The debate about whether active investment management or passive investment management will outperform in the long run has been going on for a very long time, and will likely continue for even longer. As you may know, active portfolio management focuses on outperforming a market segment compared to a specific benchmark, while passive portfolio management aims to mimic a particular index through lower-cost vehicles.

At WMS we use both types of strategies—there are some segments of the market where we feel active managers have an advantage, and others where they do not. However, no matter which side of the debate you fall on, one thing is certain—demand for passive strategies is on the rise.

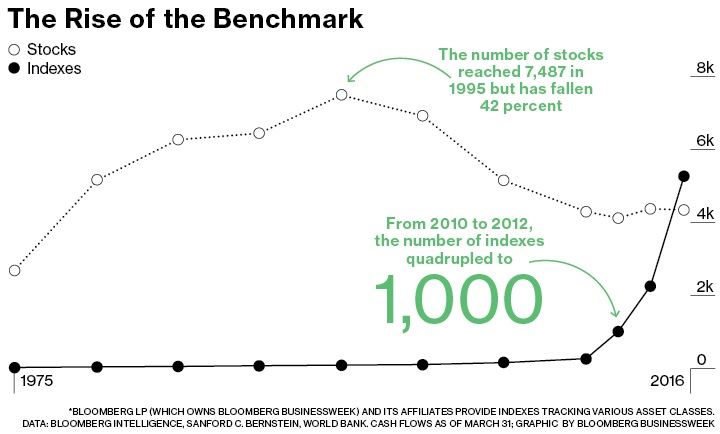

According to a recent study by Bloomberg (see chart below), there are now more market indexes in existence than there are U.S. stocks. The number of stocks has dropped by 42% since 1995, so that certainly has been part of the story. However, from 2010 to present the number of stocks has held fairly steady, while the number of benchmark indexes has gone from about 250 to over 5,000, close to a 2,000% increase!

The primary reason for this surge in indexes has been the parallel surge in the number of ETFs that have come to market. As demand for index-based strategies has risen, fund managers are scrambling to create lower-cost “index funds” for investors. As Bloomberg attests, over the past three years, $1.4 trillion of assets have flowed into index-oriented U.S. mutual funds and ETFs. The problem, however, is that many investment strategies do not correlate very well with existing market indexes. Not to be deterred by this minor detail, managers will just make sure a new index is created to fit their needs. When they then measure tracking error (the amount the manager’s performance deviates from the benchmark’s) against their benchmark, it will be attractively low, in a self-fulfilling way.

One of the consequences of this development is that investment advisors and managers now have a plethora of indexes from which to choose when benchmarking their own performance. At a basic level, the purpose of comparing one’s performance to an index is to give a fair and honest assessment (both to the investor and to the manager itself) of what value is being added from active management versus passively investing in an index with a similar strategy. Historically, we have not been fans of benchmarking entire client portfolios to just one particular index, particularly because a lot of our income-producing private investments do not have relevant benchmarks. The best metric for measuring our performance as total wealth managers is how well we help our clients in meeting their long-term financial goals. We still show major market indexes and allocation-weighted benchmarks on our reports, but we tend not to evaluate ourselves internally or market ourselves against these metrics, regardless of whether we “underperform” or “outperform”. Unfortunately, the same is not true for less scrupulous managers in the industry.

I was on a conference call a couple of weeks ago with a fixed income manager that we were evaluating. The portfolio manager made a statement along the lines of “we have outperformed our benchmark every year for the past 15 years.” The logical follow-up question on our end was, “what is your benchmark?”. When the answer to that question began with “Well…”, we could pretty much discount everything that followed. To use an analogy, it turned out that the fund was investing in apples and benchmarking themselves against oranges. Sure, they’re both in the same part of the food pyramid, but clearly apples are going to dominate oranges in most market environments.

In this particular instance, the manager was using a benchmark that we recognized, so it was easy to call them out on this mismatch. However, now that there are over 5,000 indexes from which to choose, it is becoming increasingly popular for investment managers to benchmark themselves to more and more obscure indexes, whether the goal is to minimize perceived tracking error, or to manufacture a perception of continuous outperformance.

The biggest takeaway from this is that now, more than ever, you need to take relative return information with a grain of salt. Just as we look at a lot more than past performance when evaluating investment managers, we look at a lot more than benchmark comparisons when evaluating the performance itself. An index that is created to track a strategy is in complete violation of the spirit of benchmarking altogether. Do you have a brand new investment strategy? There’s a benchmark for that!