recruitment, sales expansion, or along dozens of other dimensions of a small or medium-sized business. Once a business grows to $1 billion in sales with multiple product lines, there are clearly fewer levers to pull. The implications of this fact on portfolio returns run in the same direction as the leverage question. While large deals are often better businesses, they are harder to improve. And the mere element of active improvement is a driver of investor returns largely uncorrelated with broader markets. Operational enhancements and “sweat equity,” are, to appropriate a public markets term, sources of alpha. And alpha is, by definition, uncorrelated.

Smaller, operationally oriented funds: The right strategy for a moment of volatility and change

The best of these middle market managers will be, in contrast to the trends playing out in the private equity industry generally, spartan in their fundraising. They maintain fund size discipline because they know that every increase in fund AUM requires them to write, pro rata, bigger checks into bigger companies and leaves them with incrementally less meat on the bone. So, to conclude, investors should be looking for smaller funds, with smaller deal sizes, and younger, hungrier management companies, with proven expertise in actually running companies well. Because this active influence is highly variable, hard to explain and harder to quantify, wise investors will spend a lot of time attempting to suss it out. We believe that this added time—over and above what’s required to choose a predictable but ultimately market-correlated megafund—will be rewarded with better returns and superior diversification benefits.

In the coming years, private equity investors are likely to learn that multiples can trend in both directions. Firms that bought high will experience thinner margins for error. When capital flows or availability of leverage go into reverse, attention must turn squarely to the true value (beyond fresh cash) that private equity managers bring to their businesses.

For those interested, investment consultant Greg Dowling explains on a popular podcast why he is excited about opportunities down-market in private equity. To paraphrase Mr. Dowling, the massive amounts of dry powder accumulating at the top of private equity’s inverted pyramid imply that those with the ability to buy companies (moderately) cheaply, drive value-added improvement, and position those assets for sale to a rapacious megafund stand to do unusually well so long as this imbalance persists. This view more or less summarizes the approach WMS Partners has taken to PE and why, despite the headwinds of rising rates, intensifying crowding, and the looming prospect of recession, we are increasingly optimistic about our private equity investments.

It's all about being choosy; in an environment of scarce liquidity, the standard of performance must go up. As investors, we should raise our standards rather than blindly, indiscriminately hoping for returns in assets that don’t mark-to-market. By happy chance, we do see the prospect of meaningful outperformance in private equity. Just not where many are looking. And it will require hard choices and no small amount of hard work.

Related Posts

The Enduring Appeal of Private Equity

The below is the first in a series of articles on private equity from the WMS Investment Committee.

Private Equity in a Late-Cycle Environment: Promise and Peril

In a previous post, we discussed why private equity remains a stalwart of long-term portfolios...

ESG Investing: Purpose and Profits (Part 4)

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate