5 min read

In a previous post, we discussed why private equity remains a stalwart of long-term portfolios seeking higher returns than those available in public markets, despite its increasing popularity among nontraditional investors. Now we turn to positioning within the private investment asset class and consider why sensitivity to economic conditions may be important to maximizing risk-adjusted returns. Finally, we consider our abilities in this area and discuss our view of the landscape for private investments in 2020 and beyond.

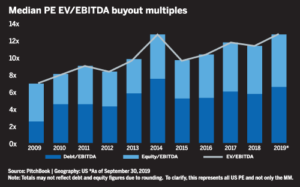

Where are we in the cycle? It’s difficult to say which inning we are in, but we are confident in projecting that funds raised today will, on average, see fewer enthralling returns than in years past. The public equity markets’ lack of enthusiasm for many of the most hyped unicorns’ cash-burning business models is one sign. Another is the increasing compression in the performance of top quartile and bottom quartile managers. When a wall of money bids up all private assets, returns become more correlated. The Economist recently reported on the flood of cash hitting late stage private growth companies. At the beginning of 2019, data provider Prequin noted as much as $2.1 trillion of dry powder in the sector, an astonishing hoard that has likely only grown over the course of the year. Much of this investment has come from “tourists” to Silicon Valley’s venture ecosystem, like Softbank’s $100 billion Vision Fund, or from traditional asset managers. To quote the Economist,

“The damage done by SoftBank is incalculable,” says one Silicon Valley bigwig. “If you make a firm go faster, it does unnatural things.” There is a growing sense that capital is being wasted. “Businesses that shouldn’t be funded are getting funded,” says another VC. Sales and marketing budgets are swollen. Firms lose track of whether their product is any good.

Finally, if you are looking for a possible canary in the coal mine, it is often a good bet these days to turn towards China. The Wall Street Journal wrote that the Chinese venture-capital boom, responsible for a number of consumer internet and e-commerce behemoths, “has come to an end”. Fundraising and deal volume have slowed and private company valuations have stalled above levels they may be able to fetch in public markets. As the tide goes out, we may see a raft of “zombie” investments and stranded capital. To be sure, Chinese capital markets are less developed than the West’s, but much of its inflows came from Western institutions. If you burn your hand in Shenzhen, are you more likely to switch to Palo Alto, or to back away from the stove entirely?

As long-term participants in the private investment universe, our view is somewhat more complicated. It would be a mistake to retreat from an asset class with such a proven ability to outperform liquid investments on the basis of a few anecdotes. We see dozens of private equity pitches a year, and we are cognizant that as return expectations come down and potential risks go up, it is surpassingly important to select your partners carefully. We are diligent in underwriting management teams, economic drivers of return, and exit strategies. To assume that the public markets are eagerly waiting with an infusion of new equity at just the right time, as WeWork seems to have, is, in our view, always a mistake, regardless of the environment. Instead, we look to managers and strategies that have a distinct edge in their markets (often sector specialists), and who take an active role in guiding their businesses’ growth rather than relying solely on leverage or financial engineering to generate returns.

We focus our attention on private equity managers who possess hands-on operating expertise to drive tangible value creation at portfolio companies. Why does an emphasis on value-added strategies make sense at this point of the cycle? As we wrote in our last blog, much ink has been spilled recently over concerns that too much cash is chasing too few deals, or that we may be approaching “peak private equity”. We share these apprehensions; this is why we look for deals sourced away from auction. Similarly, we agree with the Yale Endowment CIO David Swensen who writes, “Pure financial engineering holds little interest for serious private equity investors, since providing financing represents a commodity-like activity with low barriers to entry.”[1]

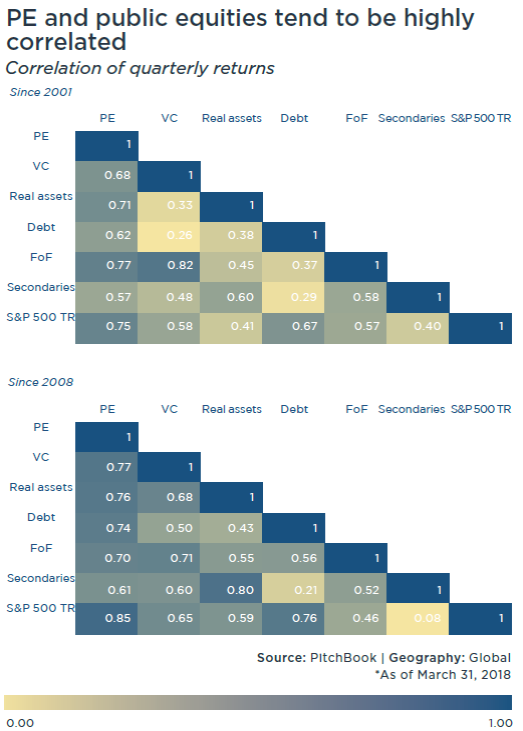

We believe that the “hands-on” value add is a critical part of the private equity value proposition. As the correlation matrix below shows, much of what private equity does may represent merely a leveraged play on the same economic drivers propelling public markets. This is likely most true of late stage, pre-IPO growth investments, of mega-buyouts in competitive public markets, and of funds that seek a short-run “flip” of a business, often to another private equity group. We prefer operational know-how not only because it improves results, but because it embodies a return driver largely uncorrelated with marketable securities. Trading companies in-and-out of public markets or simply adding leverage does not diversify market risk. Building and growing businesses over the long-run does.

Alternatively, one can earn attractive risk-adjusted returns in a late-cycle environment from being a ready liquidity provider as the tide goes out. Secondary market LP investments seem interesting should the spigot to private growth companies be turned off, or if exits come slower than expected. Institutional investors are already beginning to adjust their valuations of certain unicorns. As some look to exit, reductions in fund valuations should create an attractive entry point for patient investors.

Above all, we favor private investments with stable, noncyclical cash flow streams. The “private equity” fund structure encompasses innumerable investment possibilities beyond simply equity. These may include middle market direct lending, other forms of private credit, or real estate where we team with strong operational expertise have the ability to drive increasing cash flow even as broader valuations become stretched. We have found interesting opportunities in such emerging asset classes as drug and entertainment IP royalty streams, which, while structured as equity, offer a risk/return profile between equity and debt. We are generally agnostic as to whether an investment is labeled “debt” or “equity”. What matters is the economic drivers of return. Often, we find the best opportunities reside outside of, or at the borders between conventional categories.

These criteria can also accommodate growth stage or bridge investments that are conservatively structured as a preferred return with upside optionality in profitable or near-profitable businesses. In short, we would not deemphasize the entire asset class as the cycle extends, but we do embrace a defensive rotation within private investments taking place toward those that are more liquid, more durable, or more attractively valued. To be sure, return expectations will have to come in from the 30% annual gross numbers that were cited in the early post-crisis years.

In the end, we are vigilant stewards of our clients’ wealth. We want to preserve it and take only risks for which our clients are appropriately rewarded. Like our clients, we are risk averse. Reaching down-market, down-in-credit, or to less robust structures does not promise good odds over an intermediate horizon. For those reasons it is all the more important to be highly selective with respect to general partners, to sectors, and to projections about multiples. If we are correct and fund dispersion increases going forward, the value of due diligence only increases as well. We may have to see a few more pitches before we swing.

[1] Quote from Swensen’s landmark textbook, Pioneering Portfolio Management (Free Press, 2009).

Related Posts

The Enduring Appeal of Private Equity

The below is the first in a series of articles on private equity from the WMS Investment Committee.

Middle Market Private Equity: The Art of Picking Your Spots

In our last entry, we wrote that inflation and monetary tightening were returning investors to a...

ESG Investing: Purpose and Profits (Part 4)

Part 4 – Frontiers for ESG Investors: Fixed Income, Private Equity, and Real Estate