16 min read

Part 1 – No Longer a Backwater

In the last two decades, ESG (“Environmental, Social, and Governance”) investment strategies have gone from fringe concerns, championed mainly by the likes of jet-setting do-gooders such as Bono and Al Gore, to a core pillar of the investment industry.

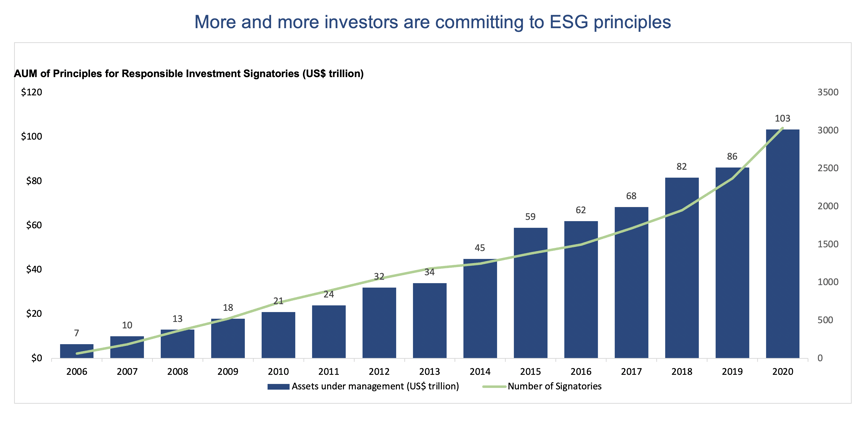

Staggering sums have been raised for ESG-focused funds, and the standards of corporate ESG reporting on ESG have improved markedly. This paper is the first in a series arguing that, while some skepticism of ESG hype is warranted, in a world which increasingly looks to business to address enormous environmental and social challenges, the precepts of ESG can no longer be safely ignored. Like it or not, all investment fiduciaries will be called on to develop and implement a coherent ESG process. Institutions are rapidly putting ESG front-and-center in their investment plans. When it was formed in 2006, the United Nations Principles for Responsible (UNPRI) Investment included 100 signatories with $6.5 trillion in assets under management. Today, this initiative has been signed by over 1,500 investors commanding over $80 trillion in AUM. A recent study by the SIF Forum for Sustainable and Responsible Investment found $12 trillion in ESG investments in the United States alone, with ESG representing more than 20% of total professional AUM. Such growth is likely to continue for the foreseeable future.

source: UNPRI

At WMS Partners, we too strive to balance a deep commitment to social responsibility with the demands of seeking investment profits for our clients. As we work with clients to evolve our own ESG framework, we want to share some of what we’ve discovered. A central insight that guides our vision is the following: Building pro-social principles into the core of the investment process should no longer be seen as a drag on returns. On the contrary, we find that ESG, when done right, is critical to creating and driving investment value.

A short history of the ESG concept

What do ESG-minded investors care about? Environment, social, and governance criteria encompass such a vast landscape of considerations that, in attempting to cover everything, the ESG rubric risks standing for nothing. For this reason, it’s important to delineate some concrete areas that investors may choose to spotlight. A few are listed below:

-

- Environmental: emissions reduction or carbon offsets, improving energy efficiency, discovery and use of more efficient materials, recycling and reduction of waste and effluents, water efficiency in agriculture and industry, sustainable land use and protection of vital ecosystems, conservation of biodiversity.

- Social: diversity and equal opportunity, payment of a living wage, employee health and wellness, rigorous product safety standards, zero tolerance for child and forced labor

- Governance: management transparency, tax compliance in all jurisdictions, decreased emphasis on lobbying and political rent-seeking, “fair trade” practices, disavowal of anticompetitive behavior such as predatory pricing.

- Environmental: emissions reduction or carbon offsets, improving energy efficiency, discovery and use of more efficient materials, recycling and reduction of waste and effluents, water efficiency in agriculture and industry, sustainable land use and protection of vital ecosystems, conservation of biodiversity.

This list is obviously not comprehensive, and different investors will weigh different priorities differently. What these goals have in common, besides their apparent nobility, is that integrating them further into existing business practices is potentially compatible with the narrower objective of shareholder profits.

In past decades, ESG initiatives were seen as a distraction from corporate managers’ chief focus and were at best neutral for investor returns. What we might call “ESG 1.0” grew out of a movement in the 1980s and 1990s toward “socially responsible investing” or “SRI.” SRI investors deliberately excluded industries and companies viewed as engaging in activities destructive of social welfare. Typically, these exclusions concentrated on the marketing of “sin” products (alcohol, tobacco, gambling, and firearms), though they could encompass industries doing business with repressive political regimes, such as apartheid South Africa. Thus, SRI formed a set of exclusion criteria, limiting the universe of acceptable investments. In simple economic theory, options have monetary value, so forgoing the option to invest, for example, in spirits companies, would be costly. SRI investors implicitly accepted a potential tradeoff in returns, almost on philanthropic grounds. The recent trend of endowments and foundations divesting from fossil fuel assets should be seen as an outgrowth of this paradigm.

ESG 1.0 can be seen as more inclusive than SRI, and simultaneously less forgiving. While entire industries might not have been marked for disinvestment, ESG investors also sought to exclude individual companies, regardless of industry, with a poor reputation for upholding human rights, a weak governance structure, or a damaging environmental record. The confectioner Nestle’s association with slash-and-burn palm oil agriculture, Exxon’s Valdez oil spill, or Union Carbide’s Bhopal chemical disaster were high profile scandals that marked these companies as uninvestible for certain institutions, even while their industry peers might be rewarded with overweight positions. A spirits company with good labor relations and a spotless environmental record might thus be a core position for an ESG investor.

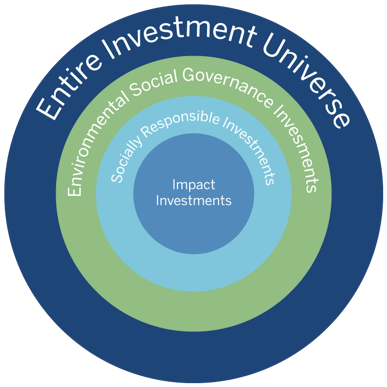

Under this schema, the most restrictive investment universe is labeled “Impact”, a category of investments made primarily for some measure of positive social benefit with profit consideration secondary.1 SRI strategies are afforded slightly wider latitude, while ESG incorporated a still broader constellation of allowable investments. As you move from impact investing to larger and larger investible universes, expected returns increase.

By contrast, the social good an investor can hope to achieve runs from lowest in the unconstrained universe to highest in pure “impact”. This way of thinking embeds the economic orthodoxy of choices, tradeoffs, and constraints. Just as consumer welfare is improved when given more choices of breakfast cereal at the supermarket, the widest latitude in investable assets serves to maximize investor welfare. Investment products labeled “ESG” were thus characterized by sacrifices and sanctimony. Companies hoping for strong ESG scores and a "good actor" designation as devoted internal resources to “Corporate Social Responsibility” initiatives which were justified (when they were rationalized at all) merely as exercises in public relations.

The legacy of this mindset is still felt today: many seasoned investors accept as given the proposition that incorporating ESG concerns means sacrificing financial returns. The possibility that narrowing the scope of investment possibilities to the best-behaved companies may in fact aid in finding the best performing investments is not yet universally recognized. A 2015 survey of institutional investors conducted by the consultant Cerulli Associates and the UNPRI found that “misperceptions of negative impact on investment performance” was noted as a challenge to ESG adoption by 88% of respondents.

The ESG 1.0 era, with its vaguely defined mission statements and blithe platitudes, was not entirely misguided. Viewed in historical context, the lack of precision with which ESG strategies were conceived was typical of any nascent investing movement. A proliferation of definitions and simplistic methodologies equally characterized the early years of value investing in the 1930s and 1940s, or, for that matter, quantitative investing in the 1970s and 1980s.

ESG: The present and the future

The evolution of ESG thinking and practice since the Great Financial Crisis has seen investors grow continually more sophisticated. We have entered an era we might call ESG 2.0—where ESG investments are equally performance- and impact-seeking, and where use of ESG as a risk mitigant is ubiquitous. What 40 years ago was primarily an exclusions-based approach has seen a movement in the last decade to incorporate ESG factors into fundamental investment decisions. In turn, what was viewed as a performance handicap has been reframed as a potential source of returns. More sophisticated portfolio design and better data means that strategies have gotten better at producing results at the same time as thinking has broadened.

The ESG state of the art aims not to replace traditional financial analysis, but rather to augment it with a suite of tools that help understand how companies manage their “off-balance-sheet” ESG assets and exposures, or what leading ESG-focused asset manager Calvert Investments calls “ESG capital.” Such an intertwined analysis of fundamental and ESG attributes in tandem results in a functionally more complete view of company prospects. It should have the added benefit of reducing portfolio volatility and managing downside risk. One conclusion that emerges from the observation of top practitioners is that incorporating ESG is most compatible with a long-term investment horizon, whether one adopts the perspective of a passive or a control investor. The asset manager T. Rowe Price writes that “Integrating ESG considerations into our fundamental research has helped the firm identify well-managed companies that are leaders in their industries, more forward-thinking, better at anticipating and mitigating risk, and focused on the long term.” Such statements are increasingly common among fundamental investors.

Most recently, as markets and economies have been rocked by various climate-related disasters and the COVID-19 pandemic, the focus of attention has progressively shifted to the role of companies, not just in adhering to minimum standards of corporate citizenship, but as creators and safeguards of social welfare. Correspondingly, the investment community at large appears to be engaging more with ESG issues formerly deemed tangential. Investors are asking whether portfolio managers have meaningful dialogue with top management or vote proxies independently. Further, there is an emerging consensus that what is good for shareholders need not be in opposition to what is good for all stakeholders. In 2019, the Business Roundtable, a collection of large company CEOs, proclaimed that the purpose of a corporation was not, as in Milton Friedman’s doctrine, solely to maximize shareholder profits, but rather to “promote an economy that serves all Americans”—including customers, employees, communities and other stakeholders.2 Such a statement emanating from the seat of financial capitalism would have been unthinkable a few years ago, and indeed many saw it as mere lip service. But the language in the Business Roundtable’s declaration echoed closely that which ESG investors have employed for years. Stockholders interested in long-term returns are not adversaries to other critical consitutencies. On the contrary, shareholders, as ultimate owners of a business, have a crucial role to play in driving corporate strategy. From the point of view of a professional equity investor, constructive engagement with companies to inspire and steer change can be seen as a rare uncorrelated driver of return—that is, a potential source of alpha. Having concrete ideas gets minority shareholders invited back to a seat at the table. Helping to improve a business—the mindset of the private equity control investor—is more valuable in the context of diversification than simply selecting today's top performers.

The world is changing, and successful investors must adapt. At WMS, we do not believe that ESG considerations and investment performance is necessarily an “either/or” proposition; it is increasingly a “both/and”. As we will review in later in this post, there is a body of empirical research testifying to this reality. There are also concrete steps money managers can take to improve performance and lower risk, while being attentive to the concerns that animate ESG-focused investors. Managers we work with at WMS have found creative ways that they can engage with companies to improve transparency, diagnose governance issues before problems arise, and (especially in the case of private equity) improve efficiency and sustainability at once. It is becoming clear that an integrated approach looking at all steps of value creation is preferable to a simple set of binary exclusions and quantitative screens. That said, purpose-driven investing must involve more than paying lip service to marketing buzzwords, looking at rankings, or checking “CYA” boxes. It must emphasize a holistic consideration of business ethics as well as an understanding of the critical issues of “financial materiality”—which ESG factors are most pertinent to a firm’s bottom line. It will require better, more accurate, and more relevant data. In the coming entries, we will review evidence of how ESG considerations can lead to improved and more sustainable long-term investment performance, and we will lay out some of the ongoing questions and challenges to developing a successful ESG approach.

The world is changing, and successful investors must adapt. At WMS, we do not believe that ESG considerations and investment performance is necessarily an “either/or” proposition; it is increasingly a “both/and”. As we will review in later in this post, there is a body of empirical research testifying to this reality. There are also concrete steps money managers can take to improve performance and lower risk, while being attentive to the concerns that animate ESG-focused investors. Managers we work with at WMS have found creative ways that they can engage with companies to improve transparency, diagnose governance issues before problems arise, and (especially in the case of private equity) improve efficiency and sustainability at once. It is becoming clear that an integrated approach looking at all steps of value creation is preferable to a simple set of binary exclusions and quantitative screens. That said, purpose-driven investing must involve more than paying lip service to marketing buzzwords, looking at rankings, or checking “CYA” boxes. It must emphasize a holistic consideration of business ethics as well as an understanding of the critical issues of “financial materiality”—which ESG factors are most pertinent to a firm’s bottom line. It will require better, more accurate, and more relevant data. In the coming entries, we will review evidence of how ESG considerations can lead to improved and more sustainable long-term investment performance, and we will lay out some of the ongoing questions and challenges to developing a successful ESG approach.

Institutional investors have woken up to ESG’s importance. It should not just be a consulting- and marketing-driven fad

Cynical observers of the investment industry could be forgiven for regarding all the ESG talk coming from Wall Street and consultants as superficial “greenwashing”—a way for companies and investment managers to polish their brands in the eyes of a new generation of consumers. Optics may indeed be one driving force. According to a survey of 500 institutional investors by Natixis Investment Managers, “improved image and reputation” was the primary benefit of incorporating ESG into their process. The benefit of this sort of reputational enhancement, predictably, has not escaped the notice of the largest institutional asset managers. Last year, BlackRock CEO Larry Fink announced that, by the end of 2020, 100% of its portfolios would apply ESG metrics. At last year’s pre-pandemic World Economic Forum in Davos, founder and president Klaus Schwab told attendees that “performance must be measured not only on the return to shareholders, but also on how [a company] achieves its environmental, social and good governance objectives.” Once a refrain is echoed unquestioningly among the global glitterati in the halls of Davos, it has surely gone mainstream.

But, as Harvard Business School academics Michael Porter, George Serafeim, and Mark Kramer write in an Institutional Investor op-ed, using “sustainable” initiatives solely as a way to burnish reputation and attract socially conscious investors, employees, and customers displays a lack of vision and ambition: “The impact of social innovations on competition and economic-value creation are not fully understood or even considered,” the authors conclude. “As a result, corporate executives, analysts, and investors alike are missing a powerful value driver.” Paying modest attention to ESG concerns ought not to be seen as a matter of image or as a license to operate, but as a source of competitive advantage. Likewise, investors who look only at historical financial information are neglecting an important part of what drives a business’ bottom line.

Notwithstanding the mood of the World Economic Forum, many professional investors have been slower to embrace such thinking. Conspicuously, when the Business Roundtable issued its recent commitment, the Council of Institutional Investors promulgated a rebuttal contending that its statement “undercuts notions of managerial accountability to shareholders” and that such pieties elide the clear distinction between mere “providers of capital” and true owners of a business.

Suspicion of shallowness has not been the only barrier to more widespread ESG adoption. For some time, many institutional investors have labored under the misconception that, somehow, fiduciary duty precluded full ESG integration. Business school decision theory teaches that more choice is always better, and to those steeped in these ideas, if ESG artificially limited the opportunity set, performance-seeking investors were bound to set it aside. Yet as psychologists and behavioral economists have documented, the “paradox of choice” can lead to less than perfect decisions by humans with limited information processing bandwidth. Moreover, ESG considerations may be viewed as increasing the amount of information available to the investment decision maker, or, at minimum, the precision with which information may be interpreted. It follows then that, if ESG information is a candidate investment factor, it might be a violation of fiduciary duty not to include it. Recently, the Department of Labor (DoL) revised its ERISA guidance in tacit agreement with the latter suggestion. It explicitly said that where “environmental, social, and governance issues may have a direct relationship to the economic value of [an] investment,” these issues are “not merely collateral considerations or tiebreakers, but rather are proper components of the fiduciary’s primary analysis of the economic merits of competing investment choices.” In other words, simply ignoring ESG will no longer fly for investment fiduciaries.3

The DoL’s rule change was made in 2015. Institutional investors’ embrace of responsible investment has accelerated in the interim. The consultant Callan’s annual survey of institutional investors found that 33% of respondents not yet incorporating ESG factors into their decision process were now considering it, which is a record high for the eight-year-old survey. Yet current momentum toward adoption camouflages a broad systemic inertia. The 42% of institutional investors who do utilize ESG factors has remained flat since 2018. There is much distance to travel: in 2016 McKinsey found that less than one percent of the total capital managed by the 15 largest US public pensions was then allocated to ESG-specific strategies or those that employed ESG insights. Why, given the highly visible enthusiasm for “stakeholder capitalism” does there remain so much distance to travel? Of the many roadblocks to implementation, the challenge of measuring, quantifying, and interpreting ESG data—along with its impact on financial returns—has been foremost. But that is changing rapidly.

ESG as a profit-driver: Evidence and theory

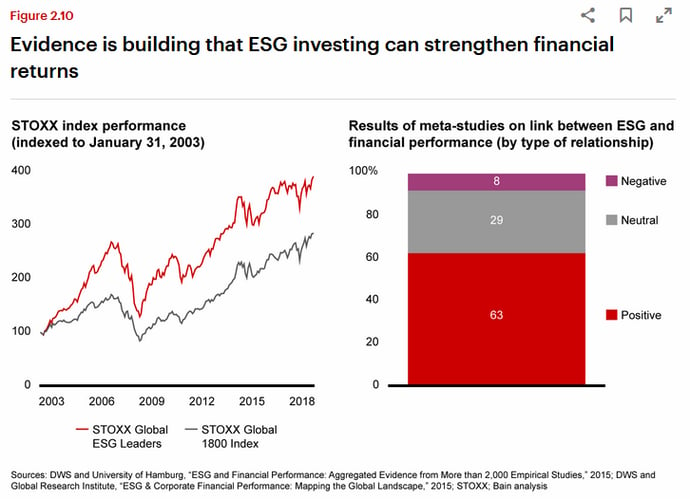

An expanding body of empirical evidence has begun to dispel the myth that taking account of ESG factors detracts from investment performance. One influential 2014 paper sorted companies within the same industry into “high sustainability” and “low sustainability” categories.4 It found that the high sustainability firms significantly outperformed their peers in on both fundamental financial and stock market measures. In February 2020, the consultancy Bain & Company looked at the performance of a STOXX index of global ESG leaders over a 16-year period and reported that it had outperformed the STOXX Global 1800 by 37%. These findings are not one-offs; broad surveys of the academic literature affirm the empirical finding that ESG is profit-making. A comprehensive meta-study undertaken by German researchers at the University of Hamburg and Deutsche Bank concluded that roughly 90% of academic research articles find a positive relation between ESG measures and corporate financial performance.5

Source: Bain

Correlation, of course, does not imply causation. Some studies report only a coincidence of top ESG scores and better financial and stock market performance. This could be because better managed firms tend to succeed on all dimensions, including ESG. Or it could perversely imply that firms rewarded by markets with lower cost of capital are better able to implement ESG initiatives.6 Teasing out causation is one of the trickiest tasks in economic research. It’s akin to a chicken-or-egg problem. But academics and financial practitioners have employed a range of statistical methods to determine that positive ESG scores are indeed predictive, and likely a causal factor in subsequent enhanced financial performance.7

In order to ascertain if ESG improvements are causative, or merely a coincident signal of fundamental success, it is necessary to develop a hypothesis of the means by which ESG steps would flow through to profits and the stock price. Harvard academics have zoomed in on the materiality criterion to better understand which types of corporate ESG efforts are likely to pay off. A 2015 study using the materiality framework of Sustainability Accounting Standards Board (SASB) found that companies that concentrate on material ESG issues do better than those who address a wider array of problems, and better still than ones that ignore ESG entirely.8

Attention to ESG factors is associate with better portfolio returns, and does not require any inherent sacrifices. Implementation, however, is not as simple as turning on a screening tool. We thus conclude that an “ESG 2.0” analysis should form an integral part of the investment process at all levels ranging from idea generation, to due diligence, to asset allocation, to risk management. Businesses must learn to speak the interrelated languages of profit and social impact. The next article in this series will address the ways that businesses and investors are implementing ESG strategies and will highlight some notable success stories. Following that, we will delve into remaining challenges to widespread adoption and discuss steps that investors can take to align their efforts with current best practice.

Please See Our Important Disclosures

[1] The recent success of the Impact category, both in impressive fundraising and competitive returns suggests that the simple labeling of the strategy as a profits-second niche may be outmoded. What was once territory dominated by small players like LeapFrog and Bamboo Capital has attracted mainstream attention. TPG is lately getting in on the act with a $2 billion raise for its second Rise Fund, while KKR and Partners Group are close behind in raising slightly smaller funds. And while “Impact” is surely one of the hardest investment objectives to measure, TPG has pioneered methods for estimating the social and environment good of each dollar invested (outlined in a 2019 piece in the Harvard Business Review. A 2019 study by the Global Impact Investing Network found that impact funds seeking market-rate returns (admittedly a small group) produced performance in excess of 16% since inception – competitive with what many LPs would expect from private equity funds.

[2] Milton Friedman laid out his vision in a 1970 New York Times editorial (https://www.nytimes.com/1970/09/13/archives/a-friedman-doctrine-the-social-responsibility-of-business-is-to.html). Corporate America in the ‘70s and ‘80s widely adopted a Friedman-inspired mantra of “shareholder value maximization”. We will discuss later the merits and demerits of Friedman’s argument, but his key point can be distilled to the following: shareholders are “residual claimants” of a business and therefore take the most financial risk. Employees, bondholders, and vendors are not seen as taking risk in a business’s success because they freely enter into contracts specifying what they will give to and receive from the company. Since shareholders are the owners, any action that corporate management takes should be primarily, or solely in the economic interest of this class of stakeholder. By maximizing shareholder profits, firms maximize the amount of cash that this crucial constituency can then deploy toward whichever social ends it desires.

[3] Other countries have gone even further. In France, the Ministry of Finance announced in 2016 rules that would require investors actively track their portfolios’ carbon emissions, as well as other ESG data points.

[4] Eccles, Robert G., Ioannis Ioannou, and George Serafeim (2014). "The Impact of Corporate Sustainability on Organizational Processes and Performance." Management Science. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1964011

[5] Friede, Gunnar, Timo Busch, and Alexander Bassen (2015). "ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies." Journal of Sustainable Finance and Investment. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2699610&mod=article_inline

[6] Krueger, Philipp. (2015). “Corporate Goodness and Shareholder Wealth.” Journal of Financial Economics. https://isiarticles.com/bundles/Article/pre/pdf/45038.pdf

[7] See Giese, Lee, Melas, Nagy, and Nishkawa (2019) [https://www.msci.com/documents/10199/03d6faef-2394-44e9-a119-4ca130909226] and Dunn, Fitzgibbons and Pomorski (2017) [https://www.aqr.com/Insights/Research/Journal-Article/Assessing-Risk-through-Environmental-Social-and-Governance-Exposures] for examples.

[8] Khan, Mozaffar, George Serafeim, and Aaron Yoon (2015). "Corporate Sustainability: First Evidence on Materiality." Harvard Business School Working Paper. https://dash.harvard.edu/bitstream/handle/1/14369106/15-073.pdf

Related Posts

ESG Investing: Purpose and Profits (Part 2)

Part 2 – How Businesses Can Effectively Integrate ESG

ESG Investing: Purpose and Profits (Part 3)

Part 3 – How Investors Can Incorporate ESG to Reduce Risk and Generate Opportunity

ESG Investing: Purpose and Profits (Part 4)

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate