19 min read

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate

In the first three parts of this series, most of the discussion has pertained especially or entirely to publicly traded equities. But ESG investors' horizon—along with the interests of regulators and investors—is expanding at such a pace that hardly any strategy is unaffected. Recently the private equity titan Blackstone got into the ESG M&A act, purchasing an ESG-focused software company for $1.4 billion. Blackstone is in the midst of a push to build out ESG capabilities across most of its strategies. “We view ESG as central to our mission of delivering strong returns for clients,” said its president, Jonathan Gray, in a press release. Meanwhile, the European Union’s regulations on ESG disclosure (SFDR) have recently come into effect and apply not just to equity fund managers but to some venture capital funds, insurance companies, and credit institutions.

Evidently, ESG considerations that were once the preserve of a fairly narrow conclave of investors in marketable securities have now become ubiquitous across the entire edifice of finance. Early adopters of ESG integration may stand to reap the benefits of far-sighted investments as the industry catches up. Yet, equally, the complacent risk being disrupted as the likes of Blackstone bring unprecedented amounts of capital and technology to the ESG arena. ESG premia, if they exist, may be competed away over the next several years in a new but familiar chapter of asset management’s never-ending Red Queen race. Here we will examine three “frontier” areas of ESG adoption where software, analytics, reporting standards, and even serious thinking about sustainability have often lagged: fixed income, private equity, and real estate. These are areas where innovative asset managers may encounter more “white space” to develop an ESG edge.

Frontier 1: Fixed Income

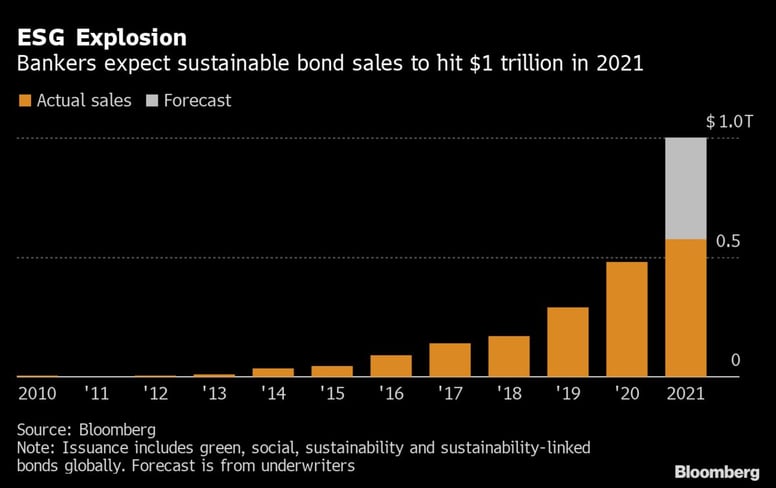

Start with bonds. One popular innovation of recent years has been the market for “green” bonds; this instrument (like its cousin, the sustainability-linked loan) attempts to tie debt issuance to the accomplishment of some climate-friendly project. Green bonds hitch the capital raised to specific corporate (or municipal) investments with perceived environmental or social benefits. Sustainability-linked notes yoke the issuer’s explicit sustainability targets to repayment of principal, coupon, or other conditions set forth in the indenture1.

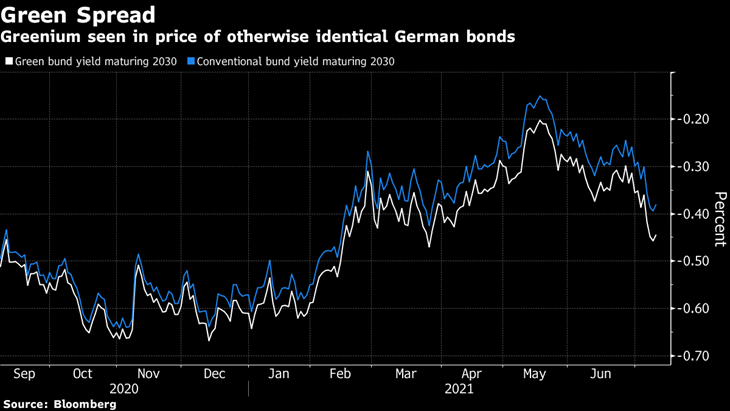

Both have gained in popularity among issuers since they appeal to a segment of investors with explicit sustainability mandates and thus may lower capital costs for those projects deemed eligible. Either by reducing the corporate WACC, or by sending signals (specifically about use of proceeds or generally about an existing portfolio of assets), green bond issuance can be regarded as a positive to the entire enterprise value. The green bond market has grown from its origins in 2007 to more than $269 billion in issuance in 2020. There remains, however, some controversy over whether this form of finance actually accomplishes much in terms of reducing carbon intensity. Green bonds may offer rewards primarily good actors, who are less polluting in the first place, rather than an incentive for firms to clean up their portfolios of assets. A green issue may thus do little to induce new investments that wouldn’t otherwise be made; as in most questions of impact assessment, “additionality” becomes a central concern.

Both have gained in popularity among issuers since they appeal to a segment of investors with explicit sustainability mandates and thus may lower capital costs for those projects deemed eligible. Either by reducing the corporate WACC, or by sending signals (specifically about use of proceeds or generally about an existing portfolio of assets), green bond issuance can be regarded as a positive to the entire enterprise value. The green bond market has grown from its origins in 2007 to more than $269 billion in issuance in 2020. There remains, however, some controversy over whether this form of finance actually accomplishes much in terms of reducing carbon intensity. Green bonds may offer rewards primarily good actors, who are less polluting in the first place, rather than an incentive for firms to clean up their portfolios of assets. A green issue may thus do little to induce new investments that wouldn’t otherwise be made; as in most questions of impact assessment, “additionality” becomes a central concern.

Irrespective of global environmental benefits, however, the availability of cheaper financing for eco-friendly businesses should aid efficient asset allocation by improving price discovery in the market. The increasing bifurcation of the fixed income landscape into "green" and “brown” suggests that environmental footprints will become an essential building block of corporate finance. Imagine prospective CFO’s sitting in business school auditoriums intently studying not just financial accounting, but carbon accounting as well. This is likely to become a reality soon.

Notwithstanding the heady growth in green bonds, fixed income investment does tend to lag behind equities in its integration of ESG tools. This is lamentable; at least in theory, debt investors may be more directly affected by borrowers’ ESG practices. With upside opportunity capped, bondholders must consider ESG matters chiefly through the lens of credit risk. As a conspicuous example, PG&E’s bankruptcy is a clear case of climate risk being mispriced. It demonstrates that ESG risks are material financial risks and must therefore be an integral part of thorough credit underwriting.

There are a number of ways that lenders can incorporate ESG risk analysis. The simplest is to look at the ESG practices of different industries and apply higher required risk premiums to those with poor records, such as oil and gas. Better still would be to look at risk management processes in place across various firms within an industry and tier their credits accordingly. Different investors take different tacks. Golub Capital, a leading credit asset manager, uses a “bottom-up” analytic approach that integrates environmental, social, sustainability, and governance risk criteria into its underwriting of every credit in its direct lending strategy.2 Each investment memorandum for this strategy contains a section dedicated to material ESG concerns. In 2011, Breckinridge Capital Advisors, a large fixed income separate account manager, created a systematic quantitative approach to ESG factors that is now completely integrated into its credit research process. Affirmative Investment Management is a credit investor that explicitly emphasizes ESG and impact strategies. It has pioneered an approach to measure the environmental and social impact of credit. Central to its strategy is meticulous verification of issuers’ statements and whether the actual use of proceeds meet companies’ sustainability goals. Because the stakes are so skewed for credit investors, painstaking authentication is of great importance.

Credit research is clearly a fertile field in which to apply ESG-related insights. ESG data offer a new, distinct input into risk monitoring and management systems. Bond investors tend to be a cynical lot, not given to excesses of hyperbole or grand narratives. Perhaps unsurprisingly, enthusiasm for ESG has been relatively slower to creep into fixed income. Stocks, after all, are a longer duration asset class and may thus be a better vehicle for capturing upside from a company's ESG improvements. But it is inevitable that any analytical tool useful in security selection will be applied to the whole of the capital structure. ESG disclosure standards and data quality may only now be catching up to creditors’ more meticulous demands. In the future, expect a high degree of methodological innovation to arise in the fixed income sector, following in the path blazed by green bonds.

Frontier 2: Private Equity

Whereas an ESG-as-risk-reduction perspective is a natural fit for fixed income asset managers, ESG-as-opportunity-driver should be a mindset comfortably at home in the world of private equity (PE). Core to private equity’s value proposition has always been operational value-add: the ability of patient owner-managers, freed from the glare of public markets’ short-term earnings obsession, "disciplined" by high leverage and incentivized by better economic alignment to bear down on fundamental performance. Typical steps taken are to implement waste-reducing operational efficiencies at portfolio companies, to apply management best practices, to recruit top talent, and to invest in modernizing technology all along the value chain. Such a hands-on, long term-oriented modus operandi should be highly amenable to ESG integration.

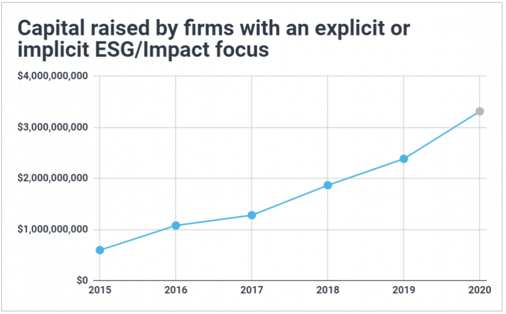

The PE industry, however, has generally yet to embrace ESG as core to its business. According to Ken Pucker and Sakis Kotsantonis writing in Institutional Investor, “The vast majority of private equity ESG efforts remain nascent and superficial.” Far from unshackling operations teams, the lower transparency in private equity seems to have allowed managers to effectively back-burner sustainability efforts at portfolio companies that would be de rigeur for public filers. Private equity GPs have been slow to integrate any of the many reporting initiatives discussed in previous articles. The relatively relaxed attitude of private equity investors toward disclosure, at least when compared to investors in competitive public markets, appears to extend to the area of sustainability as well.

Source: Institutional Investor

Source: Institutional Investor

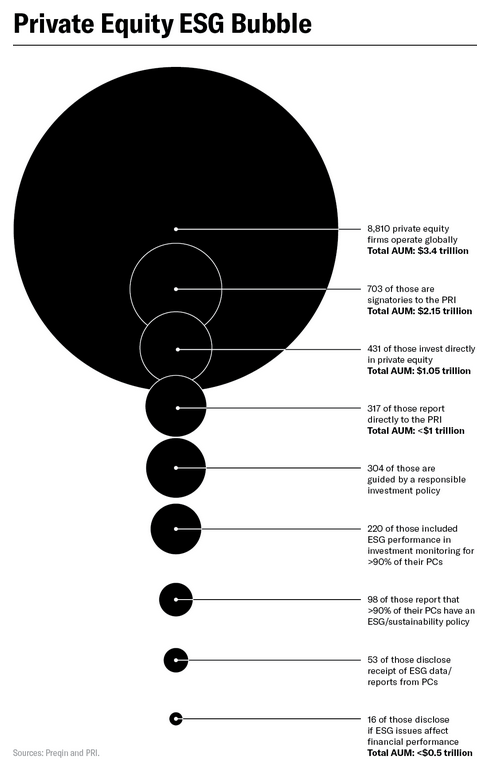

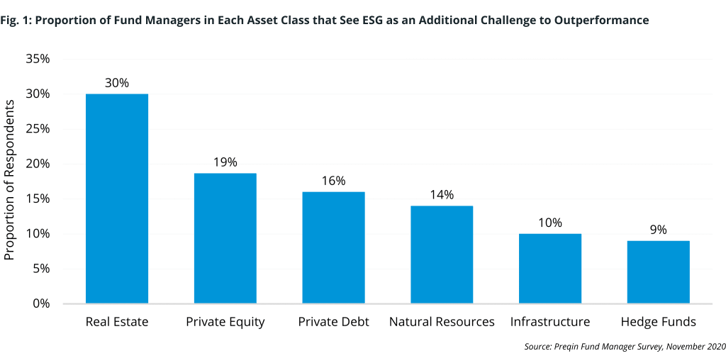

In fact, while a group of the largest PE firms totaling over $2 trillion in assets under management are signatories to the UNPRI, many fewer have sustainability policies in place at their portfolio companies and far fewer still report on ESG materiality to profits. While some prominent LPs (notably certain public pensions) have pushed for better environmental accounting in the PE industry, a recent survey by RBC Global Asset Management found that LPs are “less inclined to build ESG criteria” into their investment approach for PE than they are for other asset classes including public equity, fixed income, real estate or infrastructure. There is some building pressure from the investor community for PE managers to catch up to the levels of ESG integration seen at their public brethren, and larger PE managers are looking to ESG as a source of differentiation. But, considered as a whole, the PE industry remains a laggard.

The PE model is built on the idea of improving businesses. In most cases, PE managers directly control the levers of change at portfolio companies. Whether their strategy looks like a turnaround, an expansion, or a roll-up, ESG is one such lever. So why does the PE industry continue to fall behind public asset managers with respect to ESG integration? Advocates have argued that private equity improves alignment between principals and agents and allows management to make innovative long-run investments outside of the quarterly earnings-obsessed public markets. Researchers have found, by contrast, that private equity managers’ incentives are usually to reach for the lowest-hanging fruit. The median holding period for a PE-owned portfolio company is 4.5 years. Even for private equity sponsors, there are simply too many competing priorities and demands on resources; and sustainability investments are under pressure to deliver over unrealistic timeframes. According to one PE firm's chief sustainability officer, ESG “was always number eight, nine, or ten on the list, and the CEO was focusing on the top six initiatives.”

While PE hold periods are longer than average for stocks, the timeframes needed for deep ESG integration can be neglected as the pace of organizational changes and internal capital re-allocation is much more frenetic at a PE portfolio company. As a result, the patience for ESG project payoffs may actually be thin on the ground. A State Street study reported that 43% of asset managers believe that ESG investments are likely to pay off only over periods of five years or more. Yet only 10-20% actually use such timeframes to evaluate investment performance. Buyout target companies also tend to be smaller than public equivalents and are often less technology enabled. They may thus experience greater challenges in data collection or reporting. Private equity LPs may also have less experience with sustainability reports than public equity investors and may therefore exert less push on managers to integrate ESG into PE investment plans.

Private equity therefore represents a wide gap between ESG opportunity and current practice. The asset class is, in many respects, a natural home for on-the-ground ESG implementation. Steven Strongin of Goldman Sachs writes, “The ability of private equity investors to directly influence portfolio company behavior increases the ability to take a firm from poor practice to good, further raising the potential returns from an ESG perspective.”3 Peter Wirtz, co-head of private equity at London-based alternative investment manager 3i, echoes this assessment: “Private equity investors are in a privileged position. We have a wide scope of influence which extends beyond our own organisations to a large number of portfolio companies, their management teams, employees, customers and suppliers. In addition, decisions can be made quickly, so we have a lot of impact.” The hands-on approach that PE general partners bring to their portfolio companies should help them reap ESG-related benefits in and through a number of potential channels:

- rationalizing supply chains can save money on transportation costs while reducing carbon emissions;

- better data analytics may be able to reduce resource or water intensity in production processes;

- broader recruitment efforts should attract more diverse talent;

- engagement with vendors, suppliers, and customers across portfolios may increase bargaining power to drive impact and improve transparency along the entire value chain;

- PE firms can upgrade the capital structure of portfolio companies by seeking reward for ESG practices by issuing green or sustainability-linked bonds and loans.

These suggestions are just the start. In principle, ESG considerations may be implemented at all levels of the decision process, from the production line to marketing to broader corporate strategy. Further, initiatives that are successful at one company can be shared and scaled across larger portfolios. Amid the celebrations of stakeholder value at last year’s Davos, Carlyle co-CEO Glenn Youngkin revealed that “every [Carlyle portfolio] company now has an ESG plan.”

The idea that private equity managers can use ESG as a lever to help improve business fortunes seems to be validated by numerous high-profile case studies. One such was Carlyle’s investment in Yashili, a Chinese infant formula company caught up in the country’s melamine scandal. Carlyle’s initiatives included switching to 100% imported milk powder and installing a food quality and safety oversight committee made up of international experts. Carlyle later took Yashili public in Hong Kong with better than a 2x return. Carlyle had another ESG success in its investment in Jeanalogia, a Spanish manufacturer of garment-production equipment. Jeanologia’s machines are used to stitch, dye, and finish about 15% of the blue jeans made each year worldwide. One of the technologies Carlyle helped Jeanologia develop can save as much as 85% of the water and chemicals used in denim finishing compared to industry averages. Sales have accelerated as customers realize both cost savings and brand benefits from more sustainable equipment.

Notably, Carlyle is not a PRI signatory. Its rival KKR is; in KKR’s 2018 ESG Report it projected $11 million in annual savings from energy and water-efficiency measures at 11 portfolio companies. KKR has created an ESG diligence group which is now embedded in every aspect of its investment research process. To wit, when KKR bought Unilever’s spreads business in 2018 for $8 billion, this group identified the company’s reliance of palm oil in many plant-based spreads as an ESG red flag. While KKR consummated the purchase, it committed to a goal of 100% sustainable sourcing of palm oil and achieved it within 18 months. These examples of large leveraged buyouts by massive global PE managers are admittedly cherry-picked. But they illustrate that addressing ESG issues can be part of the equation for success, even for less well-resourced sponsors. Indeed, ESG can sometimes be a primary rationale for the investment.

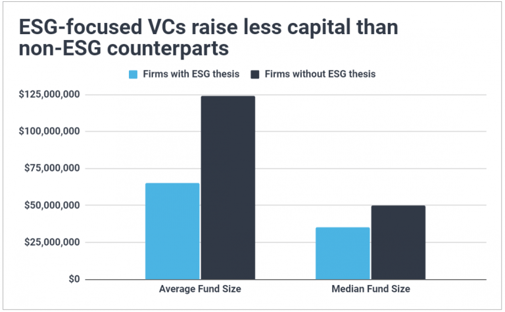

Before leaving the topic of private equity, a final word should be said about venture capital (VC). On Sand Hill Road, much is made about corporate mission statements, social consciousness, and “disrupting” the business status quo. VC-backed companies and their employees frequently do care about such issues as economic inequality and the environment, but Silicon Valley’s record on diversity, on consumer privacy, and on climate change is spotty at best. The likes of Theranos, Zenefits, and Hampton Creek testify that the widely embraced mantra articulated first by Facebook—“move fast and break things”—does not exactly make for a salutary model of corporate governance. It would seem that venture capital’s boasts of widespread ESG adoption are a recipe for rampant greenwashing.

Source: Different Funds

But VC’s historic competitive advantage has been looking further into the future than the industries they aim to disrupt. The next category-killing companies—whether in information technology, healthcare, or energy—are more likely to be backed by venture capital than to grow from the atrophying corporate innovation labs of incumbents. With its distinctive optimism, VC should be uniquely able to target the “double bottom line” of impact and profit. A longer time horizon for investment and a tolerance for years of negative free cash flow give VCs more wiggle room than executives at listed companies. Particularly, as the young are disproportionately early adopters of technology and are more likely to care about sustainability, consumer-focused ventures have every incentive to be cleaner, greener, and more socially minded than competitors. B2B companies that save customers money by reducing or eliminating wasteful resource use will also occupy a stronger competitive position. Finally, VC’s are often thought of as “adults in the room” who can implement both responsible corporate governance and operational nous. While many of the venture industry’s grandiose claims should be taken with a pinch of salt, we expect the best VC funds to be testbeds for ESG initiatives that may become the norm across the corporate world of the future.

Real Estate: The Final Frontier?

As the oldest alternative asset class, real estate investors have a long history of embracing ESG practices under a different name. Divergent nomenclature is common in real estate finance; like sailors, real estate investors have developed their own unique vocabulary—“cap rates” instead of valuation multiples, “net operating income” in place of EBITDA, “mortgage” as opposed to secured loan, "loan-to-value" rather than financial leverage. But it is only recently that real estate as an institutional asset class has begun to see its unique concerns merged with those of the broader ESG investment paradigm. The language of “green building” and “energy savings” can be reframed through the lens of environment. “Inclusionary housing” may be viewed through the social pillar. Governance questions largely translate directly, though REITs have some special issues such as the Maryland Unsolicited Takeover Act.

Property owners have many levers they can pull to reduce the environmental impact of their building. Energy efficiency, water use, and waste disposal can often be upgraded, especially for older buildings. Better insulation, “smart” sensors, and greywater recycling can all impact the investor’s bottom line. As a simplified example, real estate limited partners may want to ask their GP questions such as, “Are you upgrading your lighting fixtures to LEDs? If there’s a five-year payoff and you have a seven-year hold, why are you not doing this?” For many years, the U.S. Green Building Council has maintained a set of standards known as LEED (Leadership in Energy and Environmental Design). LEED-certified buildings, from the baseline rating up through the highest rating level (“Platinum”), have been shown to contribute meaningfully less greenhouse gases while consuming less energy and water. While building to LEED standards also cuts down on costly construction waste, environmental stewardship doesn’t begin and end at project development. Green retrofits have a wide variety of return on investment and payback periods, with whole-building project costs ranging from $2 to $7 per square foot, and payback periods of two to fifteen years, depending on a building’s age, design, and purpose. Some of these timeframes imply internal rates of return below commercial building owners’ targets, which may account for many real estate fund managers’ particular reluctance to make large investments in sustainability. It should be remarked, however, that green buildings are more likely to attract better tenants and to command a premium at sale.

As is typical, real estate investors have their own body for sustainability reporting, adding to the alphabet soup (SASB, GRI, UNPRI, CDP, IIRC, CDSB, etc.) of standard setters recognized by traditional asset managers. For real estate, ESG benchmarks are set by an organization called GRESB, which maintains a highly detailed self-assessment and certification process. GRESB standards can aid investors identify leading real estate managers and can help develop a set of questions and suggestions for improving the sustainability of property ownership. In fact, the basic GRESB questionnaire usefully suggests several topics LPs may wish to discuss with other private equity managers outside of real estate.

As is typical, real estate investors have their own body for sustainability reporting, adding to the alphabet soup (SASB, GRI, UNPRI, CDP, IIRC, CDSB, etc.) of standard setters recognized by traditional asset managers. For real estate, ESG benchmarks are set by an organization called GRESB, which maintains a highly detailed self-assessment and certification process. GRESB standards can aid investors identify leading real estate managers and can help develop a set of questions and suggestions for improving the sustainability of property ownership. In fact, the basic GRESB questionnaire usefully suggests several topics LPs may wish to discuss with other private equity managers outside of real estate.

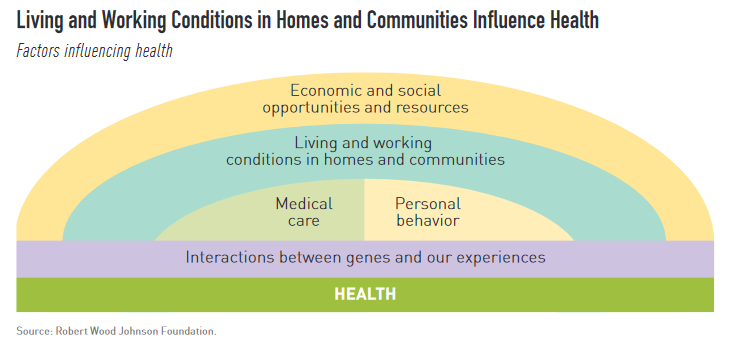

Apart from the environment, there are many social issues on which real estate investments have significant bearing, from tenant (customer) relations, to community impact, to workplace safety and culture. To some degree, these are no different than the social criteria ESG-minded investors care about in their equity portfolios, although there is one critical distinction: real estate is physically instantiated in its community or neighborhood. Commercial property is where people live, work, and shop. As architects and planners attest, the quality of the “built environment” has a tremendous spillover impact on the geography of health, happiness, economic opportunity and social engagement. For some investors, real estate is just dollars and cents, pro formas and quarterly reports. For the people it touches, however, place matters. Property owners thus have a special responsibility to be stewards not just of investors’ capital, but of the neighborhoods they occupy.

One particular example serves to illustrate real estate’s potential for social impact. Affordable housing is often in very short supply in America’s booming cities. Without some amount of dedicated “workforce housing,” the squeezed middle classes risk being priced out of areas with the greatest engines of job creation. Institutional capital largely focuses on class-A or “trophy properties,” increasingly in a few neighborhoods in so-called “gateway” cities. As a result, for investors who know how to take advantage of local and state tax incentives, to navigate federal programs, and to build and manage responsibly, there exist great opportunities to link financial returns and significant place-based impact—often in the same cities they look out upon from glass-and-steel office towers. Especially among the many commercial property sub-sectors, housing is a critical fulcrum for the distribution of economic opportunity and quality of life. Rarely do ESG-minded private equity or credit investors face such tangible choices.

While real estate operates in a slightly different idiom, it is as much affected by ESG considerations as any other investment alternative. Investors in private markets should attempt to understand the distinct sustainability risks and opportunities in each of the many alternative asset classes, all the more since the managers they employ have such an array of tools at their fingertips to drive ESG-related results. In our survey of the evolving landscape across stocks, bonds, and private investments, we have observed a number of recurring themes. Among these are generally improving standards of data transparency concurrent with a confusing tangle of definitions and methodologies, and a rising tide of marketing hype. While statements of greenery or pious intent proliferate, investors’ focus should zoom in on materiality. The objective should be to find strategies that are authentically rooted in ESG research and really do have ESG diligence that is an integral part of and not an overlay on the investment process. Another theme is the increasing recognition that ESG strategies can and ought to pursue “non-concessionary” returns. ESG is a vital tool for risk management and source of investment opportunity. The final theme is that, across all asset classes, engagement between investors and managers around ESG issues should be routine. In our next, and final piece we shall bring together some concluding thoughts and lay out the elements of a robust ESG investment process for advisors and clients.

Please See Our Important Disclosures

1. According to The Economist, sustainability-linked loans now account for a quarter of all green debt issuance (https://www.economist.com/finance-and-economics/2020/02/15/companies-are-tying-their-loans-to-measures-of-do-goodery). Recently, the Italian utility Enel issued one such bond that will increase its interest rate by 20 basis points unless its renewable share of generation rises from 46% to 55% by 2021.

2. Golub Capital, “ESG Policy”, Internal Document, 2021 Update.

3. Strongin, Steven. “Sustainable ESG Investing: Turning Promises into Performance.” Goldman Sachs Research Report, July 6, 2020.

Related Posts

ESG Investing: Purpose and Profits (Part 3)

Part 3 – How Investors Can Incorporate ESG to Reduce Risk and Generate Opportunity

The Enduring Appeal of Private Equity

The below is the first in a series of articles on private equity from the WMS Investment Committee.

Middle Market Private Equity: The Art of Picking Your Spots

In our last entry, we wrote that inflation and monetary tightening were returning investors to a...