3 min read

For some, these conversations have included the contemplation of a transition from employee to self-employed as they start their own businesses. For others, more consideration is given to compensation earned from consulting ventures or from serving on a board. In anticipation of these changes, we are evaluating which various alternative retirement savings vehicles align with clients’ retirement goals.

For many of these clients, Solo 401(k)s and SEP IRAs can be attractive alternatives to traditional retirement plans, allowing clients to contribute more of their self-employment income annually without being “phased out” from deducting these contributions on their annual income tax returns.

Moreover, the current income limitations disqualify many who participate in an employer plan from making income tax deductible contributions to Traditional and Roth IRA plans. For example, married couples with annual modified adjusted gross income (MAGI) over $124,000 ($75,000 for individuals) in 2020, cannot make deductible contributions to a Traditional IRA.

These alternative retirement vehicles are discussed in greater detail below.

Individual “Solo” 401(k):

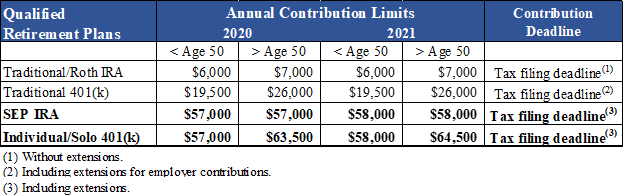

The Individual 401(k), also called the “One-Participant” or “Solo” 401(k), is a qualified retirement account for an individual or an individual and his or her spouse with self-employment income, such as income received for serving as a board member or income received from consulting fees. There can be no other employees. It operates similar to a traditional 401(k) with the major difference being the contribution limits. To be effective for 2020, the plan must be established by December 31, 2020.

SEP IRA:

Like the Individual 401(k), the Simplified Employee Pension (SEP) IRA is another qualified retirement plan offering higher annual contribution limits than a traditional 401(k) plan. Unlike Individual 401(k) plans which are available only to self-employed individuals and their spouses, SEP IRAs can also be set up by employers on behalf of any number of employees. Also, unlike the Individual 401(k), the initial plan can be established by the due date (including extensions) for the tax year.

Contributions:

The maximum annual contribution to any Individual 401(k) or SEP IRA is $57,000 for 2020. For those over age 50, a catch-up contribution of $6,500 for 2020 applies only to the Individual 401(k), bringing the total allowable contribution up to $63,500 for those over the age of 50. Therefore, no catch-up contribution may be made to a SEP IRA for those over age 50.

For self-employed persons contributing to a SEP IRA, this maximum contribution of $57,000 in 2020 is further limited to 20% of net earnings after subtracting the self-employment tax deduction1. Since contributions are discretionary, the percentage of compensation contributed may vary from year to year.

For the Individual 401(k), the 2020 total contribution limit of $57,000 is split between the theoretical employer and employee portions although these contributions originate from a single source, the self-employed person (or married couple). While the employee portion of the contribution is limited to $19,500 (or $26,000 if over age 50), the employer portion is limited to 20% of net earnings after subtracting the self-employment tax deduction1. As discussed, these contributions in aggregate are also subject to the $57,000 maximum limit. The difference between employer and employee portions only comes into play when contributing on a post-tax (or Roth) basis as only the employee portion, limited to $19,500 in 2020 (or $26,000 if over age 50), can be contributed post-tax. In this case, the remaining $37,500 could be contributed on a pre-tax basis by the employer with income tax deferred until withdrawal.

Account Set-up:

For both the Individual 401(k) and the SEP IRA, plan creation is simple and administrative costs are low. Most financial institutions offer IRS qualifying prototype plans, thereby simplifying the application and set-up process. WMS can help you complete all phases of this process.

WMS will continue to consider these alternatives, where applicable, as part of your continuing financial and investment planning. In the interim, please do not hesitate to contact your WMS advisor with any questions or concerns.

1Please contact your WMS advisor and/or tax accountant for further detail how these contribution limits apply to your specific situation

Related Posts

Tax Planning Takes on Even Greater Significance in This Election Year

There has been a great deal of discussion and speculation concerning possible changes to estate and...

Post-Election Tax Planning

Maryland Senate Approves Raising Estate Tax Exemption

We are happy to share the news that the Maryland Senate passed a measure, already passed by the...