5 min read

Like all of you, the most we can do is watch in horror and sympathy at what is unfolding in Ukraine — perhaps also with some anxiety. In the modern world the economic impacts of war ripple far and none of us can escape untouched. It has been a long time since investors have had to deal with a war in Europe and even longer since they have had to worry about serious inflation.

It feels callous to ignore the unfolding humanitarian tragedy and the very real horror being inflicted on civilians as we write. A few weeks ago, Ukrainians were going to bars, shopping at stores, and visiting their grandmothers. Now they are fighting, fleeing, or hiding in air raid shelters. How easily this could be any of us. Yet here, at WMS Partners, our job is to look after investment portfolios. With the human toll in our hearts, we are forced to reckon with our heads. Our key points are summarized below:

- The war in Ukraine will impose huge economic costs on the world, exacerbating inflation and causing the consumer-led expansion to slow. The Federal Reserve is in a very difficult position.

- Stock markets have repriced in the face of this reality, but slower growth and lower valuations will be a challenge for investors in the months and quarters ahead.

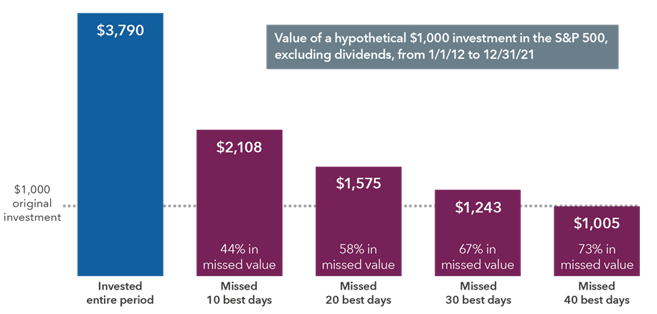

- Attempting to time an exit from the market based on geopolitical or recession risks is a self-defeating project. Investment portfolios perform best over long periods when we stay invested through short, sharp downdrafts.

- Greater caution is warranted when deploying capital and stickier inflation puts an even greater premium on true diversification.

Clearly, this environment is one that will prove challenging for both the economy and for risk assets like stocks. High-flying growth stocks are selling off as rising interest rates batter valuations while, at the same time, energy prices, GDP headwinds, and service sector worries pressure earnings expectations. On one hand, the U.S. economy comes into 2022 with a lot of momentum. Analysts had looked for S&P 500 operating earnings to grow by over 8%. A tight labor market and a blowout jobs report in February add to a base of fundamental strength. However, after an initially blasé reaction to the news of the invasion, U.S. equity markets are now in turmoil. WTI crude oil has blasted through $125 a barrel, the S&P 500 has declined further into correction territory and the NASDAQ 100 has passed the 20% drop threshold that signals a bear market. While there are precedents for the geopolitical tension that now roils the European continent—the Russian annexation of Crimea, the Gulf War, and even the Arab oil embargo of 1973—markets are now grappling with a much larger constellation of risk factors, including a nuclear threat, a likely global food crisis, and inflation that was already testing 8% in the U.S. on the back of a historic pandemic.

The worry today for markets is one of the most dreaded words in any investors’ vocabulary: “stagflation.” Stagflation is an economic phenomenon that is characterized by periods with considerable inflation, little to no growth, and potentially high unemployment. However one defines that term, the impact of the Ukraine conflict on the global economy clearly presents some stagflation scenarios—that is, it will serve to push consumer prices up for a wide variety of goods and services, while simultaneously weighing on economic growth. The European economy, dependent as it is on Russian energy supplies, is now within sight of recession. Could the U.S. also dip into a recession?

With the US electing to block energy imports from Russia, crude oil and natural gas prices will stay elevated for the considerable future regardless of whatever supply response OPEC and the U.S. shale patch can muster. Markets ultimately will test the price level that destroys currently booming demand for the black stuff. Is that $150? Is it $200? Even more alarming, wheat prices are soaring to new records. Fertilizer prices and those of its associate inputs (Russia exports 22% of the world’s ammonia—a key ingredient in nitrogen fertilizers) are rising and set to rise further. Nickel, a little used metal but one critical in the batteries that power EVs, rose so much this week that trading in futures contracts had to be suspended on the London Metals Exchange.

The U.S. is a resilient economy, self-supplied with energy (no more mile-long lines at the pump), and far less dependent on foreign commodities than Europe, or even than we were in the 1970s. But oil prices, like most key input prices, are set globally, and they drive up the costs of producing most finished goods. Commodity price surges feed back into transportation costs, as well as into the costs of food, manufacturing, and even drugs. Homes will cost more to heat and air condition. Soaring oil prices will hurt a services economy dependent on travel and leisure that was set to emerge from the winter of the Omicron variant. They will snarl up supply chains further as ships’ bunker prices rise and freight must be routed around Russia. As the recovery enters its third year, consumer pocketbooks are healthy. Financial conditions are accommodative and tightening only slowly. Real GDP is growing. We have weathered higher energy costs, in both inflation-adjusted and consumer wallet-share terms, before. But war complicates an already complicated picture.

While inflation stays heated, demand will fall and the likelihood of a recession increases. Fiscal stimulus, other than a possible draw from the U.S.’ Strategic Petroleum Reserve, is not forthcoming. Indeed 2020’s fiscal push is now rapidly receding in its impact. As recently as a few weeks ago, futures markets were discounting as many as seven Federal Reserve rate hikes this year. That draconian scenario may be off the table now, but the Fed will feel it has to reassert control and hike at least several times off of zero, if only to preserve “dry powder” should financial conditions tighten significantly. The flattening of the yield curve, with the benchmark 10-year/2-year spread tightening to 20 basis points, suggests that bond traders see the risk of recession in the next couple years rising dramatically.

It bears repeating that inflation represents not the level of prices but their rate of change. Brief, sharp shocks (such as those in nickel, wheat, and oil) are disruptive but do not in-and-of-themselves lead to durable inflationary spirals. Given time, supply chains can adjust, even to the removal of the largest country in the world by land area from global markets. As we have repeatedly advised, look to labor costs, shelter costs, and the expectations of consumers, businesses, and market participants for a view of the longer-term outlook.

We expect that the equity markets will likely remain volatile in the near term while the conflict in Ukraine persists and throughout the Fed’s hiking cycle. We also stress the importance of considering the potential duration of this conflict to look at where we go from here. Like with epidemiology, war and geostrategy are better left to the experts. But our instinct is that the conflict itself and the blow to the established world order preceding it are unlikely to be unwound as quickly as markets may expect. Clarity will no doubt emerge as the next weeks and months unfold but a tidy resolution looks increasingly remote.

So why do we remain allocated to stocks? Why not trade out ahead of macroeconomic or geopolitical volatility? The first and simplest answer is that attempting to second-guess the market and successfully pulling out ahead of recessions requires three things: a) perfect foresight, b) perfect timing, and c) the ability and wherewithal to get back in at the right moment. This is not a trade that consistently makes investors richer; quite the contrary in fact.

Chart source: Capital Group (www.capitalgroup.com)

Most importantly, stocks are long-run assets and their payoffs to patient investors accrue over the long run. Recessions tend to be short, and while geopolitical conflicts drag on, supply chains and markets eventually equilibrate. U.S. stocks are now more than 10% cheaper than they were at Christmas, albeit from a rather plump basis of valuation. Further, while inflation and stagflation remain risks, investing in the growing earnings of good businesses with pricing power remains the surest way to protect and compound wealth through a protracted inflationary environment. Complementing portfolios with physical assets, real estate, and less correlated private investments can diversify inflationary risks and help protect against recessions. For those of us anxiously watching our portfolios, this is not a moment to jettison the long-term plan. Neither, however, is it an opportune time to “buy the dip.”

Related Posts

There is a Silver Lining to Inflation - Expanded Tax Planning Opportunities

The Negative Effects of High Inflation

We have all experienced some form of the negative aspects of...

Impact of Stronger Dollar

The rising value of the US dollar is giving millions of American consumers a much-deserved...

Why Do We Invest?

Why do we invest?