14 min read

Part 2 – How Businesses Can Effectively Integrate ESG

In our last piece we took a brief tour of the ESG (Environmental, Social, and Governance) concept from its origins in the “socially responsible” investment trend of the 1980s and 1990s through its maturation as an evidence-driven investing sub-discipline, and its broadening acceptance within the business and financial communities. In this post, we will explore how businesses are reacting to the public clamor for environmentally and socially sustainable corporate leadership, and how this strategic evolution can be made to work to the benefit of investors and society writ large.

While the growth in ESG-flavored investment strategies has accelerated in the last few years, corporate leaders have responded with flashy new sustainability reports, public statements of intent, and new corporate social responsibility (CSR) initiatives. In a real sense, a new generation of CEOs is responding to changes in the public mood and the twin crises of climate change and economic/social inequality. But well-meaning words can only go so far and there remain important questions about what the private sector can really achieve toward social ends, or even what role, if any, the corporate enterprise should play. Inevitably, as ESG has become a fast-rising topic of conversation in investment circles, the increasing flood of ESG-labeled products has invited a backlash. In March 2021, USA Today published an editorial by Tariq Fancy, the former head of sustainability at the world’s largest asset manager, Blackrock. In Mr. Fancy’s opinion, much of what goes on under the umbrella of ESG amounts to “little more than marketing hype, PR spin, and disingenuous promises.” No doubt Mr. Fancy has a point; whenever demand for a particular investing strategy becomes hot, Wall Street scrambles to mass produce merchandise to satisfy it. Some of what gets sold will be poorly thought-through, self-contradictory, or worse. The USA Today opinion piece pointed to self-described ESG funds that invest in big polluters, such as oil majors. The SEC has said it is looking into ESG-related misconduct.

mood and the twin crises of climate change and economic/social inequality. But well-meaning words can only go so far and there remain important questions about what the private sector can really achieve toward social ends, or even what role, if any, the corporate enterprise should play. Inevitably, as ESG has become a fast-rising topic of conversation in investment circles, the increasing flood of ESG-labeled products has invited a backlash. In March 2021, USA Today published an editorial by Tariq Fancy, the former head of sustainability at the world’s largest asset manager, Blackrock. In Mr. Fancy’s opinion, much of what goes on under the umbrella of ESG amounts to “little more than marketing hype, PR spin, and disingenuous promises.” No doubt Mr. Fancy has a point; whenever demand for a particular investing strategy becomes hot, Wall Street scrambles to mass produce merchandise to satisfy it. Some of what gets sold will be poorly thought-through, self-contradictory, or worse. The USA Today opinion piece pointed to self-described ESG funds that invest in big polluters, such as oil majors. The SEC has said it is looking into ESG-related misconduct.

Similarly, the Economist points out that the CA100+, a group of large asset managers pushing for more corporate action to address climate change, has seen only modest progress in improving either the carbon footprints or the climate risk disclosure from its target companies. But we will argue that such efforts are not fruitless. Just as investors are learning how attention to ESG criteria can improve portfolio performance, businesses are figuring out how sustainability initiatives can improve their bottom lines—and how to communicate this information to their shareholders. This conversation between business and the Street must continue to evolve and should not be derailed by a frank admission of both sides’ temptation toward empty hype.

In this piece, we aim a spotlight on the critical issue for profit-driven businesses seeking also to drive positive social change. This issue goes by the name “Materiality.” In short, the challenge for corporate managers is to determine which environmental, social, or governance projects are most likely to improve profits. Management’s objective is to allocate capital in order to optimize long-term financial returns, as well as to reduce waste, to foster better equity and inclusion, and to generate positive social multipliers. Investors simultaneously must make efforts to understand which corporate strategies are likely to produce results along ESG as well as purely financial dimensions. No company should try to be all things to all stakeholders. Rather, corporate decision makers should seek balance between competing claims, invest where they have a meaningful competitive advantage, and focus on efficiencies. This recipe comes straight out of a professional

manager’s existing playbook. ”Materiality” only implies that the same techniques should be applied to a broader range of goals than simply maximizing short-run shareholder value. In the end, a focus on ESG materiality is an attempt to answer the question, “what really matters?”

Materiality drives investor returns

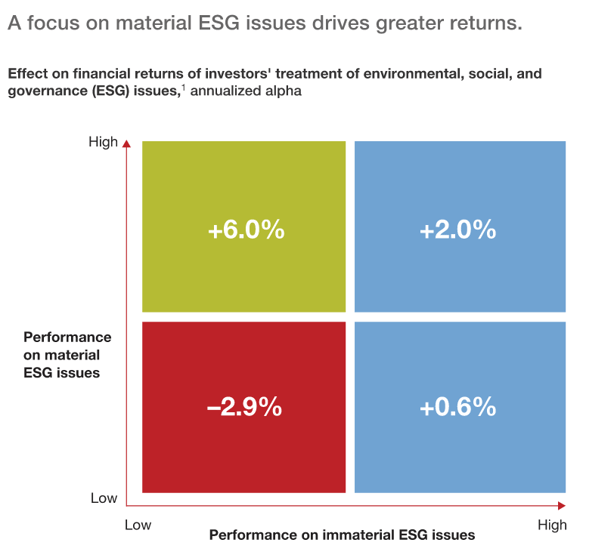

As we have previously written, firms with better ESG metrics have generally been shown to outperform broad markets. Whether ESG efforts are a cause of this success, or merely a lagging indicator, academics have a developed a testable hypothesis that would explain why ESG should be associated with financial performance. ESG initiatives aimed at addressing those matters which are most financially material to a business’s bottom line should be correlated with better returns than those that generate only public goodwill. And that is exactly what studies have found; in one 2015 paper, researchers looked at companies which disclosed investments in areas deemed material to their business by the Sustainability Accounting Standards Board (SASB). Those companies outperformed a control group of their peers which made “immaterial” ESG investments, as well as companies which made no ESG investments whatsoever.1

Source: McKinsey

Source: McKinsey

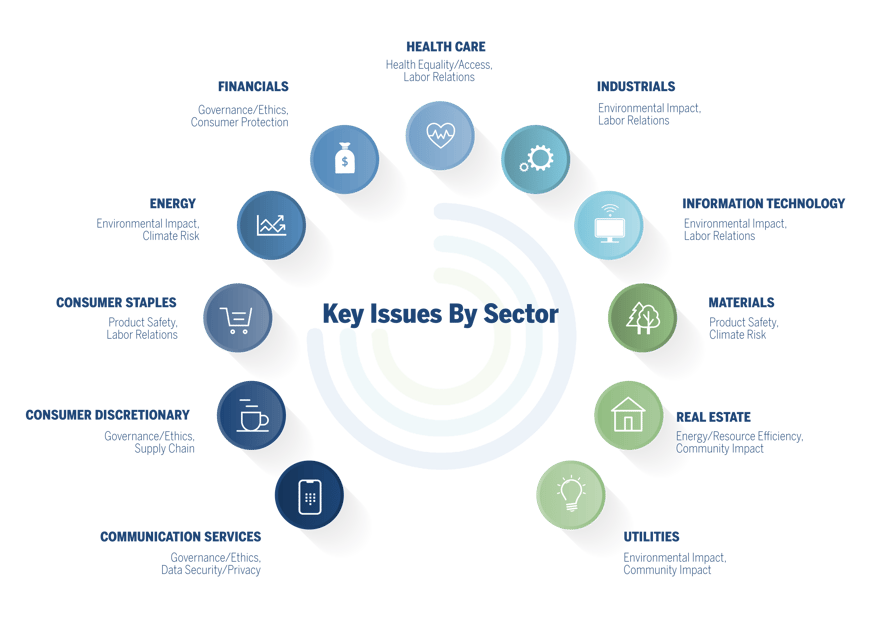

What counts as “material” remains somewhat subjective, though researchers are crafting new hybrid metrics to more explicitly capture how ESG key performance indicators (KPIs) relate to profit and cashflow. We will discuss a few of these hybrid metrics in a subsequent article. The most material issues certainly vary by sector. According to a basic definition offered by State Street, “A piece of information is material if it is likely to affect financial performance.”2 In many cases, popular ESG factors are immaterial or irrelevant to a given business and can thus cause average quantitative scores or rankings to underemphasize performance on the most critical variables. For example, when analyzing a credit card company, it might be a mistake to concentrate on its carbon footprint or water usage. But data security, anti-money laundering and consumer privacy would be truly material issues. A few years ago, when banks’ subprime, teaser-rate consumer loans invited large fines for predatory selling practices, those same banks were generally receiving positive ESG report cards. On the other hand, greenhouse gas emissions are more clearly tied to operating margins for logistics companies such as FedEx, UPS, and DHL. Likewise, water use is highly germane for apparel manufacturers. Levi Strauss found that nearly 3,800 liters of water are used to make a pair of blue jeans and has pioneered an initiative to reduce this amount by 96% across the value chain from cotton seed to finishing, saving over one billion liters in the process.3 Standardized, check-the-box ESG reporting would largely overlook this critical cost-saving benefit.

The subtlety in materiality analysis is that it depends critically on the business model. Even GAAP accounting standards differ between companies in similar but distinct lines of business. Similarly, ESG scorecards sometimes ask companies to report on “total volume of fossil fuels” employed in their supply and distribution chains. An object lesson of where such a broad question disguises the true carbon intensity of a business can be found in the contrast between Walmart and Amazon’s method of consolidation. Vertically integrated Walmart’s logistics fuel use is entirely captured by this query; Amazon’s is not. In reality, Walmart is working with its suppliers to eliminate a gigaton of carbon emissions while simultaneously reducing costs. Amazon leaves these decisions up to its sellers and third-party delivery contractors. Walmart routinely scores worse on environmental criteria than Amazon. But which is the greener business practice?

Therefore, even within retail, material inputs and outputs may hinge on the manner in which a questionnaire is framed or a value chain is organized. SASB’s materiality map, outlined in detail at its website (https://materiality.sasb.org/), is an important first step for analysis, but it is only a point of departure. In its original legal sense, materiality is a narrow concept used only for determining which risks require formal disclosure. SASB’s methodology is based in financial reporting and is not especially geared toward identifying future opportunities. Yet a broader conception of materiality could do just that. Approaches that interpret materiality most broadly leave more room for subjective weightings but are potentially more applicable for investors.

Source: WMS, Parnassus Investments4

Material benefits, material risks

The question of materiality cuts deeper than any single initiative. When companies take seriously the proposition that corporate citizenship and financial performance are indivisible, managers and stockholders alike may begin to see their commitments as congruent with a shared sense of corporate purpose. The pharmaceutical giant Johnson & Johnson is often cited as a paragon of stakeholder capitalism. It first published its business credo in 1943, which argued that the firm’s responsibilities were to customers first, then to employees, suppliers, the local communities in which it operated, and only then to shareholders. When a scandal over poisoned Tylenol capsules hit the business in 1982, line managers were empowered to take direct action and pull shipments even before corporate headquarters could issue new marching orders. The public reaction was swift and the value of JNJ shares fell, but the company survived with its reputation for integrity intact, even enhanced.

To be clear, vague, heartwarming statements of good intent (as have become fashionable in Silicon Valley) are unlikely to be embedded at all levels of firm culture. As economist Paul Collier observed in his 2018 treatise The Future of Capitalism, an unremitting sense of duty was actually common in a number of early Victorian-era enterprises—the duty to provide safe products to customers as well as good jobs and decent living standards to employees and their families, and to leave a lasting social legacy in their community. While the first Gilded Age of corporate industrial capitalism is justly infamous for Dickensian squalor and rapacious robber barons, earlier magnates like Richard Arkwright, Robert Owen, and Josiah Wedgwood viewed their industrial concerns as social missions and laboratories for progressive reform.

It isn’t fair to assume that capitalism is incompatible with serving wider society; only that the increasingly narrow conception of shareholder value has become too myopically devoted to short-term profits at the expense of lasting “shared value.” Companies like Johnson & Johnson and Unilever provide a viable alternate model. Business professors George Serafeim, Claudine Gartenberg, and Andrea Prat are dismissive of the trend for bland mission statements along the lines of “Our mission is to elevate the world’s consciousness”. Rather, in their view, true clarity and unity of purpose--which can be reflected in worker surveys--is the fundamental driver of shareholder returns.5 The umbrella idea of ESG in fact subsumes a tremendous variety of routes for companies to credibly deliver on social purpose.

It isn’t fair to assume that capitalism is incompatible with serving wider society; only that the increasingly narrow conception of shareholder value has become too myopically devoted to short-term profits at the expense of lasting “shared value.” Companies like Johnson & Johnson and Unilever provide a viable alternate model. Business professors George Serafeim, Claudine Gartenberg, and Andrea Prat are dismissive of the trend for bland mission statements along the lines of “Our mission is to elevate the world’s consciousness”. Rather, in their view, true clarity and unity of purpose--which can be reflected in worker surveys--is the fundamental driver of shareholder returns.5 The umbrella idea of ESG in fact subsumes a tremendous variety of routes for companies to credibly deliver on social purpose.

Understanding materiality is thus the key to understanding the link between ESG-themed capital projects and improved financial performance. These efforts should be easily explainable within the context of an organization’s existing commitments—to its workers, to its customers, to its community. Looking at the differing contours of companies’ sustainability plans can highlight the channels through which ESG impacts the bottom line. Are they aimed at cost reductions by reducing waste through the value chain? Are they focused on brand differentiation? Are they directed toward growth by entering new markets or new product categories? Is their goal to expand cultural and cognitive diversity among senior management? To improve promotion and retention of talented women and underrepresented minorities? Different ESG strategies will impact cash flows in different ways. Firms might equally employ an ESG decision-making framework to make more efficient use of resources, to encourage more innovation, to improve workplace culture, to modernize long-range planning, or to enact better targeted incentives for senior management. Any of these actions could translate into ultimately higher profitability and higher returns for investors.

Another way that highlighting material ESG factors can benefit stockholders is through risk reduction. Companies with strong ESG characteristics often have above-average corporate compliance standards and risk controls. These companies are therefore less likely to be victims of fraud, embezzlement, or litigation that would impact the stock price. In this sense, ESG is a form of self-insurance. The implication for shareholders is that looking at ESG can both reduce stock-specific idiosyncratic risk and lower tail risk.

Finally, there is a case that a company that improves its ESG profile is also less vulnerable to market shocks (such as pandemics or environmental catastrophes) and may therefore have lower systematic risk as well. In corporate finance theory, lower market risk (lower “beta”) results in a lower equity cost of capital. For example, energy companies with decreased exposure to dramatic shifts in commodity prices have had share prices less sensitive to these risk factors and have therefore enjoyed lower equity risk premiums and lower discount rates. These companies become commensurately more valuable to investors. In each of these avenues, ESG momentum (e.g., improvement on ratings scores) is a financial indicator worthy of watching.

A few more examples should suffice to give a sketch of how these multiple channels can yield a profusion of diverse opportunities to remake production processes and management practices. In one case study by Porter, Serafeim, and Kramer, Nike created a shoe made from a single strand of material, effectively cutting production waste to zero. Not only was this shoe—the Flyknit—cheaper to manufacture, but it was also lighter and more breathable, resulting in over $1 billion in sales. Fellow Harvard professor Rebecca Henderson offers a different example of successful ESG leadership by Nike. In the 1990s the company was stung by discoveries of forced child labor throughout its South Asian supply chain and found that it alone could not fully audit its web of suppliers. Instead, Nike created an industry-wide organization called the “Sustainable Apparel Coalition” which was effective at enforcing higher standards among suppliers to all Western brands. Addressing a PR headache for the brand, the initiative also helped Nike resuscitate its overall reputation as a sustainable sportswear company while building a more reliable supply chain for itself.

A similar investment was made by the minerals company BHP, which spent over $50 million to upgrade the quality of its local suppliers to its Chilean mines. In addition to improving the physical infrastructure and business environment in some remote Andean regions, BHP also catalyzed a cluster of world-class mining suppliers that generated more than 5,000 jobs and saved the company over $120 million in business value. Investments in human capital need not take place only in far-flung locations. The Starbucks program offering online college courses for free to its employees has helped drive success in recruiting. It also contributes to improved employee morale, retention, and productivity. A comparable effort at JetBlue has positioned the airline as one of the best places to work in the industry. While these programs appear to drive value and are likely material, they might not be heavily weighted in ESG ratings.

Lastly, we turn to an example of opportunity gained and lost. While the Italian energy company Enel has made over €85 billion in renewable energy investments since 2014 (and announced plans for €160 billion more by 2030), most of its rivals have doubled down on legacy coal and gas generation capacity. Alongside Enel, another notable exception is the Spanish utility Iberdrola. As the cost of renewable generation has plummeted, Enel’s investments now look savvy while its peers’ higher-cost conventional generation assets appear increasingly uneconomic. According to Porter, Serafeim, and Kramer, the inertia shown by Enel’s continental rivals has resulted in the destruction of $550 billion in economic value across the European utility industry. Enel, Iberdrola, and the American utility/renewable developer NextEra are among the most valuable energy companies in the world today.

When “shared value” is incorporated into corporate strategy, it can open new markets or new opportunities in several mutually reinforcing ways. Productivity enhancements can take shape either through exploiting efficiencies or improving productivity of employees and suppliers throughout the supply chain, as in the Nike example. As BHP discovered, it can improve the overall business environment, leading to new industry clusters. Finally Enel and Iberdrola illustrate how viewing opportunity through a broader social prism can create entirely new business segments that cater to unserved customer needs or address an emerging source of demand. Inevitably, as with any long-term investment, some ESG plans will result in resource misallocation. It is up to capital markets to identify those with real promise and finance them on reciprocally beneficial terms.

We acknowledge the possibility that much of what is touted by companies as “ESG” is superficial spin. Yet, looking closely at businesses through the lens of financial materiality can uncover real opportunities to boost profits. ESG investors should not simply load portfolios with companies in low-carbon industries, or with stellar reputations. They should dive into annual reports, comb through financials, and engage with management to learn which initiatives are underway that can drive shareholder value while at the same time syncing with a broader social or environmental purpose. Such initiatives may or may not be captured by ESG scorecards. A gold rating is only the start of the analysis; by looking closely at what matters for all stakeholders, ESG investing programs can truly add value.

[1] Khan, Mozaffar, George Serafeim, and Aaron Yoon (2015). "Corporate Sustainability: First Evidence on Materiality." Harvard Business School Working Paper. https://dash.harvard.edu/bitstream/handle/1/14369106/15-073.pdf

[2] Eccles, Robert G. and Mirtha D. Kastrapeli. (2017) “The Investing Enlightenment: How Principle and Pragmatism Can Create Sustainable Value through ESG.” State Street Report. https://www.statestreet.com/content/dam/statestreet/documents/Articles/The_Investing_Enlightenment.pdf

[3] Unilever, whose former CEO Paul Polman pursued a relentless emphasis on sustainability and social responsibility, saved over $1 billion from reducing its water, energy, and materials use across its product lines. In 2020, the company went further by pledging over $1 billion in spending to get to net-zero emissions by 2039 and reduce usage of non-recycled plastic by half by 2025. Unilever, for instance, has saved $1 billion since 2008 by proactively cutting its water, energy and materials usage.

[4] Adapted from Parnassus Investments' ESG Approach Brochure.

[5] Gartenberg, Claudine, Andrea Prat, and George Serafeim. (2019) “Corporate Purpose and Financial Performance,” Organization Science. https://dash.harvard.edu/bitstream/handle/1/30903237/17-023.pdf

Related Posts

ESG Investing: Purpose and Profits (Part 3)

Part 3 – How Investors Can Incorporate ESG to Reduce Risk and Generate Opportunity

ESG Investing: Purpose and Profits (Part 4)

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate

ESG Investing: Purpose and Profits (Part 1)

Part 1 – No Longer a Backwater

In the last two decades, ESG (“Environmental, Social, and...