4 min read

The below is the first in a series of articles on private equity from the WMS Investment Committee.

In October, the co-working startup WeWork pulled its IPO and required a bailout from its deep-pocketed backer, SoftBank. Growth plans are being shelved and workers are being laid off. The unicorn property firm had boasted a valuation of $47 billion, inflated over multiple rounds led by Softbank’s Vision Fund, a huge late-stage venture capital pot that has deployed over $76 billion in two years.

Is the failure of WeWork’s IPO a predictable misfire? A profitless, cash-hungry business with weak internal controls spurned by traditional stock pickers who insist on a greater degree of transparency than its overoptimistic insiders? Something of a familiar story. After all, Facebook struggled in the immediate aftermath of its IPO, prompting charges its underwriters mislead investors about the social network firm’s revenue prospects.

Or, is WeWork’s troubled flirtation with public markets a signal of something larger amiss? Financial media have speculated about too much money being raised in private markets, fictitious valuations of high-flying unicorns, and a wave of bad investments for which the bill may shortly be coming due. Bloomberg speculated in November that most of Softbank’s Vision Fund investments will flop and further writedowns are likely in order. The article implied that venture capitalists are generally no better than stock markets at picking winners.

Core tenets of the private equity value proposition, from the role of venture capital in nurturing growth of technology companies to the effect of buyouts in turning around or repositioning old-fashioned retail businesses, are lately coming under attack. Leverage and corporate distress are rising faster in private markets than in public ones, according to the Wall Street Journal. Is this a moment to reconsider investment policies that allocate heavily to private markets?

We find, in fact, that the private equity model still works well for investors with sufficiently long time horizons, though caution is warranted after an 11-year bull run. In a series of posts, we will examine the proper place of private equity in the portfolios of long-term investors, where we think the risks lie, and how we work to uncover superior risk-adjusted returns in an increasingly diverse private investment landscape.

Why private equity?

Private equity and venture capital have been the standout performers in institutional portfolios for several decades, yet recently alarms have been ringing that these asset classes may no longer offer the sizzle they once did, or, at least, that risks in the sector are higher than have been appreciated. There has been much ink spilled over private equity’s failures. Recent unflattering newsflow has featured the high-profile IPO disappointments of Uber, Lyft, Slack, and Peloton, the dramatic debacle at WeWork, and the dozens of bankrupt retailers saddled with too much debt from the LBO-binge of the mid-2000’s. Below we argue that both the phenomena of private equity’s long-run superior performance and its recent hiccups are understandable consequences of the asset class’s historic success and of its appropriate role in portfolios as we approach the later stages of the current business cycle.

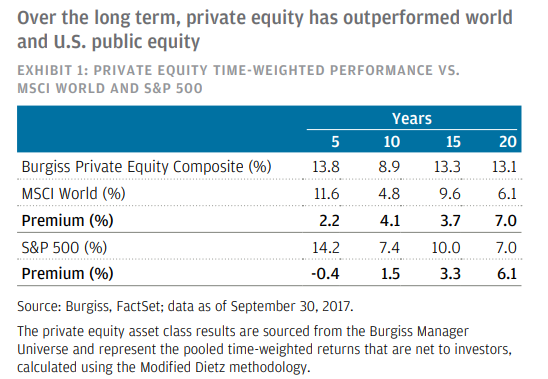

The above chart, from JPMorgan Asset Management, shows the premium private equity funds have earned vs. public stock indices over intermediate and long horizons. Academic research has generally found similar premiums, despite a number of methodological quibbles.[1] One might ask the question: “Why should the future be like the past?” This is really a question about the durability of private equity’s competitive advantage, and we think there are strong economic reasons for continued solid performance to accrue to skilled managers for decades to come. As deal counts and deal sizes rise, these factors ought to be at the front of every private investor’s mind.

Private equity tends to outperform stock indices for several reasons. Investors who are locked up for 10 years or more expect (and receive) an illiquidity premium for their patience. Private equity managers are generally experienced industry hands who lend operational, financial, and marketing expertise to their portfolio companies. In the venture capital and growth arena, immature companies rely heavily on the experience of private equity teams. In the case of buyouts, taking a company private removes it from the spotlight of quarterly earnings reports and the short-termism of Wall Street fast money. In theory, lack of such exposure frees firm managers to re-focus on a business’ long-term competitive position, cut fat, restructure operations or invest in new products and new markets.

These levers afford skilled managers time and room to build and compound value. Further, private equity fund managers who often take a control position in portfolio companies, may be better aligned with owners than public company management teams, who are merely owners’ agents. Critically, this value-add is repeatable. Private equity firms have historically demonstrated both performance dispersion between the top and bottom quartiles, and persistence of performance across sequential funds. The ability of the right manager to dependably add value places a premium on manager selection and due diligence, as the best performing fund groups will find their later fundraising efforts oversubscribed and capacity in new funds full. Thus, for investors who can tolerate illiquidity, an allocation to private equity will often make economic sense in every environment, though it is essential to find skilled general partners, and to ensure that a fund’s structure and terms are favorable to LPs.

[1] See for example: PE outperformance doesn’t add up, Demystifying Illiquid Assets: Expected Returns for Private Equity, or The Faulty Metric at the Center of Private Equity’s Value Proposition.

Related Posts

Middle Market Private Equity: The Art of Picking Your Spots

In our last entry, we wrote that inflation and monetary tightening were returning investors to a...

Private Equity in a Late-Cycle Environment: Promise and Peril

In a previous post, we discussed why private equity remains a stalwart of long-term portfolios...

ESG Investing: Purpose and Profits (Part 4)

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate