21 min read

Part 3 – How Investors Can Incorporate ESG to Reduce Risk and Generate Opportunity

As we roll out this series of ESG articles, the backlash we wrote of last time has continued to grow. A new study carried out by The Economist criticizes ESG funds for an inconsistent approach, selective ethics, and artificial branding. On average, The Economist finds that the world’s 20 biggest ESG funds hold 17 investments in fossil-fuel producers. One even had a stake in a Chinese coal miner. On the whole, we view such critiques as healthy. The discipline of ESG investing—if it can be called that—is no longer nascent but it still lacks focus, transparency, and even broad agreement on the meaning of standard definitions. Forthcoming guidance from European regulators and possibly the SEC should help clear up some murkiness. But investors eager to integrate social or ethical values into their portfolios, or those simply looking at data that might offer a competitive edge, cannot give up and conclude that ESG rests solely in the eye of the beholder. Nor should we rely on standard-setting bodies to determine what qualifies for the label and what does not. Investors must become more clear-sighted about which information is critical to the investment decision and build a coherent process around sourcing, verifying, and evaluating ESG data. Previously we looked at “materiality,” a concept which is at the core of the effort to tie sustainability ambition to traditional financial or management metrics. In this entry, we will go further, highlighting specific data that can aid ESG analysts in ranking companies or projects. We will also dive into a number of the remaining reporting challenges that regulators are likely to address in the coming years.

A vital tool for risk management

Where ESG factors first gained currency among fundamental investors was in the analysis of business risk. Indeed, along with financial and regulatory risk, ESG is becoming a pillar of asset managers’ risk management frameworks. Data privacy controversies like Facebook’s involvement with the research firm Cambridge Analytica, or fraud scandals like Wells Fargo’s fake account revelations have recently sharpened risk managers’ attention to governance cultures at top firms. Likewise, it is becoming apparent that environmentally unsustainable business practices have the potential, in the form of “stranded assets,” to pose serious financial risks. Companies are being forced, by regulators, courts, and activist shareholders to change tack. For all its flowery imagery, ESG offers a suite of tools for cold-blooded risk measurement; these tools need not be the sole province of risk professionals.

Indeed, the case for reducing vulnerability to negative surprises such as corporate scandals has been central to the adoption of basic exclusions-based SRI investment mandates for decades. Recent events have shown that investment risk takes many forms, and that ESG criteria may be a subtle but effective lens for ordinary investors to grapple with this multiplicity of risks. From a Capital Asset Pricing Model point of view, more accurate market pricing of ESG risks (for example, higher yields for energy companies or poor ESG performers in sectors like retail) would make it easier for non-specialists to avoid fat tails. A Bank of America Merrill Lynch report from 2016 highlights this point: ESG factors themselves can be used by ordinary investors as signals for volatility and risk.[1] “ESG could have helped investors avoid 90% of bankruptcies,” the authors write, citing 15 of 17 large corporate bankruptcies from 2008 to 2016 where ESG criteria flashed early warning signs. For risk-averse investors, ESG alone is a valuable proxy for many different portfolio vulnerabilities.

Apart from bankruptcies and frauds, all companies face the same set of systematic risks. But all companies do not enjoy the same level of resilience to so-called macroeconomic tail risk. The recent COVID-19 pandemic illustrates the importance of scenario analysis for global disaster risks across a portfolio. The pandemic, which shut down supply chains, took production offline, and damaged real economies in unforeseen ways may serve as a preview (or even a stress test) of the climate-related risks that companies will increasingly face in coming years.

The bankruptcy of the California energy utility PG&E can be read as a chilling prelude of how climate risks can impinge on even well-run businesses. While the utility’s financial statements included disclosures that it could be exposed to legal liability from faulty equipment, many investors were unprepared to take seriously the scale of risk to life and property posed by Californian wildfires in 2017 to 2020. This was a risk that, as it turned out, was existential for PG&E. Investors with a more finely tuned ESG risk model may have perceived that PG&E’s business was less stable as its consistent dividends implied. While some ESG data and ratings providers flagged safety concerns, others gave the firm strong ratings, a fact that underscores the complexities of quantifying ESG risk. Bloomberg writes that, “On a scale of 1 to 5, with 1 being the lowest risk, Sustainalytics rated it category 4 or higher on quality and safety after a fiery explosion of its San Bruno pipeline in 2010.” The reality that different providers’ ESG ratings, even for a single company, substantially conflict, means that investors must exercise judgment and not rely solely on crude quant models. As climate is a fat-tailed risk, standard assumptions of normally distributed financial returns do not apply. For most assets, climate risk is highly left-skewed. These facts increase the burden on investors to look beyond financial statements and historical volatility when assessing risk. Utilizing a consistent approach to ESG data would aid in this process.

The trouble with conflicting ESG ratings.

Source: https://www.bloomberg.com/news/articles/2019-12-11/conflicting-esg-ratings-are-confusing-sustainable-investors?sref=CWVdwe0e

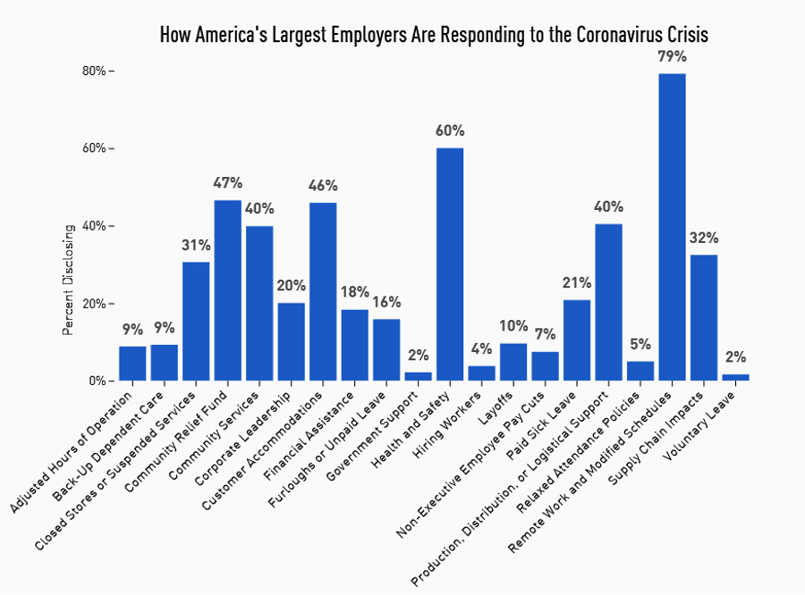

ESG investing remains more art than science. The art lies in choosing which dimensions the analyst views as most material, and in judging how companies’ ongoing strategy accords with numerical scores. Real-life stress scenarios can be a critical way to evaluate performance. The COVID-19 pandemic was a crucible in which company managements could be held to their ESG commitments. Many CEOs signed or endorsed the Business Roundtable’s rejection of the principal of shareholder primacy. Yet noble intent sometimes meets reality only when a crisis strikes. In many cases, corporate actions—for instance, suspending dividends or buybacks to maintain workforces and vendor relationships—matched reverent words uttered before the pandemic. Where they did not, investors should have taken notice.

Holding businesses to account for ESG pledges during COVID-19.

Source: Just Capital, https://justcapital.com/reports/the-covid-19-corporate-response-tracker-how-americas-largest-employers-are-treating-stakeholders-amid-the-coronavirus-crisis/

Still more art than science

Minimizing both company-specific and global investment risks is reason enough for asset allocators to take account of ESG information. But the phenomenal growth in institutional assets under management with at least an ESG overlay is the product of a separate, but related realization: ESG is not only a risk management tool but is itself often coterminous with better investment performance. Where investors and executives used to see only tradeoffs between shareholder value maximization and social responsibility, a more nuanced understanding is emerging. With a focus on the most material ESG factors, capitalism can be both more sustainable and more ruthlessly efficient. In this “doing well by doing good” paradigm, ESG investments have been reframed in terms of positive externalities or virtuous circles.[2]

Why should spending ESG programs deliver superior bottom-line results? Reasons to take seriously this “double bottom line” are the same that undergird the movement toward “stakeholder capitalism”, reflected in the Business Roundtable’s 2019 manifesto and discussed in our previous article. First, firms’ investments in ESG, and asset managers’ financial commitment to those firms tend to have a long duration. When a traditionalist such as Warren Buffett pronounces that his “favorite holding period is forever,” or when economists decry a plague of “short-termism” in the stock market, they are expressing the view that long-horizon (re)investments into a successful business are more likely to create tangible lasting value than a narrow emphasis on cost-cutting or returning capital to investors. ESG-driven investments are more likely to produce durable payoffs over a period of many years.

These types of investments may set the stage for a corporate culture of innovation. Compared to CSR*-inspired public relations campaigns or corporate philanthropy, their benefits may accrue more consistently to the owners of an enterprise. ESG investments may allow a company to better internalize some of the social value they generate via lower costs of equity and debt capital, better customer loyalty, and more motivated and productive talent.[3] In short, they foster better overall alignment of all stakeholders.

A saying common in management circles is “what gets measured is what gets managed.” Management’s short-term bias is often embedded in everything from compensation structure, to performance benchmarks for internal projects, to the information and reports that flow up to top decision makers. Factors embodied in ESG, with years- or decades-long paybacks can be tricky to define and measure. Management practice that focuses on instant feedback risks embedding short-termism in a firm’s culture. The long-term nature of ESG payoffs require a commitment to deeper, strategic thinking on the part of corporate directors and investors alike. They may require a different approach to executive compensation—certainly boards should consider whether excessive emphasis on annual performance hurdles is commensurate with lasting competitiveness and earnings power. ESG-focused investors will find greatest alignment with companies that articulate reasons for doing business and a corporate identity that spans generations, rather than indulging bankers’ and analysts’ taste for treating the firm as a portfolio of assets to be rearranged according to the CEO or the market’s whims.

In its simplest interpretation, ESG provides a clue to help investors overweight “best-in-class” companies. As data collection and reporting has improved, ESG can be more reliably incorporated into portfolios through basic quantitative screens. This effort resembles yet is distinct from the “quality" factor. Yet systematic strategies have so far met with mixed success. A prominent example of this liminal stage of quantification is the sustainability-focused fund manager Arabesque Partners, whose “smart beta” products attempt to integrate the vast array of corporate ESG data into a rules-based process. Despite an innovative approach, Arabesque’s funds have failed to gain much traction, and the firm has recently repositioned itself as an AI consultant.

Fortune Magazine’s 2020 “Change the World” Index. Source: https://fortune.com/change-the-world/2020/search/

The evolution of ESG as a quantitative data science application is in its infancy. The problem such systematic strategies run into is wide variety in the quality and interpretability of ESG information. Even firms lauded for their social impact are often missed by ESG rankings. Porter, Serafeim, and Kramer write that the companies identified in Fortune magazine’s annual “Change the World” list are often not ranked atop their respective industries by ESG data providers. Yet companies receiving this more qualitative source of acclaim have outperformed the MSCI World stock index in the year following publication by an average of 3.9% and have tended to beat analyst estimates after their inclusion.

A social problem

“Social” factors are frequently seen as the most subjective and therefore the most resistant to quantification. Historically, many ESG raters have used employee satisfaction surveys to gauge “social” performance. Evaluated in isolation, however, bad reviews are more likely to pile up at larger firms and will lead socially minded funds to arbitrarily overweight small companies. Firms that monitor reputation risk typically scrape news headlines for negative mentions. This practice may introduce the same bias, and are likely to provide, at best, a lagging indicator. Purdue Pharma was generally highly rated before its role in America’s opioid crisis entered the public consciousness. A close look at inputs such as actual diversity recruitment programs or product safety policies should complement assessments’ positive news coverage, simple counts of women and minorities in leadership roles, and online employee reviews.

Clearly quant screens alone are deficient. Their chief drawback is that they cannot accurately weight what is and will be important, either in terms of impact or of profitability. Investors can of course build weighted averages of the myriad ESG metrics on offer by more than a dozen vendors, but this method is as likely to introduce a fog of data pollution as to zero in on the critical variables. Ultimately, what investors and corporate managers require is a multi-layered fabric of criteria, differing from industry to industry, that together relate social and environmental issues to economic impact and shareholder returns. Building up such a system depends on judgment, experience, and in many cases, dialogue between management and various stakeholders. What the Business Roundtable calls “commitment to all stakeholders,” Porter, Serafeim, and Kramer prefer to term “shared value” creation. Attention to financial materiality, they argue, is the proper platform for ways a company may make social and environmental issues integral to its core strategic positioning. By embedding “profit-driven social impact” at the heart of corporate strategy, companies should see opportunities for sustainable higher growth and profitability, outcomes more likely to align all stakeholders than short-term financial engineering.

Blending data and informed judgment: a unified path forward

Similarly, investors should consider how to integrate analysis of performance on environmental and social factors as part of fundamental investment research, rather than just treating ESG as a separate risk-management overlay. One notable success story is Generation Investment Management, founded by former vice president Al Gore and David Blood, former head of Goldman Sachs Asset Management. Generation’s global equity fund was the best performing fund in Mercer Analytics’ 2018 category ranking over its 12-year history. For its first ten years, Generation’s global equity fund averaged a 12.1%, more than 5% higher than the comparable MSCI index. Generation’s mantra is “The impact on society is the driver of value creation,” and, rather than treat ESG and valuation analyses as separate, it actively searches for firms whose competitive strategies are tied to environmental sustainability. Other prominent examples of blended sustainability and fundamental research included Calvert Investments’ International Equity Fund which has beaten the MSCI EAFE Index by 118 basis points annually over the past 10 years through 2020, and Parnassus Investments’ flagship Core Equity Fund which has outperformed the S&P 500 by an annual average of 107 basis points since its 1992 inception.

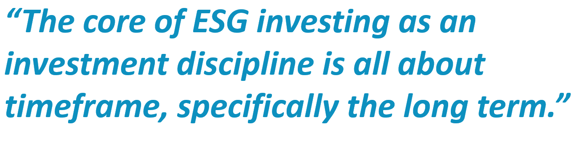

In conclusion, ESG does appear to be a potential source of alpha in stock selection. How can this edge be quantified and democratized? Which “risk factor” do ESG investments exploit? Or does ESG serve mostly as a signal of capable management and intelligent internal capital allocation? Where we can have the most certainty about ESG’s value is in its link to what we might call “time horizon arbitrage.” ESG investments’ longer payoffs should encourage managers and investors  alike to think strategically about the evolution of industries and markets over timeframes of many years. Warren Buffett’s permanent capital has long afforded him an advantage that many benchmark-constrained mutual fund managers lack. Similarly, the late Yale University endowment manager David Swensen has said that the theoretically infinite time-horizon of his sole client allows him to seek opportunities those with shorter-term performance objectives miss or ignore. On this subject, Goldman Sachs’ portfolio research team insightfully offers,

alike to think strategically about the evolution of industries and markets over timeframes of many years. Warren Buffett’s permanent capital has long afforded him an advantage that many benchmark-constrained mutual fund managers lack. Similarly, the late Yale University endowment manager David Swensen has said that the theoretically infinite time-horizon of his sole client allows him to seek opportunities those with shorter-term performance objectives miss or ignore. On this subject, Goldman Sachs’ portfolio research team insightfully offers,

[T]he core of ESG investing as an investment discipline is all about timeframe, specifically the long term. ESG can be thought of as an investment process which posits that the markets and many companies are too short term in their assessments and that if a company effectively invests in its own structure, its people and its community, that company’s long run performance will improve. The idea that companies that embrace better business ethics, respect for human dignity and environmental responsibility as core principles, will over time attract better employees, develop tighter relationships with customers and avoid government censure and thus be able to create more economic value long term, has clear and obvious business logic, even if the timing and magnitude of the value created is less clear. Equally, it is easy to understand how companies that fail to embrace these values are taking serious and perhaps ultimately fatal business risk.[4]

Perhaps “sustainable” might be best translated as “durable” when it comes to companies’ investments in their competitive niche, their own human resources, or the communities in which they operate. For investors, it will be important to put ESG in the correct risk bucket—one less focused on monthly or quarterly performance targets, and more compatible with this sort of long-term thinking.

The communications challenge and the Wild West of ESG data

It is the purpose of financial markets to allocate capital toward its most efficient use. Businesses make strategic investments; stock and bond markets supply them with capital at a fair price. If markets are to perform this information processing function, investors in those markets need both accurate information and an understanding of what that information means. Today’s bewildering mix of ESG reporting requirements and standards means there remains, in Keynes’ phrase, “many a slip twixt the cup and the lip.” Good intentions count for only so much; a coherent corpus of what constitutes ESG best practice is still some way off. This communications challenge between executives and capital markets continues to hold back broader ESG adoption among asset managers.

Regulatory standard setters have thus far failed to coalesce around a single, unified code of guidance. Companies’ ESG stories are self-reported, largely through unaudited, glossy corporate sustainability reports (CSR's) filed with securities market regulators. Today, 58% of companies in the S&P 500 publish one, up from 37% in 2011. According to The Economist, a few broad standards dominate this alphabet soup of ESG reporting. The Task Force on Climate-Related Financial Disclosures (TCFD) and the Carbon Disclosure Project (CDP) provide guidelines for companies’ reporting of exposure to climate risks.[5] The Global Reporting Initiative (GRI) extends sustainability reporting to human rights and corruption. This, the oldest standard founded in 1997, remains the most popular with 40% of S&P 500 companies referencing it in their sustainability reports.

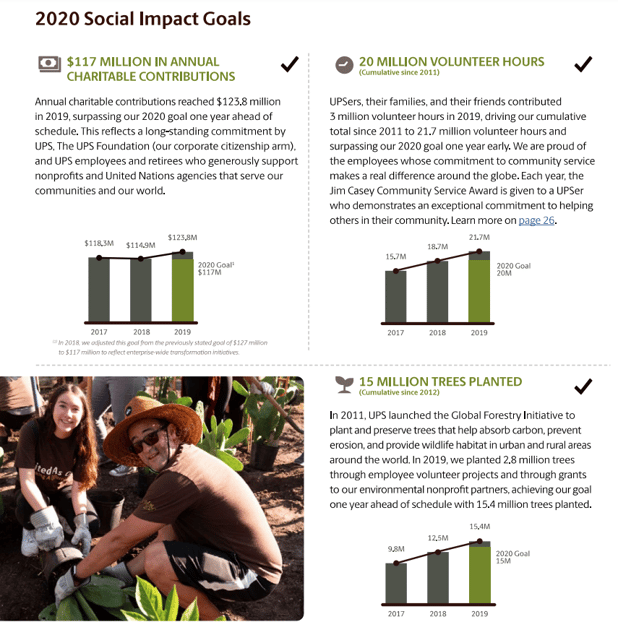

A sample Sustainability Report, from the logistics company UPS.

Source: https://about.ups.com/content/dam/upsstories/assets/reporting/2019-UPS-Corporate-Sustainability-Progress-Report.pdf

Recently, initiatives to integrate ESG materiality into financial reporting have gathered momentum. Robert Eccles, a professor at the University of Oxford, launched the Integrated Reporting Initiative which encourages companies to include some social and environmental indicators in their regulatory filings. By 2020, 96% of the world’s largest 250 companies had done this, up from 44% in 2011. SASB standards, which explicitly link ESG to financial materiality, are rapidly gaining ground, thanks in part to their embrace by large asset managers such as BlackRock and State Street. SASB is now referenced by a quarter of S&P 500 companies. Financial market regulators have generally been content to let this Wild West of self-policing evolve on its own. In the long run, it seems likely that one single reporting standard—or at most a few—will prevail, since there are clear network effects to widespread adoption of a lingua franca, even an imperfect one. But regulatory pressure could nudge the market in one direction or another. The European Union’s Non-Financial Reporting Directive, first promulgated in 2018 for companies subject to EU regulation, will accelerate the trend toward consistency and external verifiability of data. SASB, GRI, TCFD and others will want to coordinate their efforts in harmony with the EU’s legally binding playbook.[6] By failing to set clear rules, U.S. regulators risk letting their Brussels and Frankfurt counterparts determine the roadmap.

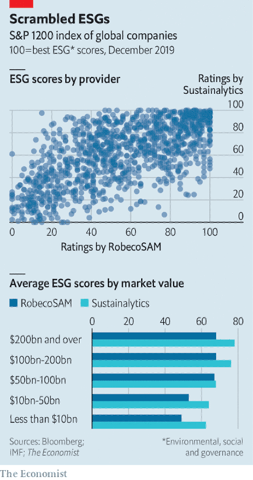

Besides voluntary reporting, there is tremendous fragmentation among third-party data providers that rank ESG performance. As mentioned earlier, contrasting ratings are a real problem Mark Kramer and coauthors note that,

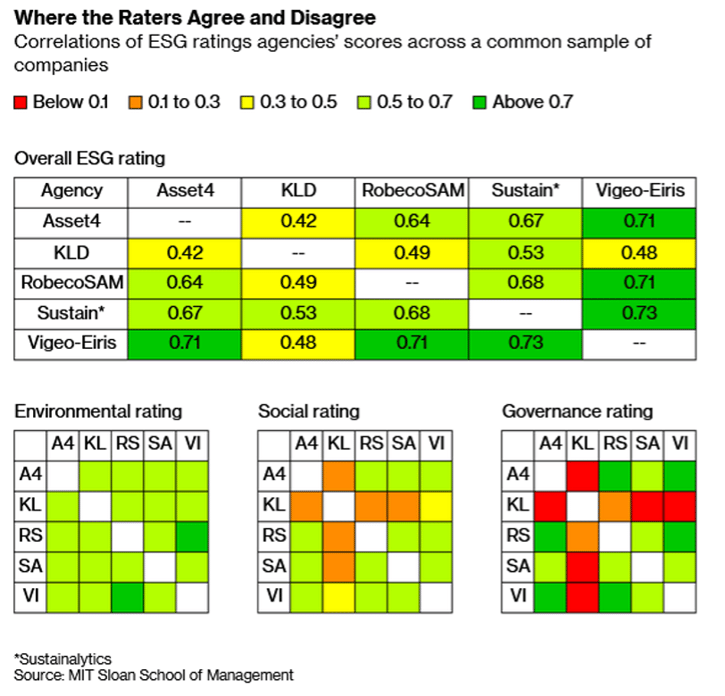

[O]ne assessor’s A+ is often another’s C-. Saudi Aramco — responsible for massive carbon emissions from the oil it sells — was rated higher than sustainability-focused retailer Costco by a top provider. A 2019 study found the correlation among leading ratings providers — including MSCI, Sustainalytics, Bloomberg, and RobecoSAM — to be only 30 percent. This contrasts sharply with a 99 percent correlation among credit ratings agencies.[7]

If ESG is to have any meaning, its meaning will have to be similar across different contexts and different parties. A study from MIT’s Sloan School of Management found correlations of 0.61 among scores for 823 companies by five leading ESG raters. Unsurprisingly, divergence was strongest in the more subjective categories of “social” and “governance,” than for “environmental.”[8]

The message for investors employing third-party ratings agencies is clear: it is unwise to rely on a single ratings provider, or on external ratings alone. At minimum, investors will want to triangulate several sources, and ideally integrate outside ratings with internal analyses tied to discussions with management. As the definition of ESG begins to narrow around areas most salient in terms of “shared value” creation, and as greater data reporting improves the measurability and comparability of corporate ESG investments, it is natural to expect scoring systems to converge over time. Less organically, there are signs of consolidation and growing heft among the data providers themselves; in 2019, the credit ratings agency S&P Global acquired the ESG ratings arm of the asset management firm RobecoSAM, while Moody’s purchased the independent provider Vigeo Eiris. In 2017, Morningstar, a mutual fund and equity research firm, bought a 40% stake in Sustainalytics. From the point of view of investors, such an elimination of redundant and conflicting information is surely welcome.

The message for investors employing third-party ratings agencies is clear: it is unwise to rely on a single ratings provider, or on external ratings alone. At minimum, investors will want to triangulate several sources, and ideally integrate outside ratings with internal analyses tied to discussions with management. As the definition of ESG begins to narrow around areas most salient in terms of “shared value” creation, and as greater data reporting improves the measurability and comparability of corporate ESG investments, it is natural to expect scoring systems to converge over time. Less organically, there are signs of consolidation and growing heft among the data providers themselves; in 2019, the credit ratings agency S&P Global acquired the ESG ratings arm of the asset management firm RobecoSAM, while Moody’s purchased the independent provider Vigeo Eiris. In 2017, Morningstar, a mutual fund and equity research firm, bought a 40% stake in Sustainalytics. From the point of view of investors, such an elimination of redundant and conflicting information is surely welcome.

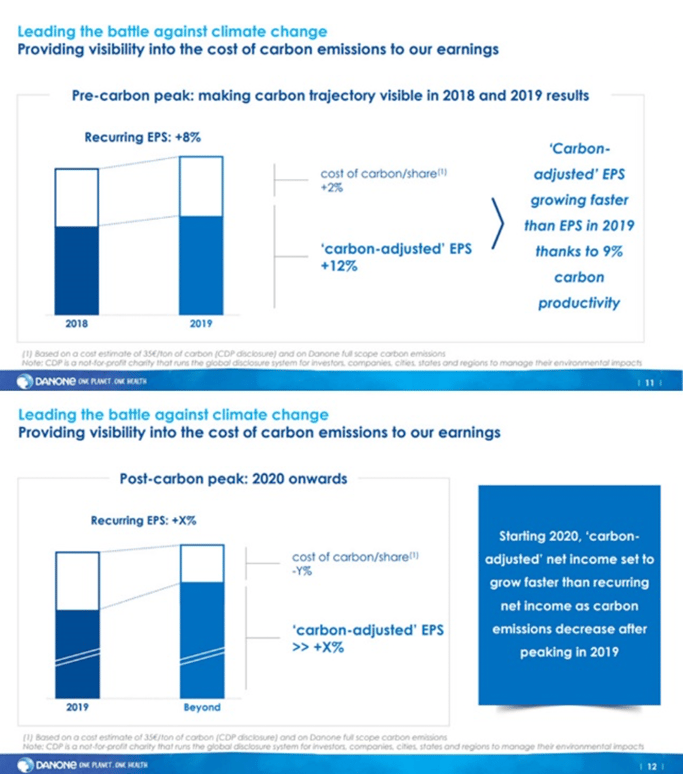

There is a broader issue that more precise standards and more consistent ratings will not address. Corporate communication around ESG initiatives and their relevance to investors must improve. In the absence of clear unified reporting guidelines, companies are taking the investor outreach effort into their own hands. Porter, Serafeim and Kramer describe how when the boss of Becton Dickinson (BD), a medical device company, met with analysts at its 2017 investor forum, he detailed BD’s efforts to build sustainable public-private partnerships throughout its emerging markets value chain, and then directly quantified their impact in terms of sales. Over the five years from 2011 to 2015, he explained that these efforts had borne fruit to the tune of over half a billion dollars in additional growth. Transparency is even more helpful when it is forward-looking. In 2020, yogurt-maker Danone published projections of its “carbon-adjusted” earnings per share, telling investors that its planned €2 billion of investments to address climate change through agriculture, energy, packaging and digital technology were expected to “deliver in the midterm a consistent mid- to-high-single-digit recurring earnings per share growth.”

Source: Danone. These sorts of slides are featuring more frequently in companies’ investor presentations, linking sustainability initiatives to key financial metrics like sales growth and profitability.

The fruits of such detailed ESG disclosures can be substantial. When Kramer and coauthors looked at a small sample of 21 firms in seven industries, they found that those classified as “strong ESG communicators” had much lower variation in analysts’ earnings estimates, and that they enjoyed price/earnings ratios on average 40% higher than their industry. Clear communication of capital spending plans (ESG or not) is also likely to lower the standard deviation of stock returns, improving the Sharpe ratios on which many asset managers are evaluated.

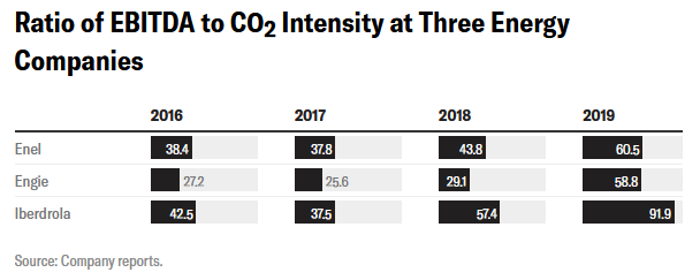

As investors look to quantify the scale and returns from company’s ESG projects, new approaches that blend ESG and traditional financial analysis are taking shape. One encouraging idea championed by academics, asset managers such as Blackrock, and companies like the Italian utility Enel is the creation of new hybrid metrics. Enel has pioneered the ratio of EBITDA to carbon intensity, which can directly tie the environmental sustainability of energy companies’ portfolios to profits. It shines a light on two important concerns for a power company: cost efficiency and compliance with forthcoming stricter emissions standards.

It is perhaps easiest to see the relevance of such blended ratios in the energy industry. Yet they may apply more widely. One could, for example, tie profitability to nutritional value for food and beverage companies or health outcomes at insurers and drugmakers. Similarly, EBITDA per unit of waste avoided, service workers wages, use of recycled materials, or customer financial wellbeing could extend the concept to retailers, materials concerns, and financials respectively. As always, a pertinent investor consideration is likely to be improvement along any of these dimensions, not simply their absolute level.

Along with offering firms tools to evaluate manager performance or trade off competing investment proposals, new metrics promise to make investors’ quantitative screening more reliable. Marrying non-financial to financial objectives introduces a route to further integrate ESG metrics into conventional security analysis. Nevertheless, no algorithmic screen seems ready to supplant thorough qualitative research. While investors and companies continue to circle in on the “right” metrics for each industry, what we might term the fundamental theorem of ESG active management still holds unambiguously: in the absence of perfect ESG information, there will be potential alpha to be derived from deep fundamental analysis.

Conclusion

ESG encompasses a complex range of factors for investors to consider. Where asset managers spin heartwarming tales of saving the planet but pack their funds with fossil fuel companies, critics are right to cry “greenwashing”. But the solution to a bubble in “green” investment offerings is not to abandon the pursuit of more sustainable ways to allocate capital; it is to dig into the data, to question simplistic ranking methodologies, to ask tough questions, and to develop a rigorous investment process built for long-term results. “Rigorous” is often assumed to mean exclusively quantitative; not here. Quantitative approaches show promise, particularly those that unite traditional financial analysis with ESG data centered around the criterion of materiality. But qualitative approaches, from interviewing fund managers and CEOs, to thinking hard about which sustainability efforts will pay off and over what time frame, to taking seriously the elusive social variable all complement a data-driven approach. Fortunately, there is momentum from government and the private sector in driving more and more standardized reporting. How investors make use of greater data transparency will come down, as always, to the most qualitative factor there is: judgment.

Please See Our Important Disclosures

* “CSR” stands for “corporate social responsibility,” an analogous movement whose popularity peaked before the financial crisis of 2008.

[1] Subramanian, Savita, Dan Suzuki, Alex Makedon, Jill Carey Hall, Marc Pouey & Jimmy Bonilla. “Equity Strategy Focus Point ESG: Good Companies Can Make Good Stocks,” Bank of America Merrill Lynch (2016).

[2] This is essentially the point of a recent book by another Harvard Business School professor, economist Rebecca Henderson. In Reimagining Capitalism in a World on Fire (PublicAffairs 2020), Henderson uses multiple case studies to illustrate how companies’ targeted investments in their community, in their workforce, and in their environment came to be seen not just as a cost of doing business, but as avenues for growth and profits. Further, she argues that corporate leadership on social issues is desirable and necessary as only the private sector has the flexibility and the tools to make these types of investments.

[3] The software company SAP produces one of the most detailed reports on its social impact efforts. Using regression analysis, the company found that a 1% increase in “engagement” correlates with a 0.8% increase in operating profit. For comparison, a decrease in carbon emissions by 1% is associated with a 6% profit boost.

[4] Strongin, Steve and Deborah Mirabal. “Sustainable ESG Investing: Turning Promises into Performance.” Goldman Sachs Global Portfolio Analysis Research Paper, July 6, 2020.

[6] EU regulation around ESG is coming to the asset management industry soon. A new requirement, due to come into force in 2022, will enforce clearer guidelines for managers and index providers who label their products “sustainable.” https://www.sidley.com/en/insights/newsupdates/2020/06/esg-disclosures-for-asset-managers

[8] Other methodologies currently gaining traction are the Impact Management Project’s effort to globally coordinate standard for impact investing and the Impact-Weighted Accounts Project that is working on a uniform set of hybrid accounts that capture social, environmental, and financial impact at once.

Related Posts

ESG Investing: Purpose and Profits (Part 2)

Part 2 – How Businesses Can Effectively Integrate ESG

ESG Investing: Purpose and Profits (Part 4)

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate

ESG Investing: Purpose and Profits (Part 1)

Part 1 – No Longer a Backwater

In the last two decades, ESG (“Environmental, Social, and...