11 min read

WMS Partners investment team discusses the impacts of COVID-19 on the financial markets and our world.

Click on the link below to connect to hear a recording of our client call from 3/20/2020:

These are certainly testing and anxious times. We are seeing dislocations in the financial system that we have not seen since 2008. Asset markets are selling first and asking questions later. Messages from Washington and from state governments seem confused and contradictory. It’s often said that markets know how to price risk, but there’s nothing they hate more than uncertainty. That goes for all of us as humans too. True uncertainty (“unknown unknowns” in Donald Rumsfeld’s phraseology) is terrifying and activates our fight or flight response. We believe the volatility we are seeing in markets these last few weeks is really a reflection of the questions we are all pondering: “How bad is this virus?” “How long will this last?” “Are we really prepared to deal with it?”

The World Health Organization describes the overabundance of information about the coronavirus as an “infodemic.” Some information is accurate, some information is partially accurate, and some information is wholly inaccurate. Simply put, this ”infodemic" is likely causing as much damage to the economy and financial markets as the actual pandemic. The tremendous volatility equity markets are currently experiencing is based on uncertainty and confusion, not on expert knowledge or concrete data regarding potential outcomes of the pandemic. Recall from our February 24, 2020 Market Update, “The Hazards of Forecasting,” we believe the suddenness with which events can turn serves mainly to highlight the futility of forecasts. Nevertheless, there are several things we do know about this outbreak that inform how long it may last and its ultimate effects on the economy. These facts generally militate against the worst-case scenarios that keep so many of us up at night.

We have been studying the pandemic intently since late January and we would like to bring many of these facts together here for those who may not have seen them, or who are unsure of their meaning. Our work is rooted in our deep sense of obligation to search out and understand the “knowable” facts about the virus. We review all we read and hear regarding the pandemic with a critical eye and ear with the goal of establishing a useful framework that will enable us to 1) better understand the situation and, based on that understanding, 2) make more informed investment decisions.

Synthesizing the Experts

These are not our opinions; they represent a synthesis of the evolving expert opinion around the globe and our attempt to cut through the “infodemic” to better understand the pandemic.

• If unchecked, COVID-19 may indeed infect as much as half of developed world populations over the course of several years. But many infections will likely be minor. Estimates of 80% of infections being “mild” do not take account of the numbers who are infected and asymptomatic or who have few symptoms but never receive a test. This larger number of mild cases is likely between two and ten times the number of official cases. These asymptomatic carriers are important in the rapid spread of the virus.

• Most of those who have died in China and in Italy have had serious “comorbidities,” or preexisting chronic illnesses. The most common are hypertension, diabetes, cancer, and heart disease. While otherwise healthy adults have died, they represent only about 1% of deaths in Italy. The average age of those dying in the hardest-hit area is 80 years old.

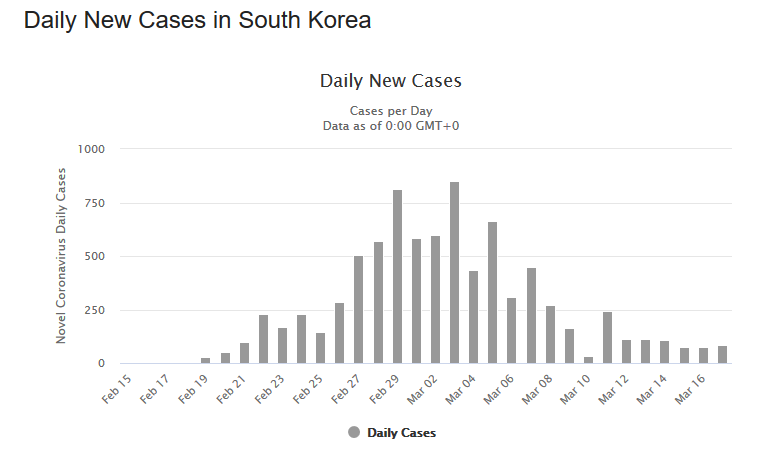

• “Social distancing” does work. It is the only method we have so far of “flattening the curve.” Hong Kong, Singapore, Taiwan, South Korea, and Japan all had early outbreaks and have managed to keep the total number of cases to manageable levels through immediate and strong social distancing efforts. Taiwan, as of Sunday, had 59 cases and 1 death. The U.S. is behind the eight-ball certainly, but so was China before authorities snapped into action. The virus was likely circulating in as much as 3% of the population of Wuhan from November to January when stronger measures were taken. On Wednesday, the entire country (including Wuhan) reported zero new domestic infections.

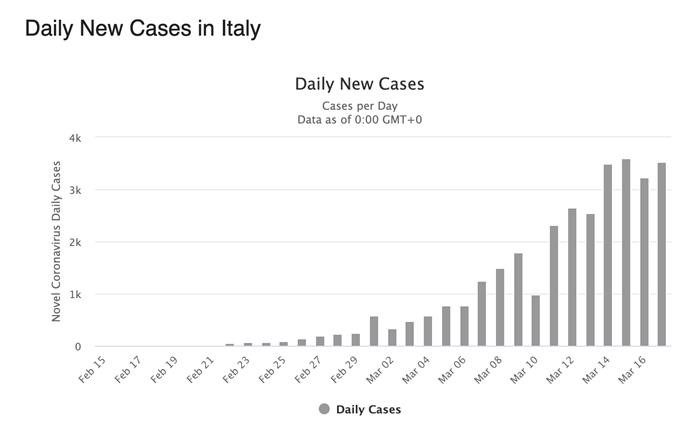

• The U.S. can learn from the examples of these East Asian countries, just as they learned from SARS in 2003. More importantly, we are learning the importance of flattening the curve from Europe. We are thought to be 10 to 11 days behind Italy, where healthcare infrastructure is overwhelmed and triaging patients and rationing ventilators have become the norm. But Italy, with its large elderly population—many living with children and grandchildren at home—appears now to be bending the curve as well. As of this week, new infections appear to be leveling off. The national quarantine instituted on March 10th appears to be working.

• “How long will the extreme social distancing measures last?” is a question no one can answer definitively. It depends on how we manage the outbreak from here. Everyone wants to return to work, for kids to return to school, and for service businesses to reopen. The more effective our quarantine, the sooner we can do this. China is going back to work, albeit with more handwashing and more caution than before the crisis. It took roughly two-and-a-half-months.

• Many people were scared when a computational model out of Imperial College London predicted last week that the virus would kill millions unless societies entered a pervasive stop-start quarantine effort that would last until a vaccine is found. Of course, this would be far more devastating for the global economy than the short recession markets had previously been expecting. Fortunately, this study relies on a number of parameters that appear to be overly pessimistic. The examples of China and South Korea, which both experienced exponentially growing outbreaks in prior months, show that with widespread testing, isolation of sick individuals, and “contact tracing” of their recent social network, we may all be able to leave our bunkers; only the recently exposed need self-isolate. A second wave of the virus is possible, but not assured. Subsequent waves will be less virulent due to partial “herd immunity.” Massively increased testing is the key to preventing a resurgence; after some regulatory roadblocks were cleared, the private sector is responding in a big way. By April, the laboratory instrument company Thermo Fisher Scientific plans to produce 5 million tests a week.

• A vaccine, we have been told many times, is at least 12-months away. Speed records are being broken as dozens of companies and university laboratories rush to find promising candidates, but safety concerns, the difficulty of mass-production, and the need for coordinated roll-out make vaccine development a tricky process. Human tests of U.S. firm Moderna’s RNA-based vaccine began ahead of schedule, and Chinese regulators may speed a domestic vaccine through faster. Luckily, we can reduce both the infection rates and death rates even in the absence of a vaccine through the improved and standardized use of already available therapeutics. There are many promising drug possibilities from the cheap, off-patent Malaria drug chloroquine, to Gilead Sciences' experimental antiviral remdesivir, to a common Japanese flu drug to several arthritis drugs that appear to slow the immune overreaction that causes severe respiratory distress and death in critical patients. Long before we have a vaccine, perhaps as soon as the fall, we are likely to have antibody treatments and prophylactics (preventive medicines) from convalescing patients’ blood plasma and from mice. Standardized treatment protocols are evolving and drug manufacturing is ramping up. Once we get past the initial peak of severe cases and the critical shortage of ventilators, fatality rates and ICU stays are likely to be reduced significantly. Treatment outcomes, even for the most vulnerable, will improve dramatically as we learn more.

• Furthermore, while early predictions that the virus would die out in warmer weather look premature, there does seem to be a strong correlation between outbreak “hotspots” and very particular temperature and humidity patterns. With warmer weather, the virus could very well have a harder time jumping from host to host. The reasons for this are not fully understood.

• So, how long will extreme social distancing have to last? There are so many variables involved in making such a prediction that we hesitate to try. But Bill Gates, who has studied epidemics and funded epidemic research, predicted six-to-ten weeks. This seems like a well-informed guess. The economy, with help from the Fed and fiscal stimulus, can survive that long in lockdown. Far longer might lead to some of the doomsday scenarios championed by stock market bears. Doubtless, the public health crisis must be resolved, at least partially, before economic recovery begins. Markets, as forecasting machines, will likely pick up ahead of the turn in fundamental activity, perhaps as case counts in Europe come down, or as critical numbers in the U.S. reach their peak in April or May. We can’t ever be sure about timing such an uncertain event, but the expert consensus that we read—from epidemiologists, to public health experts, to economists—to authorities in Asia, supports the view that we have a very tough two or three-month period ahead of us. And then the clouds should begin to part and the resilience of our people, our companies, and our economy will shine through.

Remaining True to a Long-Term Disciplined Strategy

We have attempted to be objective and not Pollyannaish in laying out the above facts, and in discussing our views on markets with our clients. None of us has ever seen an event like the new coronavirus, and radical uncertainty makes for treacherous investing. But we know that those who lived through stagflation, the crash of 1987, the tech bubble, September 11, and the Great Financial Crisis all saw stocks rebound to new highs within a period of a few years.

We are not arguing that one should not change investment strategy to reduce volatility, but the time to do so isn't after or even during a market sell-off. Making major investment decisions is not the course of wisdom when emotions are running high. If the decision was to own stocks, review the original reasons why, and reflect on the possible outcomes for the market over the next year or two. History says a rebound will eventually occur. After that rebound will be the time to consider adjusting the strategy. As the old saying goes, "In for a penny, in for a pound." We'd advise seeing the original decision through to better times.

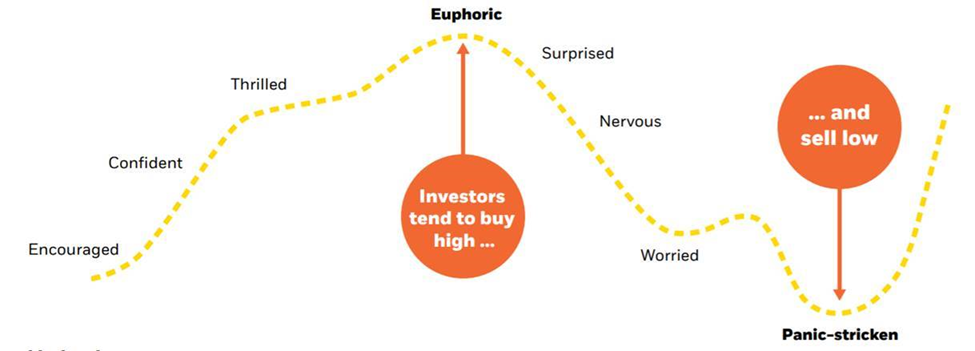

When things are going badly, we want to limit our losses. When things are going well, we wish we had invested more. We all fear missing out. It is Behavioral Finance 101. But when you’re investing, giving in to fear is often a losing strategy. More often than not, investors with this mindset tend to buy high and sell low as they invest more in a rising market and pull money out in a falling market.

We are not suggesting that we are at the absolute bottom in this scenario, but we are much closer to it than we were a couple of weeks ago. Our current allocation to equities is relatively low and the market has already priced in a pretty dire outcome from this crisis. Selling on emotion is a great way to sow seeds of future regret. We firmly believe that we should stay the course and try to tune out the “infodemic.” Easier said than done, we know.

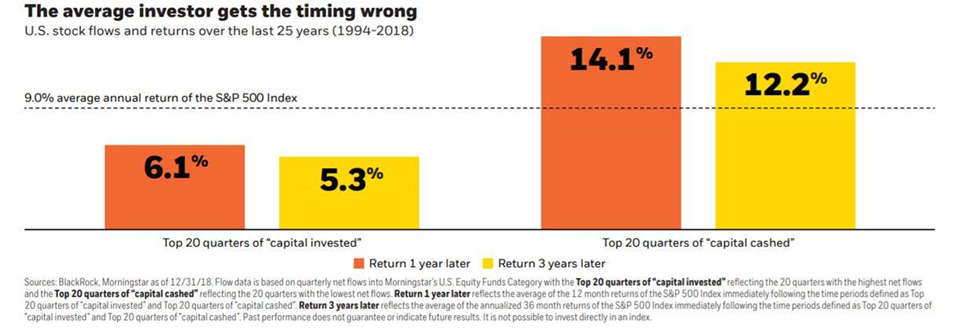

Trying to time the market requires knowing when to get back into stocks and not missing out on much of the gains that also can come in a matter of days (like the losses of the past two weeks). Investors who have followed their emotions, joining the crowd of other emotional investors, and paying heed to the “infodemic,” have, historically, regretted it. Periods that followed investors cashing out of the market have provided above-average returns, while periods that followed investors adding to the market have provided below-average returns. Here is some quantitative data that outlines the anecdotes we mention above:

The four most dangerous words in investing, it is said, are “this time is different.” But the truth can be better expressed in five words: “this time is always different.” And yet, over time, sticking to a thoughtful plan and a well-diversified investment portfolio based on a long-term disciplined asset allocation strategy weathers new storms and allows us to come back stronger. Let us remember that constant, and through this challenge continue to support each other in times of need, reach out to our friends and loved ones (even if only over the phone), and above all, focus on the health and wellbeing of ourselves and everyone around us.

References

https://www.ft.com/content/e015e096-6532-11ea-a6cd-df28cc3c6a68

https://www.worldometers.info/coronavirus/country/italy/

https://necsi.edu/review-of-ferguson-et-al-impact-of-non-pharmaceutical-interventions

Please See Our Important Disclosures

[audio mp3="https://www.wms-partners.com/wp-content/uploads/2020/03/Cutting-Through-the-‘Infodemic’-to-Better-Understand-the-Pandemic.mp3"][/audio]