11 min read

Market prognosticators, hoping to glean some sense of direction, have a raft of recent data to digest— soaring unemployment, collapsing oil prices, and historic output declines in both manufacturing and services. The economic analysis, however, remains incomplete without a forecast of how long lockdowns and social distancing measures will continue to be required. This latter question hinges on projections of a timeframe until we have 1) robust testing and tracing, 2) effective therapeutics, and 3) a clear pathway to a vaccine.

Below we offer an update from Josh Rowe, Portfolio Manager at WMS, who continues to closely monitor all relevant data and news regarding the pandemic and its potential impact on the economy and financial markets. Josh has been our point-person tracking the COVID-19 news cycle around the clock, but he is neither a medical doctor nor an epidemiologist. The views expressed here result from synthesizing numerous sources, including news reports, medical journals and preprints, and from speaking with several experts in the field. Therefore, the views of Josh and those of the investment committee should be regarded as an information resource only, and not a qualified medical or public health opinion.

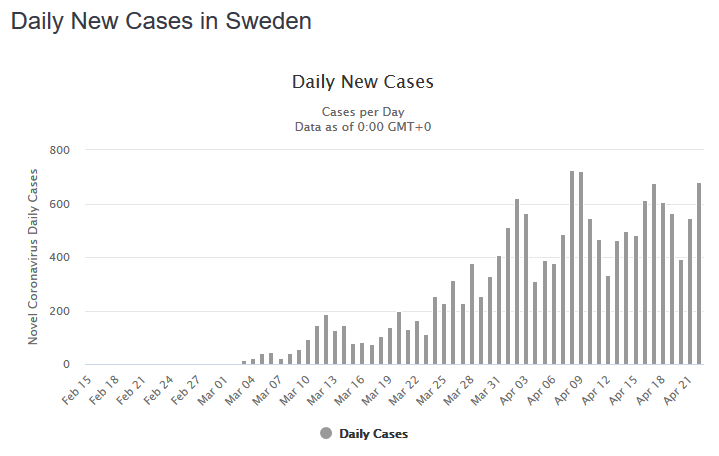

Sweden – A Natural Experiment

Sweden is (perhaps unintentionally) providing the world with a real-time natural experiment on what degree of containment measures are truly necessary. Over the coming weeks, we will learn a lot from the Swedish example; they are like the control arm in the global, enforced lockdown experiment. Cafes and schools in Stockholm remain open, though citizens are, for the most part, voluntarily adhering to stay-at-home recommendations. Does Sweden offer a preview of the United States’ future as we exit lockdown?

While Sweden has seen proportionally more infections and more deaths than its neighbors with stricter mass-quarantine rules, previous dire forecasts of overburdened hospitals and ballooning fatalities have so far failed to materialize. As of April 22, the rates of new cases and deaths, despite testing levels similar to those elsewhere in Europe, have ceased their exponential ascent and begun to plateau. Deaths have been concentrated in long-term care and nursing facilities, which are generally larger in Sweden than those in Denmark and Norway. The question of why Sweden may yet plateau despite its more relaxed rules is of essential interest to policymakers and investors around the world pondering their own exit strategies.

Swedish authorities point to a population nearing herd immunity, which would necessarily slow rates of new infections. In the last few weeks, a number of serological surveys (tests for antibodies in blood) undertaken around the world have revealed that no more than 20% of populations in hotspots like New York and Western Germany have been infected, while elsewhere antibodies appear present in fewer than 5% of test subjects. These tests have been attacked for biased sampling or faulty equipment that, if anything, is likely to over-estimate the numbers of infected. How are most countries so far from herd immunity, while Stockholm expects to get there by June? Or, if Sweden’s estimate is wide of the mark, why are cases slowing there and death rates not higher, given the relative permissiveness of the Swedish regime? Something doesn’t add up; either Sweden’s outbreak is a statistical outlier, with fewer hospitalizations and deaths than expected given the rate of infection, or other countries’ estimates of the percentage of populations infected are too low. In either case, we hope the Swedish trend holds. Sweden’s economy is affected by a slowdown in exports to the EU and the world, yet preliminary forecasts are for a decline in GDP of only 6% in Q2, roughly a third of the median estimate in the U.S.

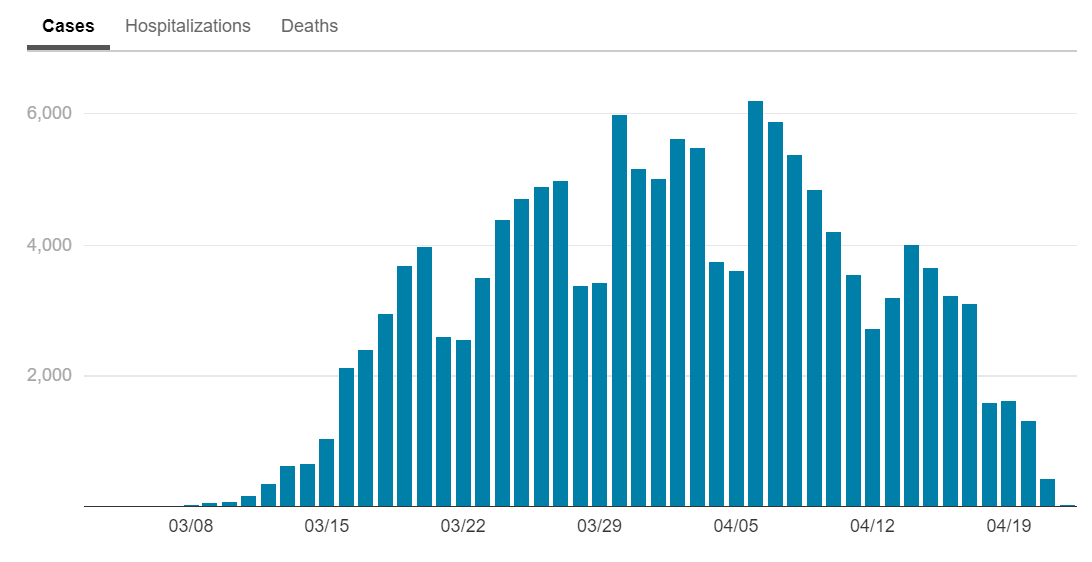

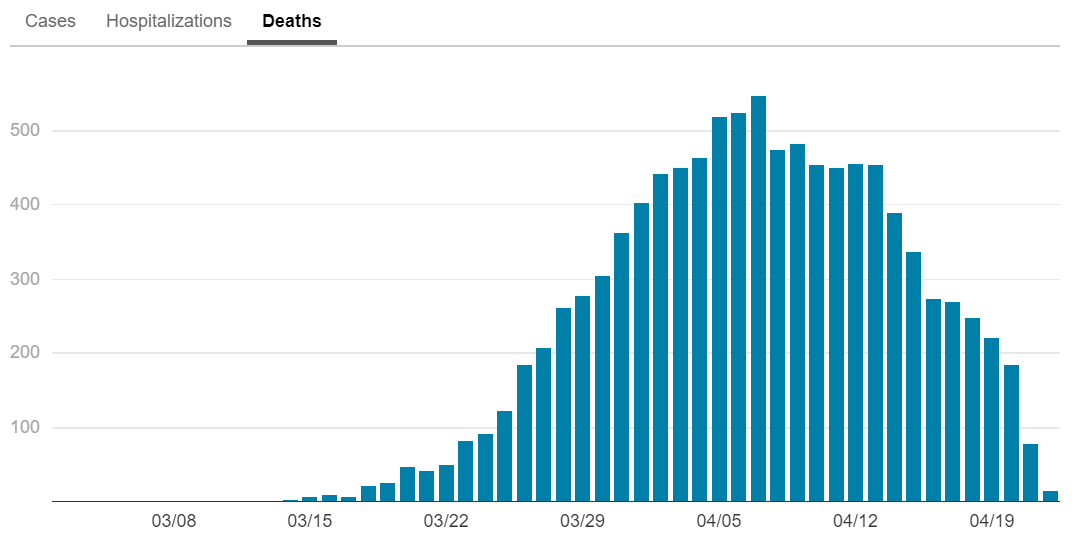

All Eyes on New York

New York continues to experience an elongated plateau. This does not really surprise us since cases in Italy and Spain both plateaued for about 10 days before coming down significantly. Deaths tend to lag infections by three weeks, so we expect to see a long right tail. Nevertheless, in New York City, the center of the United States’ epidemic, the trend is still positive. For daily updates, please visit: https://www1.nyc.gov/site/doh/covid/covid-19-data.page

Concern for Southern States

Georgia, Tennessee, and South Carolina are among states looking to follow the Swedish example. Will Southern states, whose governors were slow to implement lockdowns and have been critical of policies that squeeze business, rush to re-open too soon and experience a second spike? It is possible that due to inherent lower density in the South, greater heat and humidity, and continued voluntary physical distancing, most states will not experience the massive peak some predict. This will be very good news given the region’s lower insurance coverage in populations with higher levels of chronic illness. Even if a surge in cases does not overwhelm hospitals, governors are likely playing Russian roulette with many lives. States outside of the Northeast and West Coast are not projected to hit their peak until May 1st or later. Many Southern states are reopening parts of the economy before vigorous testing-and-tracing measures are in place, and before their outbreaks are truly under control. Lockdowns save lives, even as they strangle the economy. Different areas will find different ways to balance the costs and benefits. What will doubtless be necessary, even in less hard-hit states, is federal assistance with spiraling state and local budget shortfalls. Partisan haggling over appropriations is likely to continue into the summer, but for the sake of the economy, we hope Congress comes together to act, as they have done in previous phases of relief.

A Second Wave?

As we pass the peak of infections and hospital resource use, the critical question coming to the fore is the possibility of a big second wave in the fall. It is often overlooked that, during the Spanish flu pandemic, the winter of 1919 was worse than the initial wave in 1918. This outcome can be avoided if key areas are closer to herd immunity than we imagine. It is unlikely that reported “reinfections” in Asia represent a true second infection and not the result of a false negative test. And even if a patient has few antibodies, or the virus mutates so that antibodies bind less closely with it, second-round infections are likely to be less severe. Perhaps many “asymptomatic” carriers overcome the virus via their innate immunity, and never develop sufficient antibody levels to show up as positives in serological surveys. It may be hoped they can do so again. More sensitive, more accurate, larger-sample tests are coming soon and will shed some light on this question.

Another way to avoid a deadly surge is the discovery of effective therapeutics that prevent hospitalizations. Accordingly, we are very interested in wider remdesivir results (due in May). Early data have been mixed with leaked positive results lacking control groups and negative ones suffering from low enrollment. Remdesivir is among the most promising therapeutic candidates, but it is only one of many antivirals being tested. Several hundred drug candidates are being actively trialed at the moment, including dozens of approved and repurposed compounds. Particularly promising are medications that target secondary effects of infection, such as anti-inflammatory drugs Actemra and Kevzara, from Roche and Sanofi/Regeneron respectively, which should also produce large-scale clinical results in May or June. Also this summer we expect to see the start of human trials of monoclonal antibody treatments from Regeneron and Vir Biotechnology which, while less scalable than an antiviral, demonstrated proof-of-concept in the fight against Ebola.

Then there is the holy grail: a vaccine. The development, testing, mass production, and distribution of a vaccine is devilishly difficult especially in a compressed 18-month timeframe. The science is not guaranteed to work. After 30 years, we still don’t have a vaccine for HIV. COVID-19 is biologically simpler and the scale of the scientific effort is unheard of. A recent long-form article in The Economist reviews both the technological state of the art and the challenges a successful vaccine entails; it is highly recommended reading. Acknowledging all the difficulties of vaccine development, both scientific and economic, there is still reason to hope that through unprecedented research and policy coordination, established speed records can be shattered.

While Moderna was first to human tests and has seen promising recent results across its platform, the most aggressive timetable has undoubtedly been put forward by the University of Oxford, in England. Oxford’s candidate, ChAdOx1 nCoV-19, is going into human trials this week, and is being readied for manufacture in the millions of doses by the fall. Can such an ambitious schedule work? Oxford’s technology is what’s called a recombinant viral vector vaccine, which aims to induce the body to produce the infamous “spike” protein by smuggling its genes in a harmless chimpanzee adenovirus. The Oxford group’s approach has already demonstrated safety in humans for a MERS vaccine, and has elicited an immune response in monkeys. As The Economist describes, this is one of many existing “platform” technologies being adapted to the novel coronavirus, which accounts partly for the rapidity of the clinical development program. While vaccines ordinarily take years, the biotech sector is throwing heroic resources at the problem. Necessity is the mother of invention.

Test and Trace

The United States, for all of its research innovation and entrepreneurial dynamism, may simply not have the capacity to centrally manage an outbreak the way countries like South Korea and Germany have. As a result, we are hopeful that one of the “outs” enumerated above (earlier-than-expected herd immunity or an effective therapeutic) will reduce the risk that we need to institute stop-and-start lockdowns. These hopes are still hopes for the moment; we know what works and that is robust testing and tracing.

Therefore, the base case is still “test-and-trace”. The key variables to watch as we evaluate the nation’s relaxation of lockdowns are testing capacity and hiring at state public health departments. The latter is accelerating as a variety of human resources are tapped—non-specialist state employees, medical students, nonprofits, even potentially repatriated Peace Corps volunteers. There was good news this week as New York followed Massachusetts in forming a large private sector partnership. Public health experts at Johns Hopkins University estimate 260,000 recruits would be sufficient to track all contacts within a few days of a positive test, and it would cost $3.6 billion to maintain this crack force through year-end. This seems doable, but are states organized and coordinated enough to run such a program on a national scale? Smart phones are unlikely to be much help; even in Singapore only 20% of citizens have downloaded an opt-in Bluetooth-enabled app.

Contact tracing is only effective with a massive increase in testing. It’s possible to track daily the number of tests run in the United States (https://covidtracking.com/data/us-daily) with recent trends pointing in the right direction. Yet we remain well short of the goal. Until positive rates are in the low single digits (currently 18%) we can be sure we are not catching most infections. Over the next days and weeks, we will be watching both absolute numbers and positive rates closely. In order to really understand the scope of https://covidtracking.com/data/us-daily the infection, we will likely need to push from 150,000 tests a day to 1 million as we approach the end of lockdown. Nobel laureate economist Paul Romer and the Rockefeller Foundation are advocating for 30 million tests per week, but we likely don’t have enough swabs, technicians, or chemical reagents to carry out such a universal program, even assuming it is possible to repurpose and scale up labs while running many tests in parallel. But home tests (perhaps using saliva) could be a game changer and might permit an end-run around infrastructure and logistics problems.

The Road Forward

Ultimately, we are optimistic that most cities and regions will fare much better than the tragic examples of New York City, New Jersey, Madrid, or Lombardy. While this is only a guess, it appears to us that these unfortunate clusters may be largely the result of percolation, chaos, and chance – lots of infectious people circulating in the wrong place at the wrong time. That might explain why other large cities like Rome, Chicago, Barcelona and Munich did not suffer the same fate. We are also optimistic that a second wave may not be as severe, if greater numbers are effectively immune than in March, and with even marginal improvements in testing, increased supplies of PPE, and sufficient hospital capacity. In short, the spread should be slower and more manageable. We worry that the rollout of any vaccine is subject to all number of logistical snafus and distribution chain problems, however soon the clinical data arrive. Even the seasonal flu shot, which is manufactured in the hundreds of millions of doses, only sees 30-40% uptake.

Although we are somewhat hopeful about the globe’s response to the health crisis caused by the pandemic, we remain cautious about the state of the economy as governors look to restart their states. We believe massive Keynesian stimulus and debt monetization will contribute to near-term stabilization, but certain parts of the economy, namely travel, entertainment, dining and hospitality may take years to regain pre-pandemic levels. Moreover, economies do not rebound elastically from 15% unemployment; damage to consumer sentiment and increased risk aversion are typically lasting effects of downturns. As a result, household and firm savings rates will remain elevated, which will keep bond yields very low for some time. Equity returns will likely be better, but a return to all-time high stock prices and all-time low unemployment levels, we believe, is years away.

As we noted in our client letter of March 20th, trying to time a tactical exit from the stock market requires also knowing when to get back in. Else, we risk missing a majority of the gains that so often come in a matter of days. If an investor were to withdraw from the market today, that investor is in fact expressing a specific investment opinion about how the pandemic will play out over the next several quarters—this is an opinion about the pace and outcome of reopening the economy, the severity and duration of a potential second wave, the timing and success of a therapeutic option, and the date when a vaccine will be available for a majority of the U.S. population. As of today, still relatively early in our understanding of the epidemiology and virology of the COVID-19 pandemic, expressing any of these views with a high level of conviction would be presumptuous.

Finally, recall that, over time, money-weighted returns lag time-weighted returns. In other words, periods that follow many investors cashing out of the market generate above-average returns, while those that that follow investors’ aggressive adding to risk assets generate below-average returns. Accordingly, we recommend that clients with a longer-term horizon remain invested but renew their emphasis on high-quality assets, avoid stretching for yield or swinging for the fences, and remain focused on the long-term normalization that will certainly come, more or less swiftly, on the other side of the curve.

PLEASE SEE OUR IMPORTANT DISCLOSURES