13 min read

Inflation: Will the Dog Bark This Time?

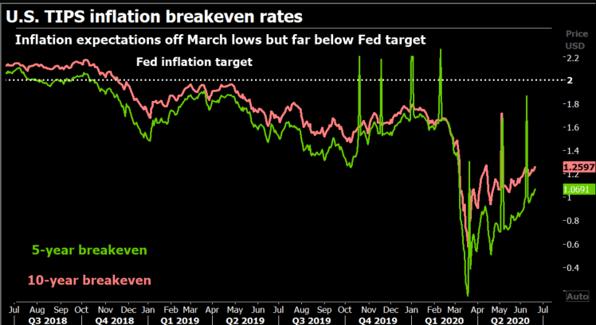

In 2013, the IMF pronounced inflation “the dog that didn’t bark”. After a pandemic and recession that threatens to reduce the GDP of advanced economies by more than 6%, it may seem curious to consider whether this time, the dog will really bark. Yet some investors look at the size and scope of governments’ to the COVID-19 crisis—$9 trillion in fiscal measures to date, and a Federal Reserve balance sheet that has ballooned by $3 trillion since March—and have begun to contemplate inflation’s long-awaited return. Gold prices are surging while the difference between inflation-protected government bonds and the conventional sort is rising again after falling dramatically in the first weeks of the crisis. Supply shortages, such as for meat, may be offering an early preview of more widespread shocks to come.

In 2013, the IMF pronounced inflation “the dog that didn’t bark”. After a pandemic and recession that threatens to reduce the GDP of advanced economies by more than 6%, it may seem curious to consider whether this time, the dog will really bark. Yet some investors look at the size and scope of governments’ to the COVID-19 crisis—$9 trillion in fiscal measures to date, and a Federal Reserve balance sheet that has ballooned by $3 trillion since March—and have begun to contemplate inflation’s long-awaited return. Gold prices are surging while the difference between inflation-protected government bonds and the conventional sort is rising again after falling dramatically in the first weeks of the crisis. Supply shortages, such as for meat, may be offering an early preview of more widespread shocks to come.

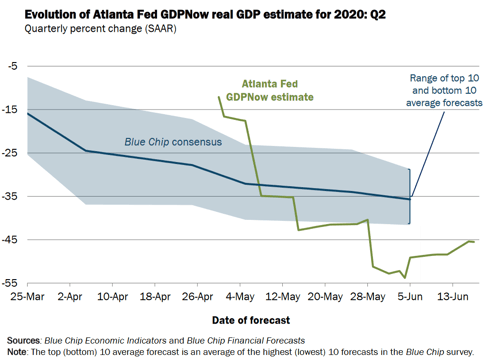

In the short run, the shut-in of economic activity has exerted severe disinflationary pressure on the American economy, as slack in output and employment reaches record levels. The Atlanta Fed projects an annualized quarterly decline in U.S. GDP of 45%. But pandemics and recessions eventually come to an end. In the medium run, as the economy absorbs years of potential deficit spending along with unprecedented injections of liquidity, the stage may be set for a rise in inflation.

Over the past two decades, there have been a number of structural factors that have conspired to keep inflation low, typically below the Fed’s 2% target. These include demographics (an aging population inclined to increase savings and rebuild balance sheets), technology (the falling cost of capital goods and the possibility of online shopping), and inequality (wealthier people have a high propensity to save). Financial influences, such as voracious global demand for safe government bonds, new bank regulations that have curtailed lending, and a lack of physical investment, have kept a lid on interest rates and on spending. In the aftermath of the 2008 financial crisis, a collapse of the shadow banking system and in the velocity of money circulation meant that warnings over the inflationary impact of unconventional monetary policies turned out to be false alarms. But the financial system today is healthy, and governments seem to have little appetite for the belt tightening they implemented in the wake of 2009’s budget-busting stimulus. Further, the age of unfettered free trade, globalized supply changes, and labor arbitrage that brought us low consumer prices and weak wage growth, appears to be nearing its end. This time, in short, may be different. *

In this note, we lay out a scenario in which above-average inflation returns to the fore. We evaluate the stages we would expect to go through before inflation becomes a first order worry for investors. We are already some of the way there, though the days of 1970s-style price controls appear quite far off indeed. Finally, we suggest some considerations for investment strategy in a decade with potentially higher inflation rates than the one just elapsed. The standby advice—buy gold, buy property, buy farmland, sell bonds—will not suffice. Investors need a balanced portfolio that will serve them well across a range of economic backdrops and must resist the urge to market-time swings in macroeconomic variables. But, as always, it helps to have a battle plan. Preparation is key.

The Stages of an Inflation Resurgence

Contrary to Milton Friedman’s dictum, inflation is not “always and everywhere a monetary phenomenon”. Yes, in equilibrium, an increase in the money supply without a corresponding increase in production will cause prices to rise. But rarely is the world so simple. Money velocity (the frequency with which a given dollar is spent, which is cratering) matters. Fiscal spending (and the commitment to back it with taxes) matters. Sudden supply shortages or gluts (such as the 1973 oil embargo, or the spike in oil inventories this March) matter. Most of all, expectations matter. Inflation works as a feedback loop. Producers of goods see higher input costs and expect these to continue, so they raise final goods prices. Consumers see prices rising, and bargain for higher wages. Employers see unit labor costs going up, so they raise prices still further. Ultimately this can set off a “wage-price spiral”.

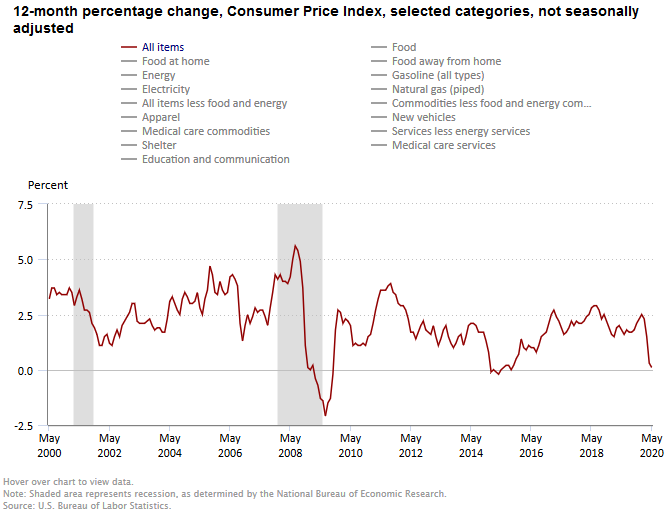

In recent decades, even as unemployment has fallen, expectations of future inflation have remained well anchored below the Federal Reserve’s 2% target. Only rarely since the crisis of 2008 have consumer prices risen by 3% annually. The observed relationship between unemployment and inflation known as the Phillips Curve appears to have broken down. Some have speculated that residual slack in the labor force due to part-time or gig work was holding down the bargaining power of workers. Others suggested that the monopsony power of increasingly concentrated employers was behind low wage inflation. Whatever the explanation, low inflation became a self-reinforcing expectations dynamic in the decade following the Great Financial Crisis. Even with massive government stimulus and an eightfold increase in the Fed’s balance sheet, turning such a process around will take time. Unless policy serves to undermine sticky expectations of low inflation, and all that central bank liquidity actually gets into the real economy—via increased lending by banks and higher money velocity—the dog will likely remain silent.

Below we outline eight steps we would expect to see before a significant, sustained pickup in the inflation trend. There is no guarantee that all of these stages will occur, though each individually is plausible. Based on historical experience, unless the economy goes through all or most of these phases, we would not expect inflation to rise materially over the period of the next several years. For those nervous about inflation’s return, however, these bear watching—we are already some way down the path.

- Step 1 – A deep recession causes a societal rethink over the limits of government policy. ☑

This is well underway. Even the notorious tightwads in Berlin are discussing binning their “black zero”—the legal debt brake and balanced-budget requirement. Eurobonds may be next. - Step 2 – Unprecedented fiscal and monetary support begins to erode the belief that governments will go on austere diets to pay back debt. ☑

For inflation to set in, it’s not enough to flood the economy with government demand. This largesse must also not “crowd out” private spending, and consumers must not believe stimulus will be withdrawn before the economy fully recovers. One way the government can make such a credible “promise to be irresponsible” is to incur debts so high they cannot plausibly be paid down without being monetized (inflated away) by the central bank. US debt has risen to over 100% of GDP, while the Fed has committed to do whatever it takes to keep rates low for years. - Step 3 – A rapid economic rebound ensues. ☑

Unless the economy begins to turn around, fiscal and monetary multipliers will be low, and private demand for borrowing and spending will stay low no matter what the government does. Fortunately, pandemic-enforced closures are the kinds of recessions that come with a natural end date, and federal relief measures so far appear to have bridged consumers and businesses through the initial difficult period. According to one estimate, nearly 70% of those who lost jobs are receiving more in temporary benefits than they did in work. An economic recovery (whether V- or U-shaped) seems on the cards for 2021. - Step 4 – Longer-run political shifts push fiscal policy back to the fore.

In the 1960s and 1970s, Keynesian planners believed more-or-less constant pump-priming could maintain aggregate demand growth for years, and effectively abolish the business cycle. The stagflation of the 1970s and the rhetorical victory of Milton Friedman’s monetarism eradicated that view. What took its place in the halls of Congress and the boardrooms of the Fed was a persistent fear of inflation and suspicion of wasteful and inefficient government spending. COVID-19 may be ushering in a generational shift in attitudes toward deficits. Deficit hawks seem to be an endangered species on both sides of the aisle. Talk of massive fiscal programs such as Green New Deals or $1 trillion infrastructure plans abounds. Again, expectations matter more than anything else. If the coronavirus relief packages show that a strong fiscal impulse can revive sputtering economies, even at the cost of some inflation, people may come to expect more. The austerity that followed Obama’s 2009 stimulus and was imitated across Europe may not be revisited in 2021. - Step 5 – Historically low productivity fails to improve and monetary support is not withdrawn.

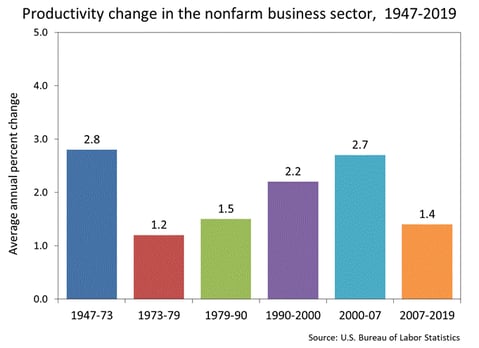

In recent years, the productivity of the U.S. economy (output per hours worked) has trended lower, well below its 2%+ trend for the most of postwar period. The causes of productivity growth are deeply mysterious, but most agree they have to do with capital spending, improved technology, and better skills in the labor force. When government investment boosts the productive capacity of the economy—for example, in highways, electric grids, or basic research—the supply side of the economy expands and deficits shrink. When fiscal firepower has low or negative returns—for example, during the Vietnam War—debt ratios grow, and inflation is the usual result. It is incumbent upon central bankers in these situations to tap the brakes, even if jobs growth is underwhelming. Increasingly politicized central banks may be reluctant to do so. Few doubt that the unprecedented scale of government relief during the current slump is warranted. But if the taps remain open once the health crisis recedes, will it be productivity or inflation that perks up?

In recent years, the productivity of the U.S. economy (output per hours worked) has trended lower, well below its 2%+ trend for the most of postwar period. The causes of productivity growth are deeply mysterious, but most agree they have to do with capital spending, improved technology, and better skills in the labor force. When government investment boosts the productive capacity of the economy—for example, in highways, electric grids, or basic research—the supply side of the economy expands and deficits shrink. When fiscal firepower has low or negative returns—for example, during the Vietnam War—debt ratios grow, and inflation is the usual result. It is incumbent upon central bankers in these situations to tap the brakes, even if jobs growth is underwhelming. Increasingly politicized central banks may be reluctant to do so. Few doubt that the unprecedented scale of government relief during the current slump is warranted. But if the taps remain open once the health crisis recedes, will it be productivity or inflation that perks up? - Step 6 – Secular forces that have weighed on inflation begin to reverse.

The developed countries and China are aging. Their populations are saving more and spending less. This demographic wave seems impossible to reverse. Other factors, such as technology, trade, monopoly, and inequality may have reached their limits. A full survey of the geostrategic landscape is beyond the scope of this note, but suffice it to remark that each of these disinflationary influences may ebb in a post-COVID-19 world. Trade spats between the U.S. and China along and the disruption of global supply chains could reverse decades of globalization. As offshoring becomes nearshoring, wage pressures should rise. The imminent demise of Moore’s Law may arrest the downward trend in the cost of computing power, while a breakup of consumer internet platforms (increasingly popular with both political parties) could reduce price wars for consumer products. A revival of trustbusting could, as noted above, give workers the upper hand in wage negotiations. And if politicos begin to get serious about tackling inequality, a rise in real wages or incomes for the bottom 50%, with their higher marginal propensity to consume, should in turn raise prices. - Step 7 – Inflation expectations begin to shift.

For years forecasters at the Fed and in markets consistently overestimated future inflation. Eventually, however, most forecasts catch up to reality. Many of the shifts outlined above are tectonic; they will not appear out of the blue. But if the positive surprises begin to add up, expectations for inflation will follow. As we have said, inflation ultimately depends on beliefs about inflation. It can be a self-fulfilling prophecy. The stories analysts and policymakers tell about inflation trickle into popular beliefs, and popular beliefs trickle into prices. As beliefs begin to shift, there will be upward pressure on wages, on prices, and on government borrowing costs. Such a sea-change may not initially lead to very high outright levels of inflation, but it will make the economy vulnerable to a shock. - Step 8 – A new supply shock emerges. Will it be caused by energy, war, drought, or something else?

The nature of a “shock” is that it is difficult to predict in advance. Public health experts warned for years that our globalized economy was vulnerable to a pandemic. Understanding that the risks of an event are heightened does not mean that we can pinpoint its precise time, place, and character. But we can be sure that, given enough time, “stuff” happens. Rising deficits and national debts, increases in the money supply, secular shifts in the dynamics of trade or labor relations, a higher center of gravity for expectations—these all would push inflation above its recent trend and above central bankers’ targets. But it would likely be a shock—an unexpected disruption of vital inputs such as food or fuel, or possibly a hot war or tariff war that destroys critical supply chains—which would lead to the kind of rapid inflation investors worry about. Luckily, we are likely several years away from such a scenario today. But if we ignore the warning signs, we may get there before we know it.

How to Invest for the Return of Inflation

Inflation is one of the greatest risks facing investors. Investors on fixed incomes are particularly vulnerable to a bout of unexpected increases in the price level. Therefore, it pays to keep inflation hedges—precious metals, real estate, or TIPS—at the ready at all times. Simultaneously, when we make long-term investments in fixed income securities, we want to ensure that we are compensated for assuming inflation risk. The “term premium”, or the difference in yield between long-maturity bonds and shorter ones, is an important variable to watch. Currently, it is quite low, suggesting investors are paid very little for taking on the risk of unexpected inflation.

Our counsel now is somewhat subtle. We do not believe inflation is imminent, despite scary stories about massive increases in fiscal spending or monetary aggregates. We do believe, however, that risks now point to the upside, and the policy environment should be considered very carefully as we move forward. As economies exit the pandemic recession, investors will be rewarded for riding a cyclical rebound: industrial, basic materials, financial, and consumer discretionary stocks will perform well. Private investments that take advantage of early cycle opportunities, such as distressed credit, may see a renaissance. But as the period from 2009 to 2013 showed us, investors should be mindful of the long tail of bankruptcies and distress, which, depending on politics, may play out in sovereign as well as corporate credit. The crisis demonstrated that a number of business models and financing strategies are dangerously fragile. Investors should play for recovery but beware stretched valuations and businesses that are binary risks.

In the intermediate term, one can position his or her portfolio for a return of inflation without paying dearly for the privilege. Historic inflation “hedges” such as real estate are relatively affordable now. Investing in infrastructure is one way to anticipate policy shifts discussed above. Metals and energy stocks are cheap as well, although these sectors have been minefields of late. Broadly, we advise to avoid long duration assets without substantial inflation compensation. These could be low yielding 30-year bonds, triple net leases, or royalty streams. Long-term cash flow is terrific, but low coupons in an era of rising inflation are deadly. We also focus relentlessly on pricing power. We prefer to invest in businesses or assets with a durable competitive advantage. That means prime real estate, quality brands, and technological barriers to entry. Pricing power is evident in margins that remain elevated for years. A business which can pass along cost increases is incredibly valuable in a period of rising prices. If they trade at slightly higher multiples than the market in today’s disinflationary environment, we might think of that premium as a form of inflation insurance.

Lastly, our advice is to remain patient and wait. We would neither recommend selling all our bonds nor putting a quarter of our portfolio into gold. The inflation scenario we laid out above is, more than anything, a multi-year process. Each step is contingent. There remain serious disinflationary forces at work in the world economy and they cannot be repealed in a month or even a year. Today, as inflation hedges are fairly cheap, it makes sense to begin to reorient portfolios for a possible future of above-trend price increases. A comeback of inflation would not surprise us as we move past the pandemic and its immediate aftermath. It is best to prepare today.

Related Posts

The Dog that Caught the Car

Last year we visited the topic of inflation, and wondered if, after a decade of false alarms, the...

Time to Buy?

No. Decades of low inflation and falling real yields pushed up valuation multiples across all...

Happy Holidays, from WMS (and the Market)

“When a consensus of policymakers, commentators and investors is arrayed so overwhelmingly behind...