3 min read

As a result of the passage of the Tax Cuts and Jobs Act in December, 2017, year-end tax planning for individual income tax returns has become even more important than in prior years.

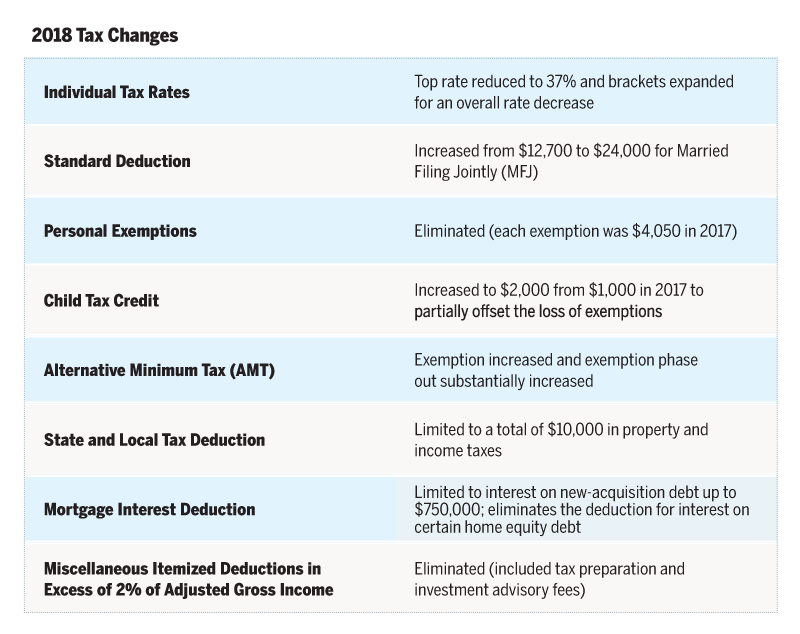

There are several notable individual tax changes effective Jan. 1, 2018, as the table below shows.

So what does the new tax bill mean to you? Here’s a sample of the options you should review with your tax advisor.

Review charitable giving

Many married taxpayers with no mortgage debt may be limited to total itemized deductions of $10,000 plus charitable contributions, which may be less than the increased standard deduction. By taking the standard deduction, any voluntary charitable contributions miss out on the tax-deduction benefit.

Bunch deductions

As a result, individuals should focus on multi-year tax projections of income and deductions. For example, consider bunching two years of charitable contributions into one year and itemize deductions in that year. The next year, take the standard deduction and then continue to alternate in subsequent years. In a higher income year, you may consider establishing a Donor Advised Fund (DAF) to maximize the charitable deduction.

Play your (tax) bracket

Consider accelerating income in years when you are below a bracket threshold. For example, you can “create” income by converting a traditional IRA to a Roth IRA.

Go direct with RMDs

If you must take required minimum distributions (RMDs) from your taxable IRA accounts, look into making charitable contributions directly to a charity from your IRA, with a limit of $100,000 per year. Reason: RMDs given to charity do not have to be included in taxable income. This results in AGI being reduced as opposed to income being reported and an itemized charitable deduction being taken. Consequently, you can take advantage of the full standard deduction and not miss out on the tax benefits of the charitable contribution.

Watch Maryland income taxes

Because Maryland’s tax code is linked to the federal code, these federal changes, particularly the elimination of many itemized deductions, may cause many taxpayers to pay increased state income taxes. For example, if a married couple elects to take the $24,000 standard deduction on their federal return, they must also take a standard deduction on their Maryland return.

To partially offset the negative effect of the federal changes, the Maryland legislature increased the 2018 MFJ standard deduction to $4,500, which is still significantly lower than the federal amount. They also will continue to allow personal exemptions. For example, if the married couple had federal itemized deductions of $20,000 that would have also been deductible for Maryland purposes, but elected to take the federal standard deduction of $24,000, they would only have a state standard deduction of $4,500. Therefore, the strategy of bundling deductions in certain years may also provide a Maryland benefit--taking a standard deduction in one year and itemizing the next.

Review the recurring year-end strategies

You should also remember to review the strategies that we have been regularly considering as part of year-end tax planning. These include:

- Making certain that charitable gifts are completed by the Dec. 31 deadline

- Front-loading charitable deductions in a Donor Advised Fund if your income is higher in 2018

- Making charitable contributions with appreciated securities that you may otherwise sell at a gain as part of your portfolio rebalancing

- Maximizing your annual gift exclusion to reduce your future estate (increased to $15,000 for 2018)

- Contributing to 529 plans

- Contributing to Health Savings Accounts

- Fully funding all eligible retirement plans by appropriate due date, up to the contribution limits: 401(k) and 403(b) elective employee deferrals ($18,500); additional catch-up deferral for age 50+ ($6,000); traditional or Roth IRA contribution ($5,500); IRA catch-up for age 50+ ($1,000)

Avoid April surprises

Many taxpayers make estimated tax payments based on the prior year’s taxes in order to avoid underpayment penalties. Because of the changes in deductions, a larger payment may be due in April than you expect. On the positive side, this may be offset by the lowering of the tax rates and expansion of the brackets. Therefore, it is even more important this year to run the numbers and plan accordingly. As always, we are available to consult with you and your tax advisor to help in any way possible.

Related Posts

These are the Times that Try Men's Souls

These are the Times that Try Men's Souls

The Dog that Caught the Car

Last year we visited the topic of inflation, and wondered if, after a decade of false alarms, the...

Inflation: Will the Dog Bark This Time?

Inflation: Will the Dog Bark This Time?