12 min read

Disclaimer: In this paper readers will find neither bitcoin price targets nor buy/sell recommendations. The paper was written in early January 2021 and it is likely that the price of bitcoin will have fluctuated dramatically by the time you read it. WMS Partners is unable to make investment recommendations concerning cryptocurrencies and cannot effectuate any transaction due to issues with custody of such assets.

“We view investing in bitcoin as a highly speculative bet on an emergent technology… which may nevertheless find much greater use in a range of new fintech applications as its network expands.”

“We view investing in bitcoin as a highly speculative bet on an emergent technology… which may nevertheless find much greater use in a range of new fintech applications as its network expands.”

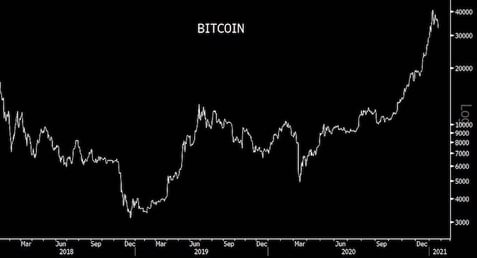

Avoiding discussion of politics and religion at the dinner table is generally wise, but this past Christmas you might have done well to abstain from mentioning bitcoin, too. The fervent religiosity of the digital currency’s fanbase has never dimmed, but a recent uptick in institutional interest has reignited the debate over its staying power. Bitcoin’s price has quadrupled over the past six months, minting many more crypto millionaires and intensifying “fear of missing out” (FOMO). Bitcoin believers will credit its recent parabolic price chart to legions of new “smart money” investors and an influx of dollar bears, while doubters may cite artificial price inflation caused by “painting the tape” schemes and stablecoin manipulation. A host of prominent bitcoin enthusiasts believe it will one day replace gold, while Warren Buffett and Charlie Munger, never fans of the yellow metal, have likened it to rat poison.

The bitcoin debate is polarizing, but with a nearly trillion-dollar “market cap” and a sharp increase in mainstream interest, its suitability as a financial investment should be thoughtfully considered by those building portfolios for the long term. With annualized volatility in excess of 100%, bitcoin and related technologies are, in our opinion, neither efficient mediums of exchange nor reliable stores of value as proponents claim. Bitcoin also has regulatory and scaling issues that gold, as the most widely held base metal, lacks. But neither of these facts mean that cryptocurrencies are uninvestable. Much of the debate has thus far been centered, we believe wrongly, on bitcoin’s “intrinsic value”. Many popular investments—art, antique furniture, classic cars—have little or no intrinsic value, whether defined as a positive cash yield, an ultimate use value, or a net present value of future cash flows. Yet they remain appropriate investments for some who possess the requisite knowledge, skill, and the stomach for illiquidity. Just because an investment cannot be “valued” does not mean it cannot be “priced.”

Bitcoin – Not (yet) a currency, not a safe haven, but a bet on technology

We view investing in bitcoin as a highly speculative bet on an emergent technology that has very little current utility, tremendous potential regulatory overhang, questionable liquidity and transparency, but which may nevertheless find much greater use in a range of new fintech applications as its network expands. As a protocol akin to the TCP/IP standard that underlies the World Wide Web, Bitcoin is also subject to tremendous network effects; the more people use it, the more valuable it becomes. Other technology platforms have clearly demonstrated how network effects beget winner-take-all economics, and bitcoin looks likely to be a winner.

Rather than launching into a philosophical argument about cryptocurrencies’ ultimate place in the financial and monetary system, we believe curious investors should begin by considering what bitcoin does, how it does it, and only then decide how it may fit in a portfolio. Ex-Facebook software engineer turned billionaire investor Chamath Palihapitiya claimed it took him 18 months to understand bitcoin’s underlying technology. A basic familiarity with the protocol’s framework, at minimum, would serve both devotees and skeptics well. Before all else, a bitcoin is a digital file that serves as a token of exchangeable value, and Bitcoin Core is the software that facilitates its transactions and governs the network. Bitcoin Core is an open source protocol, meaning anyone can improve upon it if their proposal meets certain technical criteria and is accepted by the community of users. Decentralization is the system’s foundational characteristic and is achieved through a complex balance of powers of three network parties – developers, nodes and miners. Developers propose iterative improvements to the software, nodes are small servers that manage network data and enforce the protocol, and miners process transactions by solving complex encryption algorithms.

The mainstay of Bitcoin Core is the blockchain, which serves as a complete and transparent record of all bitcoin transactions since its inception. It is in essence a transaction ledger that utilizes cryptology to link present and historical transactions. Every ten minutes, on average, a limited number of bitcoin transactions are consolidated into a block and added to the end of a blockchain. Once a block is added, its component transactions are irreversible. Those due to mistakes or fraud are not exempt. Transaction information and a copy of the ledger are maintained by nodes that run Bitcoin Core software and communicate with their peers to transmit transaction data, audit the blockchain and approve newly mined blocks. The distributed nature of this system of nodes is crucial—it requires a relatively low amount of computing power to run a node, allowing individuals to support the integrity of the decentralized network.

Bitcoin miners add transactions to the blockchain and mint new bitcoins. Each miner will run nodes to authenticate new transactions and aggregate them into “mempools,” a holding area for pending transactions. From this collection, miners will typically assess each transaction fee and select the most profitable transactions for inclusion in a new block. Each miner races to be first to mine their newly created block by solving a cryptographic “hash function”, essentially a trial-and-error math problem that requires tremendous computational brute force to output a single arbitrary number from a truly massive possibility set. This effort requires a substantial amount of computing power and thus electricity. If the Bitcoin network were a country, it would rank in the top 40 by electricity consumption, according to estimates by the Cambridge Center for Alternative Finance. When the algorithm is solved, the new block is added to the blockchain, and the race for the next block begins. The winning miner is rewarded with a fixed amount of newly minted bitcoins (the “subsidy”) and a collection of the block’s transaction fees.

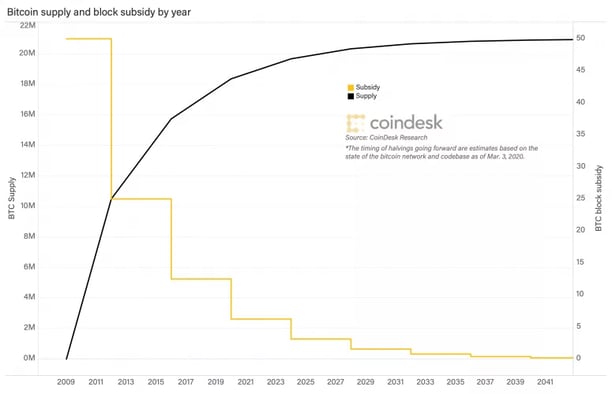

One last technical detail—which is the most widely discussed—is bitcoin’s scarcity. About every four years, the rate at which new bitcoins are minted is halved, and the supply will be fully exhausted at 21 million coins. Today, there are over 18.5 million bitcoins in circulation, and the last bitcoin is expected to be minted in 2140. The significance of this date is often over-emphasized and can be quite misleading; equally important is the declining rate of growth, and the reduction of the current subsidy of 6.25 bitcoins per block to about 0.2 bitcoins two decades from now. Critically, unlike sovereign currency or even gold, both bitcoin’s ultimate supply and the pace of its mining are arbitrarily limited. Other crypto assets, however, have emerged to effectively increase supply as demand soars.

Source: https://www.coindesk.com/bitcoin-halving-explainer

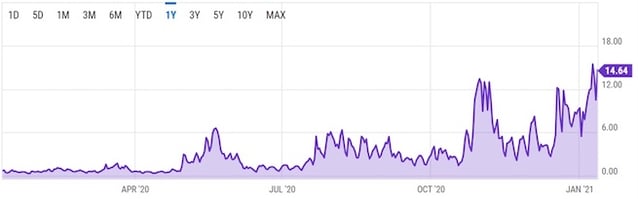

Originally, the techno-utopian vision for bitcoin was as a cheap, anonymous payment network that would be independent from central banks—hence its initial popularity among anti-government libertarians, cybercriminals, and drugs traffickers. Beyond a few unfortunate pizza purchases and crypto-friendly e-commerce sites, bitcoin’s use as a medium of exchange has been hindered by scaling problems as built-in velocity restraints and transaction fees begin to bite. The rate at which bitcoin transactions are processed is largely determined by the number of transactions that can fit in each block and the difficulty of the hash function. The current protocol sets a low ceiling on bitcoin’s velocity, with a theoretical processing limit of seven transactions per second. For reference, Visa processes 1,700 transactions per second with a theoretical limit of 24,000. As a consequence, as the number of bitcoin transactions grows, fees are driven up with multiple users competing to have their transactions processed simultaneously. These constraints are by design as they maintain the security of the network. Slow transaction velocity checks growth in the amount of computing power required for individuals to run a node, allowing the network to remain decentralized. Transaction fees also experience upward pressure as the bitcoin subsidy decreases over time. As the subsidy approaches zero, the decrease in miners’ compensation must be offset by rising transaction fees and/or an increase in bitcoin’s price.

Bitcoin average transaction fee (Source: Ycharts.com)

Bitcoin average transaction fee (Source: Ycharts.com)

So bitcoin, which was conceived as a decentralized currency independent of political manipulation, is both too slow and too costly to reliably serve most of a currency’s important functions, except perhaps in some places where rule of law, trust, and governmental institutions are weak. A borderless currency that appreciates so rapidly as to encourage hording, whose transactions are irreversible, and whose “wallets” and “exchanges” are vulnerable to theft and hacking hardly meets its anonymous founder’s dreams of “an electronic payment system based on cryptographic proof instead of trust.” Forgetting that trust—far from being a bug to be eliminated—may be the cornerstone of all economic exchange, bitcoin and the blockchain concept on which it is based is simply a clunkier mechanism than trusted third party systems. What gives? What accounts for bitcoin’s remarkable rise from fringe science experiment to mainstream investment alternative?

It turns out that what makes a poor currency—scarcity, illiquidity, volatility, reluctance of its most dedicated adherents to part with it—makes an excellent speculative asset. For skilled traders such as Paul Tudor Jones and Stanley Druckenmiller, volatility itself is part of the appeal. As bitcoin’s utility as a medium of exchange has faced increased headwinds, the narrative that bitcoin is superior to gold as an inflation-hedged store of value has gained popularity. Indeed, both assets share certain qualities—gold is physically scarce while bitcoin is deliberately scarce, both appear to be effective portfolio hedges against liabilities denominated in G7 currencies, and the public’s acceptance of bitcoin as a store of value is growing. What makes any token appealing as a store of value is others’ belief that it is a such a store. Gold is no different, and bitcoin is advancing quickly in this respect.

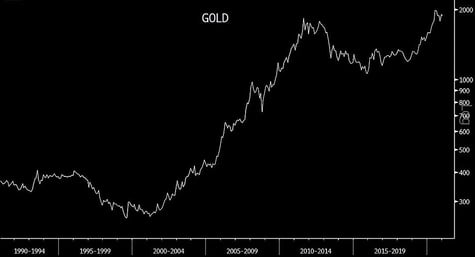

But bitcoin and gold have some important differences, including storage costs, energy consumption, security and industrial utility. For bitcoin to adequately serve as a store of value, its vertiginous price drawdowns will need to dampen as it matures. Over the past three years, bitcoin has experienced three 1-month drawdowns exceeding 40%, fueled in part by its lack of liquidity. Gold, the majority of which is held in reserve by central banks, has not experienced a decline as sharp as this this in the past 30 years.

Source: Bloomberg

The “e-gold” analogy may be one of convenience as bitcoin struggles to establish its identity. But as crypto is embraced by Wall Street, the two assets’ investor bases increasingly overlap. Bitcoin’s elevated volatility will persist as its underlying technology is still in its infancy and its price movements remain largely tied to momentum and sentiment. Bitcoin is likely to see new arguments for its inevitability as a world currency, for its use as a diversifier of portfolios, and for its status as a haven from inflation in other fiat currencies. In one way, however, a bitcoin is fundamentally different from a gold bar: innovation.

In our view, bitcoin attracts justifiable interest as a potential long-term investment because it is an intriguing technology with overwhelming first-mover advantage. Not only is the Core developer community working continually to improve the network, but third-party technology companies are building platforms to solve current challenges and expand bitcoin’s use cases. For example, the Lightning Network is a second layer technology seeking to improve bitcoin’s scalability. Blockchain technology still has few current practical applications but it may have the potential to be useful in cross-border transaction settlement, supply chain management, or corporate record-keeping. Surely, the kinks will need to be worked out. But, unlike private payments systems, the public blockchain (of which bitcoin is the most prominent application) is open to iterative enhancement by its expanding community of developers. Bitcoin, by far the most accepted and widely used cryptocurrency, is thus positioned to benefit from protocol improvements and innovations to the blockchain. The competing goals of security, decentralization, and efficiency are inherent tradeoffs, but not necessarily insoluble ones.

One additional consideration for bitcoin investors is a mechanism known as a hard fork. When a change is made to the Bitcoin protocol that affects a critical operating parameter, it can lead to a divide among the node and mining community. A large enough dispute could, in effect, create an entirely new cryptocurrency. In past events, bitcoin owners have received a copy of the newly created currency in addition to their bitcoin, and they retain ownership until one is transacted. Multiple previous hard forks have generated contention among crypto fans, with some even labeling the debates a “civil war.” In our view, such splits are signs of progress and durability. They serve as proof that bitcoin may evolve in different directions without fundamentally fracturing its core ideas. For patient investors, hard forks can be seen as an option on technological progress.

How to gain investment exposure today, and what lies ahead?

In general, central governments have taken a wait-and-see stance on cryptocurrency. Regulation is often cited as an existential risk to crypto assets, but this too might be taken as a positive step in their development. Reducing fraud and piracy while increasing the transparency of the market structures that govern supply and demand will likely lead to broader institutional adoption. With PayPal and Fidelity and even the insurer Mass Mutual entering the arena, it appears bitcoin investing is progressing out of its “Wild West” period. Traditional, non-Fidelity brokerage accounts have added bitcoin exposure through public investment trusts such as GBTC and various private fund structures, and a number of ETFs are currently seeking approval. Alternatively, there are a range of public companies that provide varying levels of indirect exposure, such as GPU manufacturers, blockchain companies, payment platforms and exchanges.

There are as many ways to gain investment exposure to bitcoin as there are opinions among the commentariat. We expect bitcoin to behave as a relatively uncorrelated, highly volatile financial asset for the foreseeable future; thus, any position should be sized appropriately to this substantial risk. As with all investments, we recommend would-be buyers do their own homework to better understand the fundamentals rather than rely on the rumor mill. As advisors and portfolio managers with an abiding interest in innovation, bitcoin is one of several early stage fintech ideas that fit in that broad theme. It is not an asset with much fundamental value today. Despite having captured much of the public imagination in the last several years, bitcoin is, at base, a nascent technology whose broader applications within business and the financial system lie waiting to be discovered. Along with indisputable risk, it may have upside optionality.

There are more and less efficient and more or less secure ways to implement ownership of crypto assets. ETFs, exchanges, “hot” and “cold” wallets, futures, private funds, et cetera—these various routes are not at all equivalent. Although we can neither recommend nor manage crypto assets on our clients' behalf, WMS advisors are happy to discuss this new frontier in greater detail. To clients who wish to gain exposure, we emphasize that it is vital to understand the risks and size positions appropriately. Cryptocurrencies are bets on immature technology that can in fact go to zero and, as a consequence, investors should risk no more than they are prepared to lose entirely. But as investors with an eye on transformative technological change, we must all pay attention, do our homework, and contemplate the possibility of radically different futures.

Related Posts

Inflation: Will the Dog Bark This Time?

Inflation: Will the Dog Bark This Time?

The Dog that Caught the Car

Last year we visited the topic of inflation, and wondered if, after a decade of false alarms, the...

2023 Thoughts: Euphoria in Reverse

Cash is once again king