Source: Barclays, U.S. Treasury, FactSet, J.P. Morgan

Stocks of U.S. companies have been the best performing asset class for the past several years, and have been particularly bolstered since the presidential election in November. Fueled by hope for an end to political gridlock, and the potential for meaningful fiscal stimulus and a reversal in regulatory headwinds. The past ten weeks have shown that Washington has indeed changed, but the hopes for a significantly more pro-business backdrop are diminishing as the U.S. political system and its checks and balances become more prevalent. For better or worse, President Trump will likely have a hard time pushing through his agenda, and any net boost to the economy in the next year will be less than some had hoped for and take longer to play out.

The economy already had a decent head of steam before political confidence spiked and thus could prove resilient even if sentiment drops a notch. Economic data has consistently surprised on the upside for several months, which has also helped boost confidence and has supported stronger corporate earnings and upgrades over the past year. Forward earnings expectations for the U.S. and international markets continue to trend higher. Many investors though are leery that the recent rise in stock prices has outstripped potential earnings support. The valuations of stocks are rich, particularly in the U.S. We expect valuations to act as a restraint on global equity performance in the year ahead, but not to prevent stock prices from moving higher.

March has brought the first losing month in U.S. equities since October. There has been active sector rotation and a slight increase in volatility. Fixed income has been counter-intuitive. When Federal Reserve Chairwoman Janet Yellen raised interest rates by ¼ point earlier in the month, one would have thought that bond yields would follow suit. Instead, the ten year Treasury benchmark dropped from 2.6% the day of the hike to 2.4%. This action is perhaps a signal of investor’s growing concerns.

As a result, we anticipate a bumpy period ahead, as economic data cools and hopes for a significant upside breakout in U.S. growth fade. The short-term path for equities is somewhat dependent on political developments in the U.S. and Europe, but are starting from an elevated level given the run up in stocks since mid-2016 and the likelihood that economic data will be less one-sidedly positive. That said, we remain even more cautious towards fixed income and interest rate risk.

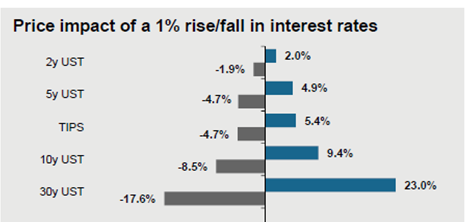

Bond investors still have considerable doubts on whether the Fed will be able to continue hiking rates in the next year. Two further ¼ -point increases would put the fed funds rate above the current level of the two year Treasury yield, underscoring the mismatch between Fed expectations for rates and the current pricing in the bond market. Bond yields and the dollar should soon edge higher, especially since the Fed was not intending that monetary conditions would ease as a result of its rate hikes.

The strong uptrend in stock prices, combined with some looming hurdles point to a near-term correction or consolidation phase for stocks. That said, we remain constructive on the global economic outlook over the next 6-12 months and expect stocks and credit to outperform bonds over that period.