5 min read

As we are now into the second half of the calendar year, our investment stance remains unchanged and positioned for growth. We believe that monetary policy settings, economic indicators, valuations and investor positioning remain positive for global stocks to outperform bonds. There have been a number of bumps in the road this year (and in recent years), but once again the global economy has survived and the equity bull market should continue to roll on.

The combination of moderate global economic growth and highly stimulative monetary policy has been sufficient to enable stocks to sharply outperform government bonds since the Great Recession. Aided by reflationary monetary policies, the global economy has proven resilient to numerous shocks in recent years, and shows signs of gaining modest additional strength over the next year. That said, capital markets have reached a critical juncture, with the Fed poised to initiate a gradual rate hike cycle that could begin as early as next month. For investors, the implication is that either equities or bonds will generate decent returns in the year ahead, but not both (as has largely been the case in the past several years). Our view is that equities will continue to trend higher as the Fed slowly hikes in response to improving economic growth, while bonds will suffer. Accordingly, we maintain our equity exposure and choose to underweight traditional bonds. We prefer cash to traditional fixed income, and continue to underweight commodities.

Stocks are slightly expensive, based on the most common valuation metric: the Standard & Poor’s 500-stock index trades at approximately 17 times the next year’s earnings for its companies, above the 25-year average of 15.7 times. However, that’s not the only metric of stock valuation. If you ask how much stocks are likely to return over the next decade or so compared to bonds, the answer is typically that stocks are supposed to return more than bonds because they’re riskier (they can be waylaid by a recession or a bear market). The magnitude of that extra return is called the “equity risk premium” and it can be inferred from current bond yields and expected growth in profits and dividends. Analysts have different measures of the equity risk premium, but the consensus is right around 4.5% right now, which is not as high as it was but is above the historical average.

This means an investor choosing between the two asset classes today could expect to earn about 4.5 percentage points more on stocks than bonds over the next decade. Stocks look less expensive on this metric because bond yields are so low—lower than fundamentals can explain. For example, in theory, the return on a 10-year bond should be roughly equal to the return on holding Treasury bills for 10 years, plus a bit extra, which is called the term premium. The term premium compensates investors for the fact that bonds are much more volatile than T-bills, largely because investors may guess wrong on the path of short-term rates.

With inflation low, the economy operating below capacity, and the Federal Reserve promising to tighten monetary policy ever so slowly, Treasury bills aren’t going to return much for a while. Yet even after taking that into account, bond yields are strangely low, because the term premium is close to zero. In other words, investors are practically paying up to own bonds rather than Treasury bills, which is not the way the world is supposed to work. What can explain the fact that investors are wary of the risk in owning stocks but are so cavalier about bonds? It comes down to the threats that hang over the world economy. If another financial crisis or deflation sucked the rich economies down, China fell into a slump, a big European government defaulted, a war broke out in eastern Europe, there was a 9/11-type terrorist attack or a pandemic swept the world, stocks would crater and terrified investors would rush for the security of bonds, driving their prices up and their yields down (the value of bonds move inversely to their yields).

This year’s roller-coaster on bond yields is probably due not just to changing perceptions of what the Fed or European Central Bank will do, but fluctuating fears of disaster (from Greece and from China, for example). Central banks should actually take comfort, then, if bond yields are headed up, because less fear of disaster means more confidence, more spending and more investment. The fact that bonds act as valuable insurance policies also means central banks and regulators should avoid creating artificial shortages of them. What’s the lesson for investors? If fear of disaster suddenly fades, yields will shoot up and prices will plunge. For stocks, it’s more complicated. Higher bond yields will squeeze the equity risk premium and thus make them less attractive over the next decade. On the other hand, a reduced fear of disaster should coincide with greater confidence in economic growth and profits and a greater appetite for holding stocks.

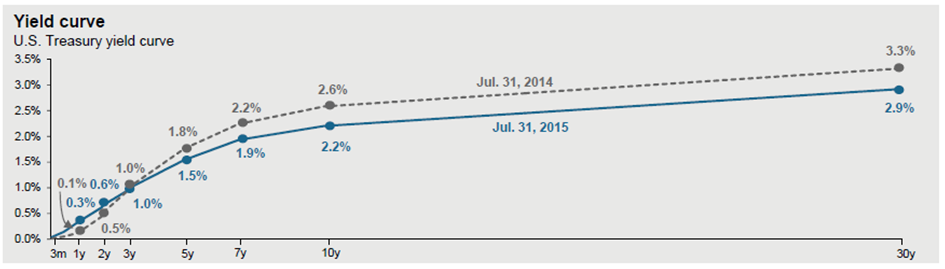

The risk of a disorderly rise in bond yields is not on many investors’ radars, given entrenched economic pessimism and low U.S. interest rate expectations. The economic and policy backdrops imply that only a benign rise in bond yields should occur. However, fickle investor sentiment (and aggressive bond positioning) may produce a more disruptive outcome. There have been two small such episodes in late-2010 and mid-2013, with the difference this time being that the Fed will be hiking rates, which usually sparks higher interest rate expectations. Despite clear messages from the Fed, investors are not discounting even a modest rate cycle in the coming years. Two-year Treasury yields, which are sensitive to changing rate expectations, are near the upper end of their range and a breakout looms if the economic data improves as we would expect.

To summarize our views:

- Global monetary conditions should remain very accommodative for the foreseeable future, even as the Fed (and Bank of England) slowly shift policy. Moreover, any sense of weaker economic data or financial market rioting will likely cause policymakers to pause. This is positive for equities.

- The global economic expansion (led by the U.S.) should slowly improve and broaden, especially with the euro-area on track to perform better. Global trade, after a very tough past four years, should also gradually pick up. The Chinese economy appears likely to remain on its long-term deceleration path, but the rebalancing towards the domestic economy offers the potential for some positive surprises. This should boost investor appetite for risk assets in non-natural resource driven economies.

- Bonds are expensive in absolute and relative terms, and are not prepared for a Fed (and Bank of England) rate cycle. Aggregate bond returns will likely be poor.

- Equities offer average absolute value (with the U.S. on the expensive side and most other areas on the more appealing side of the spectrum), and good relative value.

- Commodities and related plays are unappealing. Oil prices are testing the low end of their expected range, and are unlikely to undergo a bull phase in the coming year despite better demand.

- The consolidation in the U.S. dollar is not over, but another (modest) up-leg should take hold before yearend against most major currencies.