11 min read

No. Decades of low inflation and falling real yields pushed up valuation multiples across all assets and created an “everything bubble.” The return of sticky inflation is causing an “everything slump,” which is still underway.

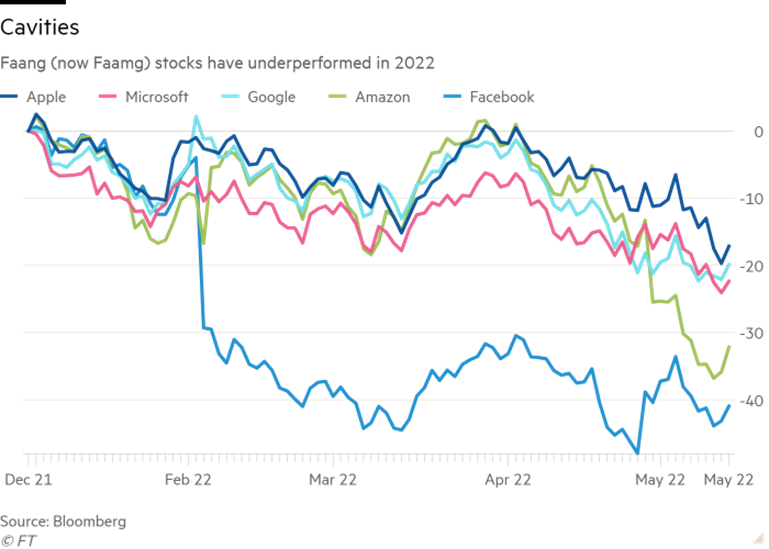

At the time of this writing, the S&P 500 and the NASDAQ are down year-to-date over 17% and 26%, respectively. Almost one in five NASDAQ Composite stocks has lost half its value in the past year. Numerous S&P 500 stocks are more than 70% off their highs. The so-called FAANG stocks which began the year worth nearly a quarter of the index’s total capitalization are all down more than 20%. Netflix has crashed so badly as to be disinvited to the party (de-FAANGed?). So, is it time to buy the dip?

https://www.ft.com/content/ac1200cd-75f7-4ea8-89ee-8125e0e9e67d

According to an adage, when markets are fearful, it is the time to be greedy. Historically, there have certainly been moments of cresting fear, such as March 2008 and March 2020, when such a strategy would have paid off handsomely. But, just as we have cautioned clients against rushing headlong into cash as market turmoil intensified this year, we believe it is too soon to add to risk in equities now.

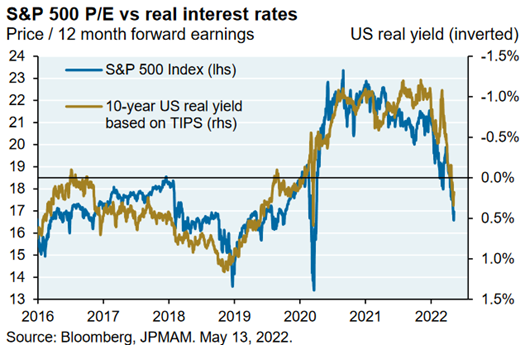

The reasons are severalfold. The first is valuations. While price-to-earnings (P/E) multiples have fallen steeply this year, in the case of large cap (S&P 500) stocks, they are only approaching their historical averages. Currently the S&P 500 forward P/E ratio stands at around 17 times—neither egregiously expensive nor inexpensive compared to the two-decade average of about 16 times. And P/E multiples rarely ever reside at their average; they tend to overcorrect to the upside and to the downside.

Moreover, this multiple doesn’t factor in a wave of negative earnings revisions that appears to be just getting started. Current consensus estimates for S&P 500 earnings stand around $230, roughly a 10% jump from last year. In an economy with rising interest rates, rising cost pressures and cooling demand, such growth expectations look like a tall hurdle for stocks. So, stock returns could be under pressure from either the numerator or the denominator of the P/E ratio.

There are more attractive valuations in other parts of the stock market, and we continue to recommend a rotation from growth to value, from large-cap to small, and (cautiously) from the U.S. to international markets. Profitable small-cap stocks (S&P 600) can be had for only 12.2 times forward earnings, and despite the recent re-rating of mega-cap blue chips, the large vs. small performance gap is still historically large over most time-scales. European equities trade at 12.5 times forward earnings, while emerging markets look an even more intriguing bargain at 11.4 times. While we prefer these pockets of (relative) value, we expect that these areas of the market will be more sensitive to macroeconomic and geopolitical headwinds that show little sign of abating. They can certainly get cheaper in the near-term.

Over long periods of time, stocks’ P/E multiples tend to follow real (after-inflation) risk-free yields. More than two decades of falling inflation—caused by a host of global factors, some of which have begun to reverse—provoked a steadily falling inflation risk premia and ever-lower real yields. The natural result was rising asset prices. This process culminated with "QE infinity" in the United States following the COVID lockdowns and real yields dropping dramatically below zero. In 2021, P/E multiples, on a cyclically-adjusted basis, reached near record highs above 35. This “everything bubble,” as it has been called, also led to a massive outperformance of high-growth stocks over slower-growing value stocks. Unwinding this trade will take years, and perhaps decades. So far, 2022 looks like the beginning of of an “everything slump.” Risk parity strategies and 60-40 stock-bond allocations are of no help in a stagflationary unwind. Even as shockingly high inflation prints recede, we still expect durably higher inflation readings than investors and policymakers had become accustomed to. This will lead to higher base levels of real interest rates and will refocus investors’ attention on dividend yields, valuation, and real returns.

As an minor digression, while we buy the "everything bubble" characterization, this argument does not necessarily recommend a particular trading strategy. Inflation was surprising to the downside, with stocks and bonds rallying together, as early as 2014, if not 2009. Had we sat out this bubble for a decade, we'd be much less well off than we are today. As of 2020 it was apparent that some kind of paradigm shift was brewing but even then it took six months for inflation to materialize and another year for the Fed to being to act aggressively. Timing the bursting of a bubble (or even identifying one ex ante) is notoriously difficult. The best we can say is that structural macroeconomic environment must inform our strategic asset allocation, but the portfolio that tends to win over time is one that focuses on compounding a growing stream of cash flows, and treats shorter-term fluctuations as background considerations. Rather than attempting to predict when interest rates will peak or what inflation will average in 2023, we believe investors are better off surveying the broad economic landscape—higher real rates, commodity price pressures, energy transition, the rebuilding of supply chains, etc.—and constructing portfolios resilient to this backdrop. To us, this means increasing the emphasis in portfolios on cash flows, intrinsic or liquidation value, and real asset diversification.

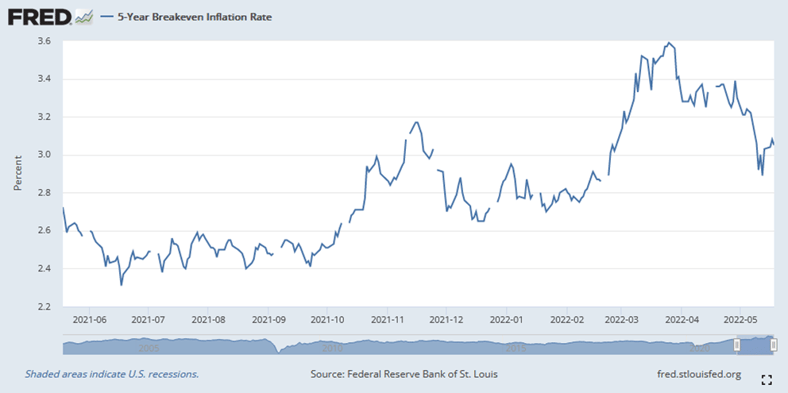

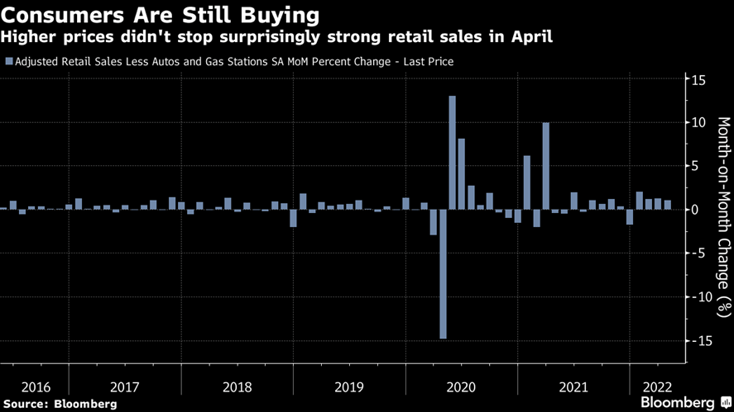

A second reason for restraint at this time is a shift in the market’s concerns from inflation to growth. 5-year market-based inflation expectations have actually been coming down swiftly as the bond market begins to price in an increased likelihood of a recession and the Federal Reserve being forced to back down from its current hawkish stance. Lower inflation would be a good thing for the economy, but when it comes from either demand destruction due to high prices of energy, food, and goods, or merely a normalization of demand patterns as consumers exhaust built-up savings, this is emphatically not a good thing for stocks. Despite epochally poor readings for consumer sentiment, retail sales have thus far held up surprisingly well. There is plenty of room for demand to fall. Corporate profit margins actually grew in 2021’s accelerating inflation environment, rising from an already healthy 9% to over 13%. Consumers hamstrung by higher gas prices and less excess savings may now be less willing to countenance continued price hikes.

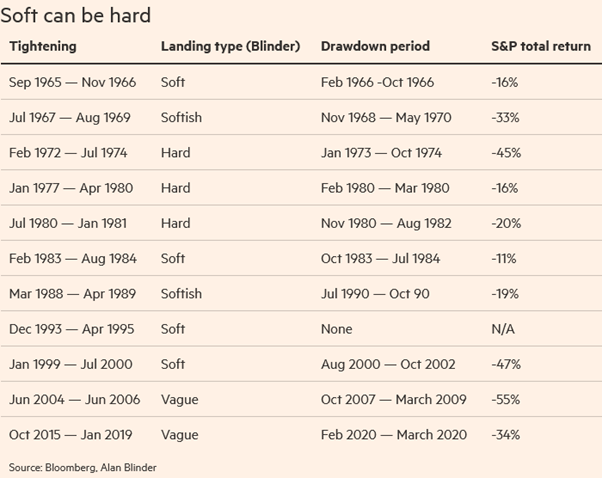

It is often said that stock markets are discounting mechanisms, and most estimates have market expectations for a recession around 30-35%. Normally, markets don’t bottom until expectations are much more dire—on the order of a 50% probability of a recession. Furthermore, it doesn’t require an actual recession for a steep bear market decline. As Robert Armstrong in the Financial Times has pointed out, even a “soft” or “softish” landing (i.e. a short and mild recession) is typically associated with stock market losses of 20% or more. That is, what markets have done so far in 2022 may be to discount the best-case scenario.

It is often said that stock markets are discounting mechanisms, and most estimates have market expectations for a recession around 30-35%. Normally, markets don’t bottom until expectations are much more dire—on the order of a 50% probability of a recession. Furthermore, it doesn’t require an actual recession for a steep bear market decline. As Robert Armstrong in the Financial Times has pointed out, even a “soft” or “softish” landing (i.e. a short and mild recession) is typically associated with stock market losses of 20% or more. That is, what markets have done so far in 2022 may be to discount the best-case scenario.

https://www.ft.com/content/88a1facd-bb37-4bbe-b8d6-f06a418186c3

https://www.ft.com/content/88a1facd-bb37-4bbe-b8d6-f06a418186c3

What’s more, these previous stock declines are not generally coming off eye-wateringly high valuations such as we saw in the middle of 2021. Many economic and inflation forecasters have debated which historical period the current cycle resembles most: first, the 1947-1950 inflation episode that was driven by pent-up demand and shortages from war demobilization and which also subsided quickly; second, the late 1970s-early 1980s drama when energy price shocks ignited wage-price spirals across the rich world; or finally, the late 1990s where euphoric valuations finally surrendered to a popping of the technology bubble, bankruptcies, layoffs, and a brief, shallow recession. Our view on this question is that today’s markets remind us of all three. Finding the right historical analogy can help us interpret market moves, but only by establishing precedent for what could happen. Notably, above, we can see that the “soft landing” after the 2000 tech bubble burst resulted in a 47% drawdown in the S&P 500, an index whose concentration in fast-growing technology names is even higher today.

The final reason to remain conservatively positioned, in our view, is that few of the economic headwinds we wrote about earlier this year appear likely to give way soon. In order for the Fed to back off its hawkish posture, it would need to see some organic respite in inflation. There are reasons to be optimistic; economist and blogger Noah Smith writes persuasively that most of the excess inflation in the U.S. was demand-driven and with early signs of this consumer demand potentially cooling, a soft landing is looking increasingly achievable. But food & energy inflation and their feedback into the critical driver of expectations are all highly sensitive to macroeconomic and geopolitical developments largely outside of U.S.-based policymakers’ control. The Chinese zero-COVID policy that has (re)entangled supply chains seems unlikely to be walked back as soon as was previously hoped. Meanwhile, though we will refrain from speculating about Vladimir Putin’s war aims, Russia may be backed into a strategy of entrenchment and escalation in Ukraine, keeping much of the world’s breadbasket and critical energy/petrochemical supply offline for a long time. This will maintain upward pressure on prices paid by consumers. Several core components are looking stickier, with some observing wage-price spirals in low-income service jobs, and lagging housing/rent inflation so far resisting sharp increases in mortgage rates. There are reasons to believe that semi-permanent shifts in the patterns of office work during COVID explain a good deal of the rise in housing costs. With rising costs and a decade of underbuilding, there is no obvious short-term remedy for this important driver, the largest weight in the CPI basket.

To be clear, we do think inflation will come down naturally from its heights. The Fed has tools such as balance sheet reduction that may help chill financial conditions without it being forced to hike aggressively, say to 5% as notable pundits such as former Fed presidents Richard Fisher and Bill Dudley and economists Kenneth Rogoff and Mohamed El-Erian have predicted. But that possibility—and worse—cannot be discounted at present. So, while today’s short-term bond yields arguably price the full brunt of a more forceful Fed, long-term bonds (10-year treasury yields have declined from 3.12% to 2.84%) and equities do not. Higher interest rates are designed to tighten financial conditions and choke off some economic activity. To the extent that economy was already contracting in the first quarter, or that in order to bring inflation under control rates may have to rise above current estimates of neutral (around 3 to 3.5%), this leaves a very narrow window for the Fed—and risk assets—to escape further damage. Our base case scenario remains that the economy avoids a severe recession, and that medium-term stock returns from here should be modestly positive. After all, the U.S. economy entered 2022 in a very healthy place, and the S&P 500 is at the same level it was in March 2021. But the balance of risks does not allow us to adopt (as we did throughout 2020) a very constructive view on stocks—yet.

We insert the qualifier “yet” very deliberately. There is some level at which stocks are clearly cheap that would give us reason to move into the “greedy” camp. The Wall Street Journal recently published a column warning of a “lost decade” for equities. That seems overly bearish to us. Patient equity investors should expect okay returns with a great deal of volatility, leading us to prefer less correlated (often cash-flowing) strategies in private markets. Yet current sentiment is terrible, which tends to indicate a potential bounce. Regardless of Putin’s motives, Russia’s forces will eventually either culminate or win in the Donbas theatre. China’s COVID surge will die down, or the CCP will relent after its party Congress this year. Base effects, new sources of supply, or high rates and softening demand will lead to lower inflation rates. Valuations will bottom, likely this year. Investors who remain in the accumulation phase of life, who have many more years of buying stocks ahead of them will be grateful for better opportunities ahead.

The current environment continues to reinforce the need for true, robust diversification in portfolios. Our tactical recommendations are the following.

- Remain short duration in fixed income; short-term bonds represent a more appealing alternative to either long duration bonds or cash.

- Continue to overweight real assets such as essential real estate and energy, preferably accessed through value-add private market strategies.

- Favor value stocks—particularly those with high, stable, and growing dividend yields—over speculative growth. There will come a time to rotate back into select high growth assets, but we counsel patience.

- Profitable, high quality small-cap stocks look increasingly attractive, if investors can stomach near-term volatility.

- Senior-secured, private direct lending is a great alternative to corporate bonds.