4 min read

- The investing environment is now best characterized as complex and uncertain. We have exited one market regime and are entering a new one that should be unlike anything we have seen for decades. There will be money to be made, but it will require two things: patience and cash flow.

- Strong and predictable cash flow has been one of the pillars of our investment philosophy at WMS Partners since our inception. While we are fans of cash flowing strategies in any environment, now is an excellent time to shorten duration in both equity and fixed income investments, focusing on cash flows that are front-end loaded.

- We favor private market strategies that provide consistent cash flow that resets with higher rates. In public markets, we look for high-quality, financially strong equities with a commitment to growing shareholders’ dividends, and short duration fixed income, where the downside is cushioned after a severe repricing of the bond market.

The events over the past several years have been extraordinary, making it especially challenging to draw parallels from past economic experience or market episodes. The unprecedented policy response to the pandemic triggered massive liquidity accompanied by rampant and broad-based price increases of most asset classes. Fed policy lagged acceleration in economic conditions and even realized inflation by an interval not witnessed in modern history. The downside of this supercharged recovery is an incipient expectations-driven inflation cycle and a policy footing that is appearing more forcefully divorced from economic reality. To cite a single example, there are 11 million jobs posted for an unemployed population of only 6 million, with private sector wages correspondingly rising 5.6% year-over-year. An economy that has run too hot, and a Fed that is frantically playing catch-up creates tremendous crosswinds for investors.

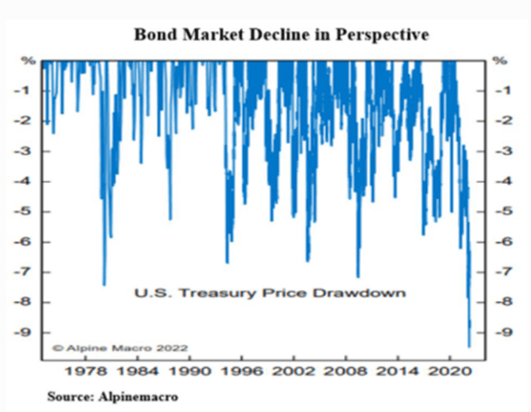

To add to the complexity of the current moment, we are also seeing a major sea-change in a long-term trend. The dominant investment influence during the past 40 years: ever-lower bond yield peaks and troughs.

Twenty years of disinflation and another 20 years of no inflation lulled investors and policymakers into the belief that bond yields would never sustainably rise. With a lid on discount rates, all asset classes flourished. For more than a decade since the financial crisis of 2007-2008, we have enjoyed low to moderate economic growth, alongside low inflation and interest rates. Well, that is no more. A new paradigm is still taking shape but it will undoubtedly be marked by higher inflation and rates than we enjoyed from 2008 to 2020. As the Fed pivoted in December, the first shoe to drop was in the investment grade bond market.

For the Bloomberg Aggregate Bond Index the first quarter of this year was the worst since 1980. And for U.S. Treasury bonds, it was the worst three months since at least 1926, when comparable data began to be available. Volatility in the equity markets makes headlines, but it’s the double-digit drawdowns in an area viewed by most as a safe haven that demands attentions.

Some of this volatility is unsurprising given the strong performance that preceded it for so long and the current worries about the war in Ukraine, new Covid-19 outbreaks, cities locked down in China, and soaring energy costs. One positive to the abrupt increase in rates is the opportunity to invest in short-term duration fixed income at much more attractive yields. These portfolios may have priced the majority of anticipated Fed hikes, and have the potential to somewhat cushion volatility going forward.

A sharp rerating of equity multiples on the back of a higher yield curve and heightened intermediate-term recession risk is testing the long-held market view that there is no alternative to U.S. stocks—often abbreviated with the acronym “TINA.” This supposed lack of alternatives was an oft-overhead mantra during the equity bull market of the last decade. If investors can be patient and hold larger amounts of money in short duration vehicles and cash equivalents, with steadily rising yields, the salience of the TINA argument is diminished.

Within the stock market, shorter duration stocks should provide some protection against rising yields. The duration of any investment is defined as the average time until its cash flows are received, weighted by their present values. In today’s environment, we see growing appeal of less levered companies who are committed to return cash to their shareholders sooner. These stocks are obviously in contrast to the many of the last cycle’s leaders—high-growth companies for whom a far greater proportion of total cash flows were expected in the distant. Today, our long-stated preference for high free-cash-yielding stocks with steady (though not eye-watering) growth appears especially appropriate.

At WMS Partners we have long focused on allocating to private markets. These strategies often provide non-correlated drivers of return, and therefore offer the potential for true diversification. Private credit strategies entail lending at floating rates, and therefore ought to be resilient in a rising rate environment. In value-added private real estate and private equity strategies, we expect returns to be driven by cashflow growth rather than by multiple expansion. Near-term cash distributions reduce the duration of investments and thus the NAV-risk of adverse market events.

Patience is a virtue, but it is one of the most difficult investment skills to master—particularly when overseeing our own money and dealing with the emotions this brings. An overemphasis on short-term results may impede progress toward long-term investing objectives. In today’s choppy market, there is an even greater premium on fortitude. Though we haven’t seen today’s inflation rates since the early 1980s, we have seen numerous cycles, and the bull and bear markets they bring.

We should all draw a deep breath, remembering that we knew this day would come—indeed we had planned our portfolios for it—and also knowing that it will pass. Knowing precisely when the volatility will ebb is unfortunately impossible. In the meantime, until there are very clear signals that the cycle of higher inflation, higher rates, and asset price volatility is receding into the rearview, we stress the value of shortening portfolio duration and staying true to long-term asset allocation targets.

Please See Our Important Disclosures

Related Posts

WMS Expands Advisory Team with Recent Hires Nate Allen and David Unger

In June, Nate Allen joined WMS as a Senior Client Advisor serving wealthy families, family offices,...

What’s Really Happening in China?

Evergrande: Not a “Lehman moment,” but it may be the first domino to fall in a larger, multiyear...

2023 Thoughts: Euphoria in Reverse

Cash is once again king