5 min read

“There is much evidence that monetary changes have their effect only after a considerable lag and over a long period and that the lag is rather variable.”

A Program for Monetary Stability, by Milton Friedman

Looking Back

Since mid-year 2022, pundits have been warning of a recession being just around the corner. But over the last year there’s been no real sign of any economic downturn in the U.S. However, rising interest rates, high inflation, and an inverted yield curve all traditionally point to an imminent recession. In fact, the New York Fed recession probability indicator even suggests currently that there is a 70% chance of a U.S. recession sometime in the next 12 months. That’s the highest reading in more than four decades. Other reliable economic indicators are flashing warning signs that the U.S. economy could soon be rolling over. But despite all these factors, the U.S. labor market remains strong, and economists are divided on whether or not a recession is inevitable in this unusual economic environment.

Since the start of this year, the economy has shown remarkable resilience in the face of still-soaring inflation, aggressive monetary tightening, banking-sector turmoil sparked by the March collapse of Silicon Valley Bank, and a prolonged standoff over the U.S. federal debt ceiling. Despite all of this, U.S. consumers remain strong. In that context, we suppose that it is less surprising that through the first half of 2023, the S&P 500 is up about 16%; a rebound that surprises many analysts after equities’ brutal 2022 decline. And the tech-heavy Nasdaq has gained about 32%, for its best first-half in 40 years. Optimism that the U.S. central bank is approaching the end of its tightening campaign helped transform the technology-heavy gauge from 2022’s market underperformer (down 33%) to 2023’s first-half darling.

This strong start to the year now has many of those same pundits raising their growth forecasts for 2023 and pushing out a recession to the end of this year, or beyond. The strength of the U.S. economy in the face of our current monetary policy in the U.S. illustrates the lags that Milton Friedman wrote about in the above referenced quote. Judging those lags is proving particularly difficult this time around. After raising rates for ten consecutive meetings, the Fed bucked the trend at its June meeting and left interest rates unchanged. Signals from Fed members meant this was already expected, with the market looking for a “skip then hike” for the June and July meetings.

Although this current hiking cycle has often been described as an aggressive one as measured by the speed and magnitude with which rates have risen, it can’t be ignored that the low starting point has played a role, as it has taken some time to get rates to a level where they can be considered restrictive. Naturally then, the time taken from the first rate rise to when it has been able to impact the economy has been extended.

Monetary policy started from an ultra-loose level and while the Fed and others might have realized the need to tighten sooner, this came against a very uncertain backdrop of the ongoing pandemic. In addition, they had to offset the stimulus from fiscal policy as well as contending with the unusual effects of Covid on spending and the labor market.

Looking Forward

Will the tide begin to turn in favor of the Fed and their goals as we move forward? Will the market hit a new bull phase?

Monetary policy is now in restrictive territory and the benefits of fiscal support and excess savings are diminishing. The offsetting behavior of financial markets is also important, although it is not unique to this cycle. For example, in 2004-05 when the Fed raised rates by 150 basis points with little impact on 10- year bond yields - known at the time as the “Greenspan Conundrum” – there was much talk of the Fed losing control over monetary policy. The issue was that no matter how many times the Fed boosted rates (a total of 17 times, to be exact), financial conditions would ease, mainly in the form of lower long-term bond yields. What central bankers didn’t seem to understand was that it was all a classic case of misinformation. The Fed thought easier financial conditions suggested that markets didn’t believe its resolve to rein in inflation, when it was really the opposite. Markets were beating down long-term bond yields and bidding up stocks because it believed the Fed would get inflation under control.

In this cycle, the Fed may still have to do more to convince the markets that it is determined to beat inflation, which no doubt accounts for the increasingly hawkish tone, and further tightening. The Fed will likely bring its target short-term rate up to somewhere around 5.5% and keep it there for an extended period to quash persistently high inflation.

A generation of investors has little experience with investing in a high-interest-rate environment. In the 21st century, there has been only a little more than a year in which the federal-funds rate has been above 5%, from mid-2006 through the onset of the Great Financial Crisis of 2008-09. Not since 1995-2000 has the fed-funds rate been more than 5%—or even near 5%—for an extended period. Perhaps the biggest change that we see now is that, after a long period of paltry yields and a historically bad year in 2022, bonds are back. To state it plainly, bonds finally offer income again. Granted, the Fed’s campaign will likely come with continued volatility in the short run. But for long-term investors, today’s yields are a welcome change from the generally low income offered by bonds over much of the past two decades.

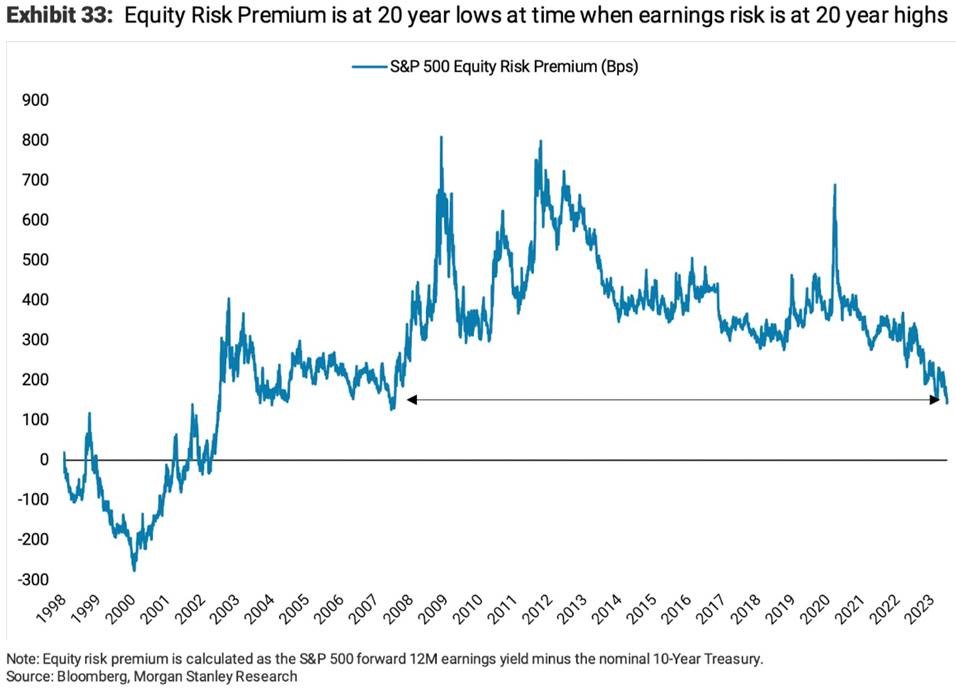

As for equities, historically a robust first half in the market is a good omen for the rest of the year. But we are not convinced of that this time, as the rally in tech stocks looks overblown, with rich valuations and just a handful of high-flyers like Apple, Microsoft and Nvidia providing the strength. Rising rates have boosted yields on fixed income assets and cash to their highest levels in decades, finally giving investors an alternative to equities. That does not appear to have hobbled stock returns so far this year, but it may dull the allure of equities going forward if rates stay elevated. The equity risk premium -- which measures the S&P 500's earnings yield against the yield on the 10-year Treasury note -- puts stocks at around their least attractive levels in over a decade.

Our Approach: Stay the Course – High Quality Stocks, Private Investments

Given these rich market valuations, we have positioned our Capital Appreciation Strategies at our long-term targets and continue to favor more defensive, higher quality equities to populate that portion of our public portfolio. We have used this year’s strength to trim where we were overexposed. Across the six earnings downturns that have occurred since 1985, companies with higher profitability, strong earnings growth, attractive interest coverage ratios, and above-average free cash flows have historically outperformed. As next twelve months earnings estimates for the S&P 500 have turned negative, these metrics and factors suggest now may be an appropriate time to increase exposure to high quality stocks.

We find it hard to get excited about buying a market-cap weighted index, like the S&P 500, at 18x forward earnings. We plan to stay defensively positioned. Bull markets do not usually start with the S&P trading at such expensive valuations.

Additionally, WMS Partners has always favored some proportion of private investments in well balanced portfolios, where they are appropriate for the individual investor. Private investments--given their uncorrelated and idiosyncratic nature--are critical to building portfolios diversified across many independent drivers of performance and provide opportunities to check the volatility and extended valuations typically seen in public markets.