21 min read

Key Points

- The pathway to a sustained, durable recovery in 2021 is now far clearer than it has been.

- With the election behind us and Washington gridlock likely, financial markets should benefit from the extension of the status quo and the deferral of many of the most radical policy proposals.

- With the recent news on vaccines, we believe both a substantial economic recovery and historic growth in S&P 500 earnings are likely for 2021. Built on the continuing strength of consumer balance sheets, we should see an unleashing of pent-up demand for COVID-sensitive outlays like travel and leisure.

- Although we continue to like the business prospects for high-flying tech companies, we are more attracted to the modest valuations and earnings recovery prospects for domestic cyclical stocks as well as to the improving dynamics for international and emerging market equities.

For weeks, if not months, we have been meeting (virtually) with clients, game-planning how to position portfolios around a number of upcoming catalysts. These have included the presidential election, control of the Senate, potential changes to the tax code, the path of the coronavirus pandemic, the possibility for a medical breakthrough, etc. So far, we have resisted the strong temptation to write a single market update with its inevitable obligation to make some sort of forecast. We have held our fire for so long because, whatever opinions we at WMS might have, investors have been faced with such irreducible uncertainty that the best we could offer would be a range of scenario analyses—“if, then” propositions each depending on variable states of the world, clients’ financial situations, attitudes toward risk, and so on. This didn’t strike us as very appealing reading.

Today, on the eve of a Thanksgiving holiday that will likely prove the most surreal and socially distant in a century, we believe that there is at last a foundation, not of certainty, but at least of conviction to render analysis and advice. The virus that has plagued society and the economy in 2020 is not retreating from the scene; on the contrary, the public health situation in the United States is more perilous than it has ever been. Nor has the virus of political rancor that has made discussion of current events feel like a Civil War battlefield receded. There is a nonzero probability of a constitutional crisis before the Electoral College meets in December that might introduce a dimension of political upheaval unseen in America since the 19th century. But notwithstanding all these near-term sources of risk and confusion, there is indeed a clarity on the horizon that did not exist only a few weeks ago. The news of Joe Biden’s narrow, yet clear victory, of Republican gains in the House of Representatives and probable hold of the Senate, and now of three highly efficacious COVID vaccines likely to be approved before year-end, has had the effect of reducing ambiguity about the future by a tremendous margin. It is commonly said that there is nothing equity markets hate so much as uncertainty. By implication, a reduction in the cloud of obscurity is very good for risk assets. Accordingly, the VIX, or “Fear Index” dropped from a level of 40.28 on the eve of the election to 22.45 on November 16. During that time, the S&P 500 rallied 10.9% in price terms. The pathway to a sustained, durable recovery in 2021—of GDP, of jobs, of earnings, and foremost of our long-interrupted social routines—has never been clearer.

The Election and the Benefits of Gridlock

The markets appear to believe that Biden’s victory makes the prospect of another dose of stimulus more likely, albeit not until after his January inauguration. It will be sorely needed. Many CARES Act provisions, such as eviction protection and extended unemployment benefits, will run out after Christmas. The $600 per week federal enhanced relief expired in July, while its $300 per week replacement has also gone. States and municipalities are in the process of furloughing staff, axing infrastructure projects, and reducing school funding. Many small businesses, hit by renewed closures this winter, will need another shot of PPP assistance. Last month, House Democrats and Senate Republicans were $2.4 trillion apart in their proposals for the size of a second relief package; as unemployment data have improved, debt-conscious GOPers have scaled back what they are willing to countenance. The consensus seems to be that a meeting somewhere in the middle, say around $1.5 trillion might be achievable, particularly if the virus situation remains grave through year-end. Estimates of the effects on growth of a marginal trillion dollars of federal spending range widely but coalesce around 4 to 5% of GDP in 2021. As Jamie Dimon, CEO of J.P. Morgan, aptly said, “You’ve got to be kidding me. Just split the baby and move on.”

Still, the logic of political compromise, one of the central tenets of the president-elect’s campaign, may be naïve. Since the summer, we have believed the outlook for fiscal policy was overrated. If Republicans couldn’t unite around a fiscal injection to support their party’s flagging candidate, is it likely they will make common cause with a “socialist” president touting green jobs, long-term extensions of the dole, and “bailouts” for lawless and imprudent municipalities? Biden’s putative skill at reaching across the aisle will be sorely tested. That said, there appears reason to believe in a fiscal put at some level; even the Senate’s budget hawks acknowledge the need for relief of one kind or another. Last spring, the speed of deterioration in economic conditions spurred Congress to act. They may be called to do so again, as the perception mounts that markets have passed “peak Fed”. Having established an inflation catchup regime but stopped short of yield curve control, the central bank has likely spent the last of its ammunition, at least for some time.

Looking out past January, there is cause for markets to cheer the surprising success of Republicans in down-ballot races. Conventional wisdom holds that divided government is good for stocks inasmuch as it reduces policy uncertainty. If Democrats fail to win both Senate run-offs in Georgia, as seems likely, Biden will be the first president since George H.W. Bush inaugurated without majorities in both houses of Congress. The prospects for his most ambitious plans—on taxes, on climate, on healthcare—have dimmed significantly. For the president-elect to deliver any legislative achievement, he will have to work with moderate Republicans, such as Mitt Romney, Lisa Murkowski, and the recently reelected Susan Collins. This will water down more radical campaign promises that might have raised corporate and personal income tax rates, imposed costly regulations on business, or had severe repercussions on the entire for-profit healthcare industry. This is just fine with markets. The status quo has been very good to stocks over the past four years. In the long-term, the United States’ patchy infrastructure, education, and healthcare systems will need an overhaul, and climate change will need to be addressed proactively in Washington. But such lofty goals must be negotiated or deferred, giving investors a certain length of runway to adjust their allocations.

Longer term, we may see a return to austerity, as happened in the wake of the Great Financial Crisis. We believe this was a mistaken policy that emphasized arbitrary debt-to-GDP targets at the cost of a faster recovery. With private sector demand functionally knee-capped, the lack of more significant public spending (with government borrowing costs at then-record lows) weighed down the economy and contributed to ten years of disinflation. Today, economic fundamentals appear in better shape, and policymakers have become less jittery about debt. But forecasts (like ours in June) for an emerging reflationary paradigm assume that the lawmakers who pushed austerity after 2008 did so in good faith. Fiscal hawks who were silent about a $2 trillion tax cut may be raptors of convenience only; it may be to their advantage to play the electoral politics of obstruction as they look out to 2022 and 2024. We believe that multipliers to government spending in a recession are significantly above 1. If a sluggish economy persists through next year and Washington fails to release the handbrake, more than a point could be shaved off trend growth. That is to say, there are both positive and negative effects of gridlock, both in the short and long runs.

COVID Vaccines: A Jab of Hope

Since the spring, we have held that the vista for medical interventions, including vaccines, was very promising. Against rampant skepticism, we believed the speed records, scientific challenges, and technical snafus were likely to be overcome thanks to the sheer amount of resources—financial and human—being thrown at the problem. We continued to believe in the stock market rally, even as a second wave of virus raged through the Sunbelt over the summer. Now the light at the end of the tunnel has arrived, and it is even brighter than we might have expected. Both Pfizer-BioNTech and Moderna have produced mRNA vaccines that have shown themselves to be clinically safe and effective for at least 94.5% of patients. AstraZeneca is not far behind. Yes, there remain regulatory, distribution, storage, and delivery challenges (not least the problems of ultra-cold-chain transport). But the arrival, in less than 10 months, of an effective vaccine from a previously unproven technology is something to celebrate and marvel at. Experts assure us that much of America will be able to be vaccinated by the end of the second quarter, with mass inoculations beginning as soon as next month. Hotel, airline, and cruise line stocks shot up on the Pfizer news. Life may feel a bit like normal by next summer, even if mask-wearing and handwashing stay with us longer, if only to protect the unvaccinated.

We believe a substantial economic recovery is likely in the cards for 2021, regardless of the likelihood of stimulus. There is much pent-up demand for COVID-sensitive products and services, from travel to see loved ones, to business clothes, to dining out. Unlike in 2008, consumer balance sheets entered this crisis in good shape, and consumers used stimulus checks they couldn’t spend on airfare to reduce credit card balances instead. Rather than retrenchment, as the economy opens up, for those fortunate enough to work from home and eager to send children back to school, 2021 may feel like a party.

We have to get through a very, very difficult period first. As of writing, the United States was logging a record 180,000-plus new cases per day. Hospitals are strained to the breaking point, simultaneously battling capacity constraints while struggling financially due to the reduction in profitable elective surgeries. And while treatment of COVID has improved to the point where death rates are much lower than in April, the sheer numbers of infected and stress on resources mean that deaths are likely to continue to rise. Though the vaccines are coming at an unprecedented clip and look to be effective and safe, they will likely not arrive fast enough to avoid a situation where more than 2,000 Americans are dying each day. This will be more than three times worse than the worst air crash in history. Every single day.

Estimates vary since the extent of behavioral and local government responses is unknowable, but even some of the most optimistic forecasts see at least 400,000 Americans having died of the virus by March. Sadly, many of these deaths will have be preventable, and will come on the eve of a medical breakthrough that will save countless more lives. As we have said many times, the economic situation is the public health situation. Until this emergency can be resolved, it simply is wishful thinking to expect anything resembling economic normality this winter. As we write, shutdowns and school closures are happening around the country and around the world once again.

Yet stocks and other financial investments are forecasting machines. They are most interested in long-run streams of cashflows. Stock investors “look through” temporary disruptions to cashflows when they can be confident the disruption is only temporary. Hence, we expect that, if there is no unforeseen vaccine setback, throughout the darkness of winter, stocks will remain focused on the dawn. Horrible headlines about death and disease may not deter the S&P from pushing towards 4,000. For those who lose their jobs or for businesses that shutter, the damage may well be permanent. Preventing such losses should be the aim of any stimulus. But, for investors, the time to take risk—by maintaining investments in equities, in credit securities, in economically sensitive private assets such as real estate, is now. Within equities, the rotation that has already begun into cyclical sectors like travel, tourism, leisure, and industrials should continue.

The Surprisingly Resilient U.S. Economy

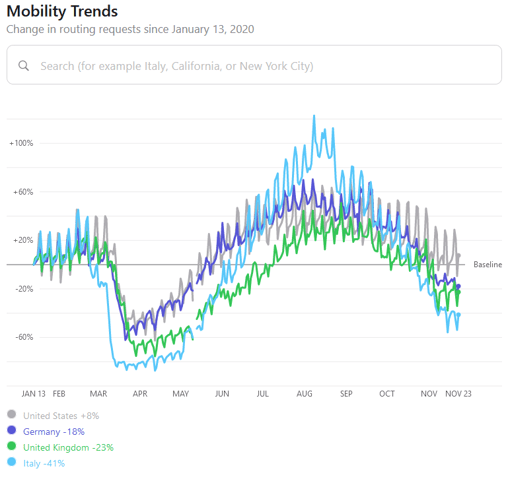

Americans are getting sicker with COVID faster than any developed country. In some respects, this is due to a fragmented and sclerotic public health response. In many others, it is a product of behavior. Taking mobility trends as a rough gauge of activity, America has not been through the self-imposed shutdowns that much of Europe has. High frequency indicators suggest that the U.S. economy has slowed since the summer, but it does not appear likely to double-dip like the Eurozone. Consumer spending will drop as cities impose restrictions on businesses such as restaurants, but analysts continue to forecast sequential growth in GDP through next year.

Apple Mobility Trends Report - https://covid19.apple.com/mobility

The labor market too is in surprisingly good shape. The unemployment rate has fallen far faster than virtually anyone predicted, from 14.7% in April to 6.9% last month. The current rate of private sector job adds would be enough to return the labor market to its pre-pandemic level in 2021. The IMF had predicted in April an annual drop of 6% in GDP, while in June the Federal Reserve saw year-end unemployment landing at 9%. The economy has easily cleared those estimates; on the current path, output will drop only 4%, much less than in 2008.

Many have noticed the unevenness of the recovery. Bifurcation in the economy has spawned a new metaphor: the “K-shaped recovery.” Service workers, the young, the less well off, and minorities are being hit far harder than white collar professionals for whom the main consequence of lockdowns has been bingeing Netflix and keeping an eye on unruly children. Low-income households accounted for 68% of the private sector job losses from February to April, according to Morgan Stanley. While the headline unemployment number is 6.9%, the U-6 number, a broader measure that counts those in part-time or gig work as unemployed, stands at 11.6%. On the whole, there will still be 10 million fewer jobs on December 31 than there were before the pandemic. One quarter of small businesses remain closed.

Despite the wreckage lockdowns and social distancing have heaped on business plans, the pace of commercial bankruptcies has been rather slow. Relief from the PPP, while flowing disproportionately to larger and more sophisticated operations, is one reason why. The Fed’s Main Street Lending Program has not offered much actual support, with only $4 billion being lent to small and mid-size enterprises. Rent relief from landlords has been a critical lifeline for service businesses such as salons, gyms, and movie theaters.

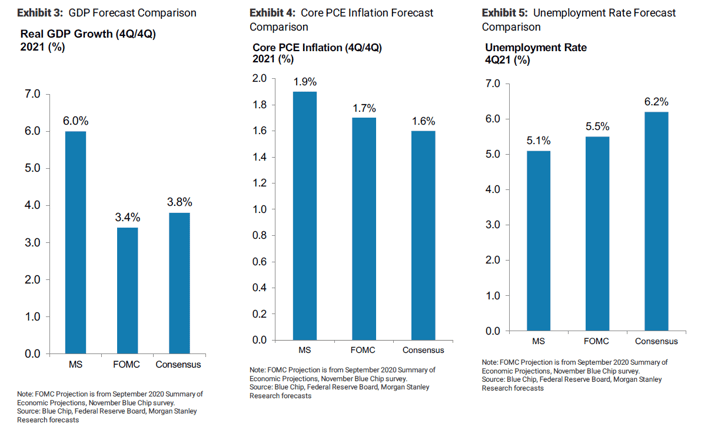

But the main driver of America’s economic pep has undoubtedly been the consumer. Credit card data show little drop-off from 2019 in consumer purchases. While spending on services has naturally lagged, durable goods spending was 5% higher in September than immediately before the pandemic, while spending on nondurable goods registered 14% above its February level. With consumer finances entering the pandemic in robust health, and $1,200 checks hitting bank accounts, Americans actually had more disposable income during the depths of the contraction than at the previous peak. The strength of the consumer has some forecasters, such as Morgan Stanley, inching growth and inflation estimates up, even as the coronavirus map says “uncontrolled spread” across most of the U.S.

Morgan Stanley's economic forecasts

We have written separately on inflation, but it is not surprising to see Core CPI and inflation expectations looking perkier than in the pandemic’s first few months. We think as consumers return in 2021 to spending on services such as weak CPI components like flights, hotels, and restaurant meals, inflation can climb from 1.6% towards 2.0%. The Fed would welcome this development and would certainly not slam the brakes as it did in 2018. Thus there is ample scope for yield curves to steepen. The Fed has essentially committed to keeping its main policy tool, the Funds rate, on hold through 2022, even as the recovery further takes hold. While the next step is tapering asset purchases, this is unlikely to happen next year as monetary policymakers will want financial conditions to remain highly accommodative while unemployment is still significantly above its previous low. Leaving aside the debate about where inflation is going in the long run, it is a fairly safe bet that U.S. ten-year yields will rise sustainably above 1% in 2021, perhaps as high as 1.5%. The signal the Fed is sending investors is to stay short in fixed income duration and to take risk in equities and credit.

Stocks and Bonds: Where Is There Value?

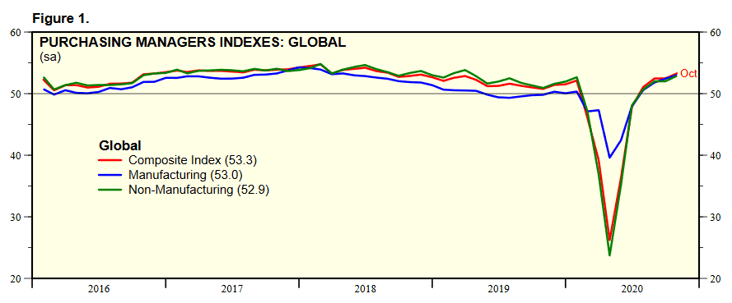

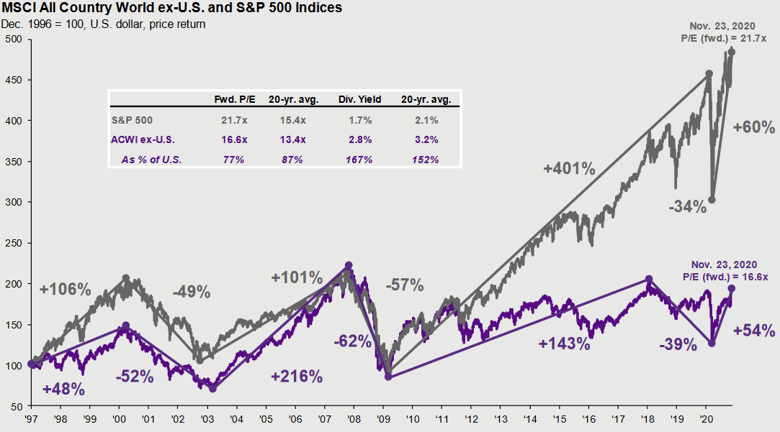

Given the expectation for broad-based global recovery taking hold throughout next spring, how ought investors position portfolios? Global spending and fixed investment have held up well, led by East Asian countries who have largely avoided the carnage that the pandemic has visited on the West. Global PMIs, which are firmly in positive territory, tend to correlate with year-on-year growth in the MSCI World Equity Index. But the latter has ample room to catch up. Through October 31, the MSCI World was down 1.4% for the year, and the All Country World Index-ex USA was down 7.5%. International stocks have rallied since the vaccine news, but they are still trailing the momentum in the global real economy, which Goldman Sachs projects will be up 6% in 2021.

Ed Yardeni. https://www.yardeni.com/pub/ecoindglpmi.pdf

Those who have read our recent writing will not be surprised to hear that we believe there is compelling value in international stocks, particularly smaller capitalization companies. The valuation gap vs. the U.S. is unusually high since America has a larger share of “COVID winners”. As we exit the pandemic, look for a rotation into non-U.S. securities as cyclical sectors catch up to the pace set by information technology and internet companies. But there are structural as well as short-term trends auguring well for international equities.

JP Morgan Guide to the Markets. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

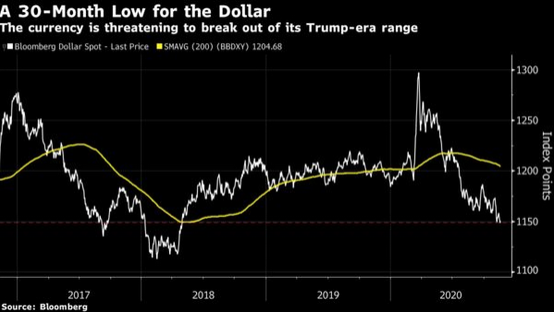

The dynamics appear even better arranged for investors in emerging markets. While Wall Street has been hitting new records, EM stocks are considerably off their highs of 2018, or even 2007. According to the Economist Intelligence Unit, the GDP of emerging economies, weighted by their stock market capitalization, will shrink by less than 2% this year, and then grow by more than 5% in 2021. Economies levered to China’s strong resurgence have held up exceptionally well. Moreover, the U.S. Dollar hit a peak in early 2020 and has been trading down for most of the year, which removes one of the major impediments to competitive returns in international stocks. With real yields below zero and the Fed reiterating its commitment to low rates, the stage is set for continued dollar underperformance. Taken together, emerging East Asia has fared much better than the West in limiting the direct and indirect fallout from COVID-19, and has stronger trend growth, a better demographic profile, improving financial conditions, and cheaper valuations. With the dollar set to continue weakening, you would need an excess of confidence not to allocate to Asian assets.

Bloomberg. https://www.bloomberg.com/opinion/articles/2020-11-18/small-stocks-revival-hints-at-dotcom-bust-danger-for-fangs?sref=CWVdwe0e

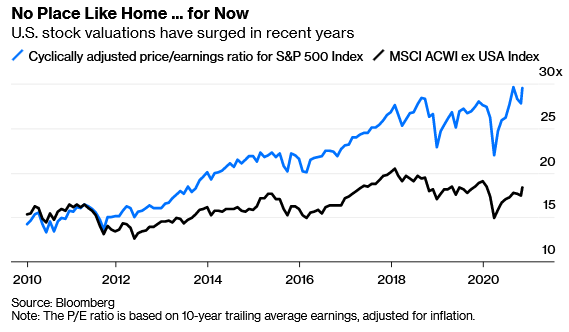

U.S. investors’ home country bias has only grown as the S&P 500 has lapped the rest of the field during the pandemic. That said, there are many reasons to stay positive on the U.S. stock market. Foremost, the Fed’s dovish policy stance is bullish for equity multiples. There remains ample liquidity sloshing around money markets and short-term bond funds, and financial conditions are exceptionally loose. Many of the companies most challenged by the pandemic piggybacked on the Fed’s guarantee of a backstop on corporate bonds to reset their balance sheets over the spring and summer. S&P 500 earnings appear poised for a historic recovery; Goldman Sachs is among the most bullish on the Street, calling for $175/share in 2021. If you apply today’s 22x forward multiple to that number (assuming zero earnings growth in 2022), you derive a 3,850 level for the S&P 500, more than 8% higher than the reading as we write on November 20. Add in a 1.8% dividend yield, and it’s not difficult to imagine double-digit returns in U.S. stocks over the forthcoming year.

But the picture for domestic equities is even more interesting than the corporate earnings recovery story. The top five stocks by market cap in the S&P 500 (Amazon, Apple, Facebook, Google/Alphabet, and Microsoft) have risen by nearly 50% in 2020. The remaining 495 S&P stocks are up only about 5%. The Russell 2000 of small-cap stocks has returned roughly 7%. Cyclical companies, value stocks, banks, and anything related to travel are generally far off their highs and are cheap by recent standards. The enormous depth of the current chasm between value and growth stocks reflects the bifurcation of winners and losers in the current K-shaped recovery as well as the winner-take-all nature of digital platforms and the network effects that drive their adoption. As such, the dispersion seems unlikely to completely disappear any time soon.

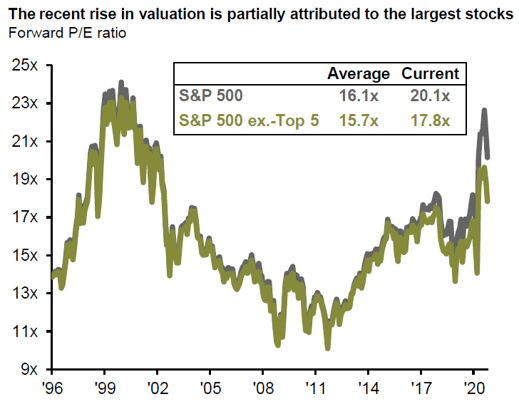

Although we have long been cheerleaders for the consistent revenue growth and unmatched earnings power of the technology titans and some of their smaller siblings, and even recommended buying a few when they were temporarily knocked off their highs in March, we see grounds to focus equity purchases elsewhere. For one thing, there is increasing scrutiny of the monopolistic position of the mega-cap tech firms. For another, they have been beneficiaries of a flight to relative safety that may be reversed as more companies begin to participate in economic growth. The top five stocks represent over 20% of the S&P 500, an extreme of concentration that looks certain to mean revert at some point. The below chart from J.P. Morgan highlights how the valuation of the S&P 500, after stripping out the top 5 companies, is quite moderate in a lower-for-longer interest rate world.

JP Morgan

JP Morgan

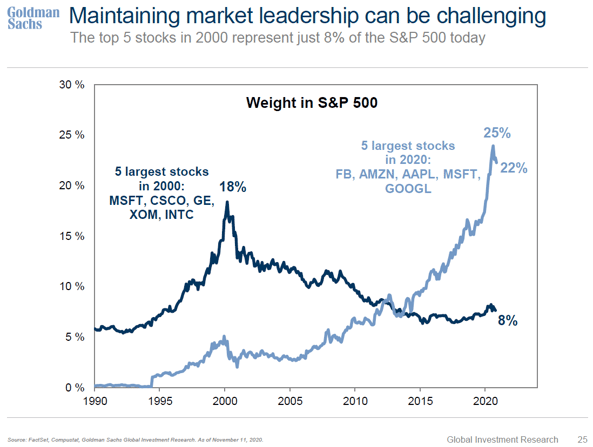

The record concentration of the large-cap index in only a few names invites a historical analogy to the peak of the tech bubble, as Goldman Sachs points out (see below chart). While investors in Microsoft at the peak of the 1990s bull market are still sitting on profits, they would have endured more than a decade of lackluster returns. Investors in Cisco, General Electric, Exxon, and Intel, by contrast, would have lost money. Extreme success is hard to replicate, and stocks priced for perfection rarely achieve it. We are not suggesting that investors blow out of their biggest winners and incur taxable gains. But we do like the look of an equal-weighted S&P 500 investment over the usual market-cap variety. Small-cap and value styles also look rather more appealing than they did six months ago as vaccine optimism gathers.

Goldman Sachs Equity Strategy

While we spend much of our time obsessing over credit and real estate, we will largely leave our thoughts on these fascinating sectors to a future dispatch. Suffice it to say that what goes for equities goes for credit and real estate as well. We favor moves toward cyclicality and risk, with scrupulous attention to business models potentially broken by COVID (for example high-priced downtown office space). In credit, the speed of mean reversion in defaults has been remarkable. After an August peak near 9%, the high yield annualized default rate has declined to 8.3% in October. We have favored loans over bonds due to generally better creditor protection, but we see the default rate for risky credit in general trending toward its long-term average of 4% by late next year. More fiscal support will only expedite the recovery.

Some landlords, particularly in retail, have taken the social distancing recession on the chin. But rent collections have improved from lows in the teens early in the pandemic, to 89% nationally in October. This level is only marginally below pre-pandemic averages. The laggards are, unsurprisingly, cinemas and fitness centers. Average collection rates may dip throughout the winter, but we see good prospects for recovery in this most affected asset class. Many private “opportunity” funds have been raised to capitalize on distress in credit and real estate assets, but private market transactions have been slower to materialize than the vultures hoped. Anecdotally, the lag in private equity deal flow is reminiscent of the GFC, despite record levels of “dry powder.” Like many, we have been surprised at the velocity of the bounce-back in the economy, which has been reflected in the valuations of many credit and real estate assets. With the Fed standing by to support markets in risk assets, with investors’ resolve firming, and with at least three vaccines on the horizon, these valuations are likely at least sustainable for the next leg of the cycle.

Brightening the Obscurity

A famous investor titled a supremely well-timed client note in March 2009 “Reinvesting when Terrified.” Today, The terror of the first weeks of COVID’s arrival on American shores has largely subsided. Those who held firm in their portfolios have generally been rewarded. Those who sold positions, perhaps prudently alarmed over a situation without precedent in modern economic history, still have an opportunity to re-enter markets at reasonable levels, provided some discretion is employed about which markets. The terror may be past but the suffering, the economic damage, the horrific loss of life, and the loss of innocence remain. Investors, like all citizens, will bear the scars of the 2020 pandemic for generations. Legacies of the lockdown may include a greater appreciation for the frailties of institutions like the CDC, or a “democratization” of stock ownership by a cohort reared on smartphones and video games. Meanwhile, politics have continued their slide into tribal nastiness, although more Americans participated in the electoral process in 2020 than ever before. Washington may be gridlocked but, for now, galvanized by street protests and social media debates, Americans are widely engaged in demanding change.

In spite of the optimistic tone of the forgoing paragraphs, we do expect more turbulence on the horizon. If the S&P 500 is indeed headed toward 4,000, it is unlikely to be a smooth ride. But as we always preach, a long-term plan sometimes requires some intestinal fortitude to “stay the course.” Current events inflame headlines and roil financial markets; getting invested and remaining invested in a judiciously chosen diversified portfolio of assets is still the surest way to grow wealth over time. Irreducible uncertainty is a fact of life, and as economists John Kay and Mervyn King argue in a recent book, is a key reason that financial assets change hands at all. But as the near-term public health scene approaches its grimmest hour, clarity about the future is ever-so-slightly enhanced. Now is a good moment for investors to begin to put in place the portfolios they wish to have in a post-pandemic world.